Leasehold

Jul 16, 2026

Title Defects in Property Investment: Risks Explained

Title defects—missing easements, covenants, record errors or boundary disputes—can block mortgages, delay sales and add substantial costs.

Title defects can disrupt property transactions and lead to financial losses. These issues include missing rights (e.g., access or drainage), restrictive covenants, boundary disputes, or errors in public records. They can make properties unmortgageable, delay sales, or reduce value. Correcting defects often costs £11,000–£15,000 and takes months.

Key takeaways:

Addressing title issues upfront is essential to protect your investment and avoid costly delays.

Title Defects in UK Property: Key Statistics and Financial Risks

Title defects can disrupt property ownership and transfer processes. As Free Conveyancing Advice succinctly puts it:

A title can be considered defective if there is something missing from it, or something within the title that should not be [2].

These issues arise when essential rights, like drainage or access provisions, are absent, or when there are unauthorised encumbrances such as outdated mortgages or restrictive covenants.

The consequences of title defects can be severe. They might block you from obtaining a mortgage, lower your property's value, or limit its development potential. In fact, many UK lenders refuse to fund properties with unresolved covenant breaches or missing easements [4]. Despite their impact, these legal oversights are more frequent than many property owners might expect.

Title defects affect thousands of homeowners across the UK annually [4]. Often, these problems remain hidden until conveyancing begins. Property expert Samantha Graham highlights the frustration this causes:

It is one of the most frustrating and least-talked-about causes of delayed or collapsed property sales. And the worst part? Many sellers have no idea the problem exists until they are already weeks into the conveyancing process [4].

