Leasehold

Jul 2, 2026

When to Use Title Indemnity Insurance

When to use title indemnity insurance for historic, low‑risk defects and when to seek a proper legal fix instead.

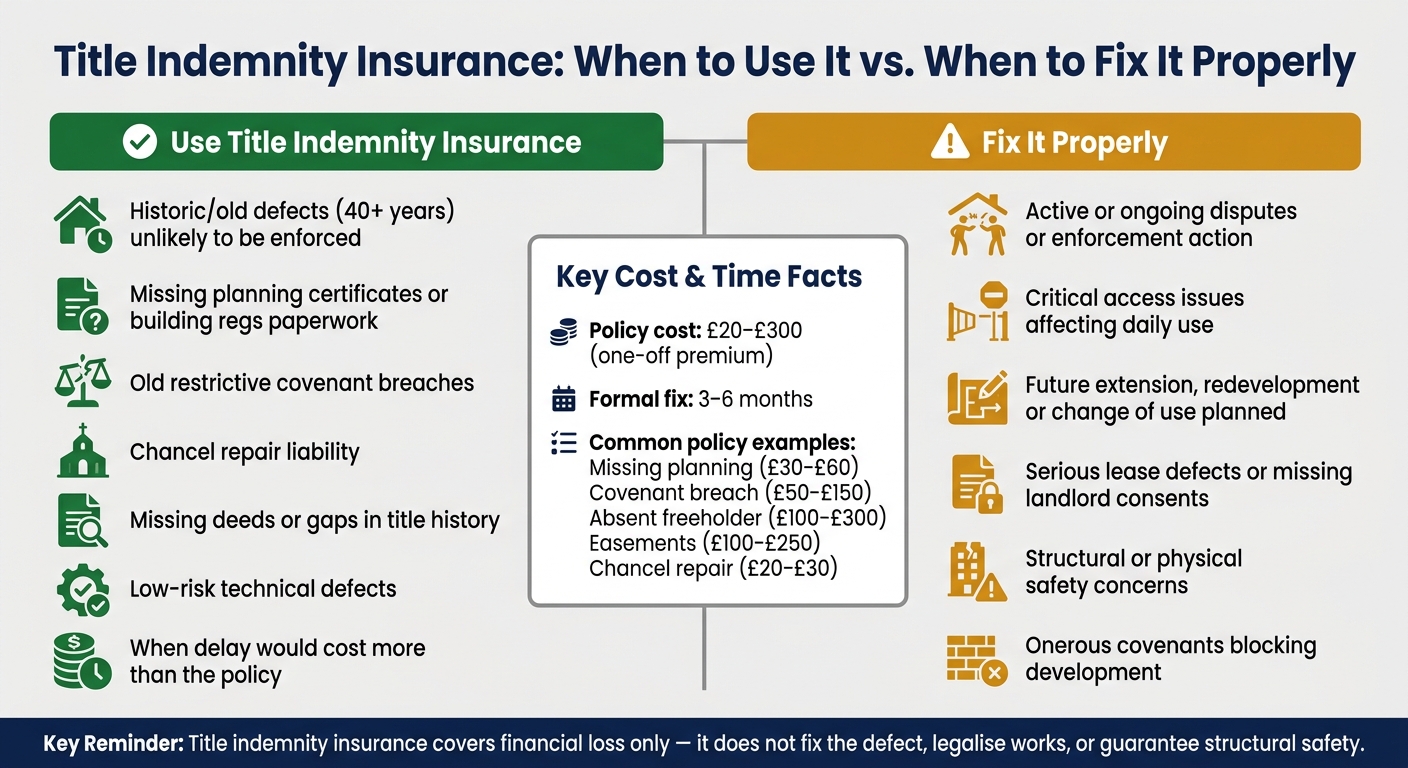

If a title problem is old, low-risk, and likely to delay the sale, I’d usually see title indemnity insurance as a way to keep the deal moving. It can cover legal costs, loss in value, and claims linked to defects such as missing planning papers, old covenant breaches, missing deeds, absent easements, and chancel repair liability.

But here’s the key point: it does not fix the defect. It also does not confirm that any work is safe. In many cases, the policy is a one-off payment, often from about £20 to £300, while a formal fix can take around 3 to 6 months. That time gap is often why buyers, sellers, and lenders agree to use it.

Before relying on it, I’d keep these points in mind:

A few common examples include:

| Situation | Insurance may work | Better to fix properly |

|---|---|---|

| Old missing certificates | Yes | Sometimes |

| Historic covenant breach | Yes | Sometimes |

| Active dispute or enforcement | No | Yes |

| Missing access needed for daily use | Sometimes not enough | Yes |

| Future extension or redevelopment planned | Often no | Yes |

| Structural or safety concern | No | Yes, with survey/legal remedy |

So if you want the short version, it’s this: I’d use title indemnity insurance when the risk is low, the defect is old, and delay would cost more than the policy. If the issue is active, affects day-to-day use, or could block future plans, I’d look for a proper legal fix instead.

Title Indemnity Insurance: When to Use It vs. When to Fix It Properly

The most common uses are unresolved planning, covenant, consent and title-history issues.

A common trigger is work that has clearly been done, but the paperwork has gone missing. Think an extension, loft conversion or structural alteration with nothing to prove it was signed off. In that situation, a solicitor will often suggest indemnity insurance instead of trying to get retrospective consent.

The same thing comes up with missing sign-off for windows, doors or boiler work. Policies for these issues often cost between £30 and £60. [2]

One point matters a lot here: contacting the local authority before cover is put in place can void the policy. [2]

That approach also applies when the defect is old rather than recent. If the work was done years ago, the lack of paperwork can still cause the same problem.

Some issues sit in the title for years before anyone spots them. A past owner may have breached a restrictive covenant long ago, and if the person with the right to enforce it still can, a lender will often want cover in place. Policies for restrictive covenant breaches usually cost between £50 and £150. [2]

Leasehold properties bring their own headaches. If alterations were made without the landlord's consent, that creates a title problem. And if the freeholder can't be found to give retrospective consent, absent freeholder cover may be used instead. That type of policy usually costs between £100 and £300. [2]

Rights can also be missing on paper even when everyone has used them for years. A property may depend on an access route, drain, pipe or other service, but have no recorded easement. If those rights aren't set out in the title, lenders often ask for insurance. Easement policies usually range from £100 to £250. [2]

When the issue goes back even further, the problem is often less about missing consent and more about missing documents.

Some title defects are buried deep in the record. Missing deeds, gaps in title history or incomplete Land Registry entries can all leave room for claims or hidden burdens later on.

Chancel repair liability is a well-known example in England and Wales. A property within certain old parish boundaries may still carry a duty to help pay for repairs to the local church. It is one of the cheaper policies on the market, often costing as little as £20 to £30. [2]

| Defect type | Risk | Typical policy | Typically covered |

|---|---|---|---|

| Missing deeds / gaps in title history | Unknown claims or rights in lost documents | Missing Information / Lost Deeds | Owner, lender and successors in title |

| Chancel repair liability | Historic obligation to contribute to parish church repair costs | Chancel Repair | Owner, lender and successors in title |

| Adverse possession / possessory title | Risk that a registered owner may claim land the seller has occupied without full title | Adverse Possession / Possessory Title | Owner and mortgage lender |

Once a defect shows up, the next issue is simple: can the sale still go ahead with insurance in place?

Title indemnity insurance is usually used when the defect is low risk, but fixing it would slow everything down. Sorting out a title problem through legal routes - such as applying for retrospective planning permission, getting missing consents, or chasing a formal remedy - can take three to six months [2]. Insurance, on the other hand, can often be put in place almost straight away. That can make all the difference when a property chain is at risk of stalling.

Mortgage lenders need to know that the title gives them acceptable security before they release funds. If a defect comes up during conveyancing, many lenders will not release the money until that defect is covered [10].

This tends to happen with older issues that are unlikely to lead to action, such as a past covenant breach or missing consent. In those cases, a policy can keep the lender satisfied without pushing back completion. That is why lenders often accept indemnity cover when the defect is historic and enforcement is unlikely.

Cost and speed often decide the issue. A one-off premium of £80 to £200 for a lack of planning permission is usually cheaper and faster than dealing with the legal fees, delay, and uncertainty that come with seeking retrospective consent [2].

Who pays for the policy is usually up for discussion. In practice, the seller often covers it, but some buyers will agree to pay if that helps keep the deal on track [9][8].