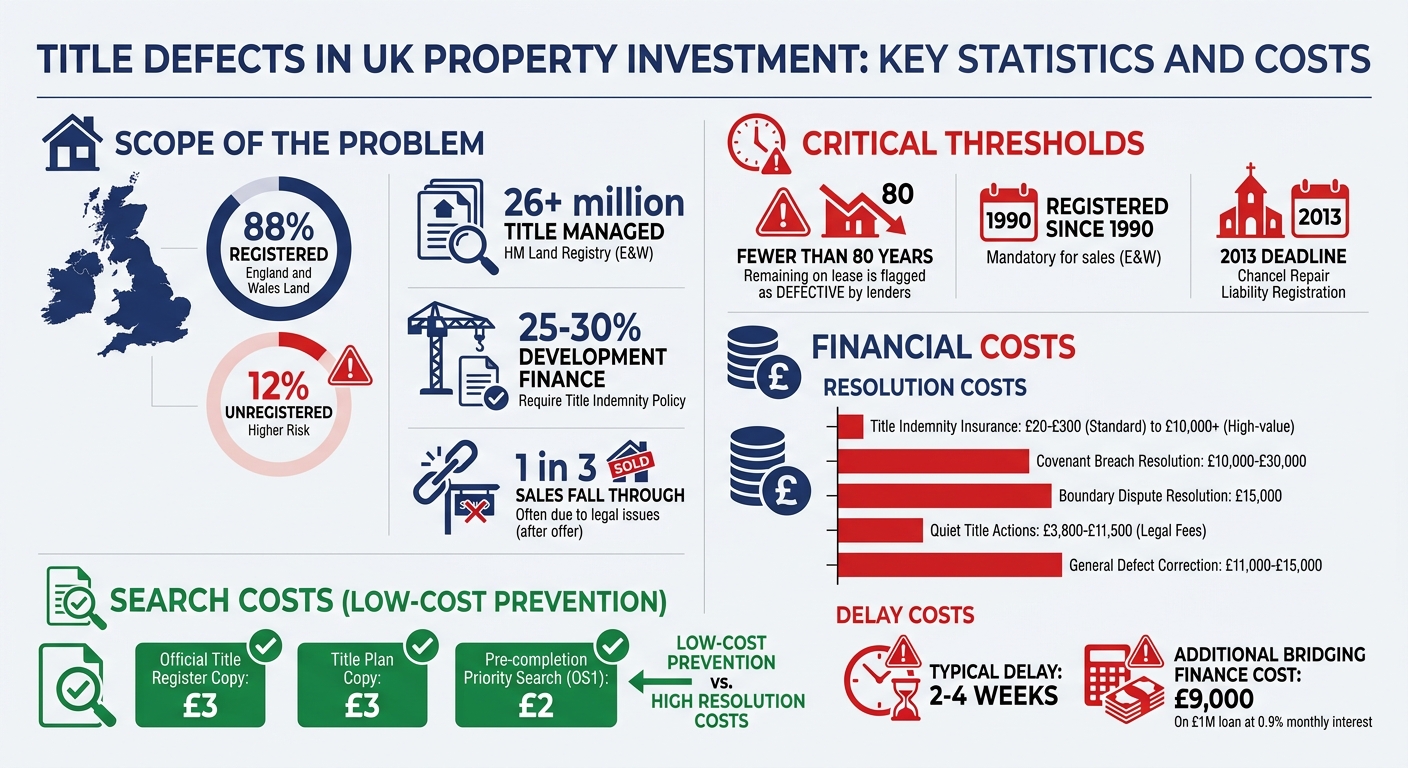

Older properties are especially vulnerable. Since 1990, land registration has been mandatory for sales in England and Wales. However, properties held within families for generations may still be unregistered, increasing the chances of title gaps [4]. Additionally, leases with fewer than 80 years remaining are often flagged by lenders as defective, making such properties difficult to finance [4].

Another historic issue is chancel repair liability. This medieval obligation, requiring landowners to fund local church repairs, must have been registered as a land charge after 2013 to remain enforceable. However, properties sold or remortgaged before that date may still carry this liability if it was previously recorded [4].

Understanding these risks is essential for anyone involved in property transactions, especially investors looking to manage potential complications effectively.

When it comes to financial and legal risks in property transactions, several common title defects can create significant challenges.

Outstanding charges tied to previous owners often linger on records until they are officially removed. For instance, if a mortgage lender neglects to file discharge forms (DS1 or e-DS1) after a loan is paid off, these charges remain on the Land Registry records [4][5]. Until such charges are cleared, a clean title cannot be issued.

Tax liens are another hurdle that must be resolved before a title is considered clear [6]. Additionally, some properties may carry chancel repair liability, a historical obligation to fund local church repairs, which can still appear on older records [4].

Restrictive covenants can also complicate matters. These legal agreements impose conditions on the property, such as prohibiting business use or limiting extensions. They can hinder resale unless addressed or covered by insurance [4]. Similarly, missing easements - formal rights for access or utilities like drainage over neighbouring land - can create significant complications [5][2].

Next, let’s look at how errors in public records can undermine the integrity of a title.

Simple administrative mistakes can have a big impact. For example, name discrepancies caused by marriage, divorce, deed poll changes, or basic clerical errors can create defects. If the name on the Land Registry doesn’t match the seller’s identification, it can delay or even halt a sale [5][4].

Errors in property descriptions or outdated ownership details can also cause issues [6]. For leasehold properties, missing or incomplete records about ground rent, lease terms, or landlord information often lead to lengthy legal investigations [5]. With over 26 million titles managed by HM Land Registry in England and Wales, even small data entry mistakes during registration can result in significant delays [5].

Beyond these clerical issues, fraud, forgery, and boundary disputes add further layers of complexity.

Boundary issues are a frequent source of disputes. The Land Registry uses a "general boundaries" system based on Ordnance Survey maps. As Pine Property Guide explains:

title plan boundaries are general boundaries... the red edging shows the approximate position of the boundary, not the exact legal line.

This lack of precision can lead to disagreements, especially when extensions or other changes are made near boundary lines [5][4].

Another potential complication is possessory title, which is granted when original deeds are lost or when ownership is based on adverse possession (commonly known as squatter’s rights). This type of title indicates an uncertain ownership history and often requires indemnity insurance to secure mortgage approval [5][4].

Lastly, third-party claims - such as notices or cautions filed by former partners or others claiming a beneficial interest in the property - can point to unresolved legal disputes or even fraud [5]. These claims can significantly delay or derail a transaction if not addressed promptly.

Title defects can seriously disrupt property transactions and impact returns. If a title is deemed unmarketable, the property cannot be legally sold or transferred until the issue is resolved [7]. This often results in failed sales or lengthy delays - typically adding two to four weeks to the timeline. For instance, bridging finance borrowers could face additional costs of up to £9,000 on a £1,000,000 loan at 0.9% monthly interest during such delays [8]. Additionally, mortgage lenders are often unwilling to finance properties with unresolved issues like breaches of restrictive covenants, unclear boundaries, or leases with fewer than 80 years remaining [4].

The costs of resolving these issues can vary significantly. Title indemnity insurance might cost anywhere from a few hundred pounds to over £10,000 for high-value properties. On the other hand, formal legal solutions can be much more expensive - ranging from £10,000 to £30,000 for resolving covenant breaches and around £15,000 for boundary disputes [8]. Notably, 25% to 30% of development finance transactions in the UK require at least one title indemnity policy [8]. Without resolution, title defects can permanently reduce a property's value and limit its development potential. As Samantha Graham from Property Swift highlights:

A well‐maintained, legally clean title is every bit as important as a well‐maintained building when it comes time to sell [4].