It is also worth checking that the limit of indemnity meets the lender's requirements [4][3]. If the defect is old, low risk, and holding up the deal, indemnity insurance is often the fastest way forward.

The main question is simple: is the defect old and unlikely to cause trouble, or is it still live and unresolved?

Aidan Welton of Stevens & Bolton LLP puts it bluntly:

"Indemnity insurance should be approached with caution and in many cases a policy should only be obtained as a last resort where all other avenues have been exhausted." [4]

That gets to the heart of it. Title indemnity insurance tends to work best for historic, low-risk defects where the chance of anyone bringing a claim is remote. It is much less helpful - and sometimes not enough at all - where the defect affects how the property can actually be used or developed.

One of the biggest traps is contact. After cover is arranged, you should not contact the local authority, a neighbour or a freeholder about the defect. In most cases, that will void the policy. Even making enquiries before the policy is put in place can make the risk uninsurable [1][7][6].

Policies also have clear limits. They do not cover issues that are already known, already disputed, or where enforcement action is already likely or under way [7]. So if the problem is active, the policy may be useless from the start.

Future plans can also cause trouble. If a buyer wants to extend, redevelop or change the use of the property, a standard policy is unlikely to do much. Most policies protect only the existing use of the property. Planned works or a change of use can void cover unless a specific endorsement is in place [7][5][4]. On top of that, many policies limit who can be told about the defect, usually restricting disclosure to buyers, lenders and legal advisers [5][3].

If the issue is active, disputed, or linked to future changes, insurance is usually the wrong tool.

Sometimes the better route is to fix the problem properly. If a deed of variation or missing document can be obtained without much delay, it often makes more sense to sort out the title rather than insure around the defect [7][8].

Emma Watson, Associate at Ison Harrison Solicitors, makes the point clearly:

"Insurance only provides financial compensation. It does not legalise unapproved works, grant missing rights of access, or remove a restrictive covenant." [7]

That matters a lot in practice. If access is needed for the property to be used at all, a cash payout does not fix the real issue [7][4]. In that sort of case, legal remedy is usually the better path.

The same goes for physical problems. Title indemnity insurance does not cover repairs, remedial works or structural defects [1][2]. Those need to be looked at separately through a professional survey.

| Usually suited to indemnity insurance | Usually better resolved formally |

|---|---|

| Historical breaches (e.g., 40+ years old) [1] | Active or ongoing disputes/enforcement action [7] |

| Missing old building certificates or FENSA records [2] | Critical access issues where physical use is essential [7][4] |

| Remote risks such as chancel repair liability [4][2] | Onerous covenants that block future development [7] |

| Missing deeds for unregistered land [1][6] | Serious lease defects or missing landlord consents [7] |

| Low-risk technical defects [6] | Structural safety concerns or urgent physical repairs [1][2] |

Once you get past the common defect types, the choice usually comes down to risk, cost and timing.

The rule of thumb is fairly simple: title indemnity insurance tends to make sense for historic defects that are unlikely to be enforced, but would be costly or slow to sort out through other routes. In practice, that often means old planning gaps, covenant breaches, or missing title documents.

That said, a policy has clear limits. It only covers financial loss. It can pay for legal costs and loss in value, but the defect itself still exists. It does not legalise unauthorised works, create missing rights, or guarantee that a structure is physically safe.

Legal cover and a structural inspection deal with two different things. If there may be a physical or structural problem, you still need an independent surveyor's report.

Use title indemnity insurance as a supplement to conveyancing and surveying, not a substitute.

The seller often pays for title indemnity insurance, especially when a defect comes up during the buyer’s conveyancing and the seller wants to keep the sale on track.

That said, who pays is usually settled through negotiation between the parties during the transaction.

In most cases, yes. Mortgage lenders often accept title indemnity insurance as a practical way to deal with known legal defects, because it covers losses linked to those issues.

That said, each lender has its own rules. So the policy needs to fit your transaction. Check with your solicitor that it meets your lender’s criteria before you go ahead.

Generally, no. If you've already contacted the council, freeholder, or another party that could enforce the defect, cover is usually unavailable.

Insurers normally want the defect to stay undisclosed to third parties. Once the issue has been raised, it may no longer be insurable. Indemnity insurance is meant for risks that aren't already in dispute or being actively pursued.