These financial risks are compounded by the legal challenges that often accompany title defects.

Beyond financial losses, title defects can lead to complex legal problems. For example, boundary disputes can arise when discrepancies exist between physical property features and Land Registry title plans. Such disputes often result in lengthy litigation with neighbours over land strips or shared driveways [4].

Restrictive covenant breaches are another common issue. These breaches could involve unauthorised home extensions or running a business from a residential property, leaving investors vulnerable to legal action [4]. Similarly, unrecorded easements - such as those needed for access, drainage, or utilities - can block development or usage and often require negotiation or court intervention to resolve [5,7].

Leasehold properties bring their own set of complications, including disagreements over service charges, ground rents, or obtaining consent from absent freeholders [4]. Missing historical deeds or errors in public records can further obscure ownership, making it difficult to prove title and potentially leading to disputes during a sale or remortgage [5,7]. Ongoing litigation or unresolved legal issues tied to the property can also delay transactions and prove both costly and time-consuming to address [6].

Detecting title defects starts with a detailed review of HM Land Registry documents, which cover around 88% of England and Wales' 26+ million property titles. These records are split into three key sections [9]:

Buyers should cross-check the title plan (based on an Ordnance Survey map with red-edged general boundaries) against the property's physical boundaries to spot any encroachments or discrepancies [4]. It's important to note that these maps provide approximate boundaries. For the 12% of land still unregistered, buyers must review the chain of deeds to verify ownership and uncover any historical issues [9]. An official copy of the title register or title plan is available online for £3 each [9][5].

Before completion, solicitors conduct a pre-completion priority search (OS1) for £2, ensuring no recent changes to the register and securing a 30-working-day protection period [9]. With one in three UK property sales falling through after an offer is accepted - often due to issues uncovered during legal checks - thorough and early document verification is crucial [9].

While document checks are essential, they should be paired with physical surveys to uncover risks that paperwork alone might miss.

Legal records provide a foundation, but professional surveys confirm the property's physical condition and boundaries. Surveys such as Level 2 HomeBuyer Reports and Level 3 Building Surveys from Survey Merchant compare physical features like fences, walls, or hedges to the title plan, helping identify boundary disputes or encroachments [4][1]. These inspections can also reveal if structures like garages, decking, or extensions cross legal boundaries, potentially constituting trespass [1][10].

Surveys may also uncover prescriptive easements - rights established through long-term use but not formally recorded, such as a neighbour's drainage pipe running under the property [4]. For leasehold properties, surveys highlight issues like leases under 80 years, problematic ground rent clauses, or missing building safety documentation, especially important after the Grenfell Tower fire [4].

Commissioning a survey early in the buying process can help buyers address title defects before contracts are exchanged. This proactive approach minimises delays and ensures the property's legal status matches its physical reality.

When dealing with a title defect, indemnity insurance is often the go-to solution. This insurance, with a one-off premium typically ranging from £20 to £300, offers protection against financial losses stemming from issues like undiscovered liens, breaches of historic restrictive covenants, or chancel repair liabilities [5]. As Samantha Graham from Property Swift explains:

The solution is usually indemnity insurance, which protects the buyer (and future owners) against any claim arising from the breach [4].

However, there’s a key rule to follow: avoid contacting the covenant beneficiary before securing the insurance. Doing so could lead to written acknowledgment, which may render the insurance invalid [4].

For added protection, warranty deeds can transfer the responsibility of ensuring a clear title onto the seller. Should defects surface post-completion, the seller is obligated to address them [11]. Buyers can also safeguard themselves by including title requisition clauses in their contracts. These clauses grant a 10-day window for the seller to resolve any issues, or the buyer can cancel the agreement [1]. Once a requisition notice is issued, sellers typically have five working days to respond [1].

Administrative corrections are another avenue for resolving title issues. HM Land Registry can amend errors such as incorrect names or outdated addresses [4]. For missing links in the title chain, statutory declarations can formalise these gaps, reducing the risk of future disputes [4]. Similarly, prescriptive easements - rights acquired through long-term informal use, such as a neighbour’s drainage pipe - can be formalised through legal documentation to avoid future conflicts [4].

While legal measures are essential, technical expertise often plays a complementary role in addressing on-site concerns.

In addition to legal remedies, expert surveyors play a vital role in resolving and preventing title defects. Accurate surveys ensure that physical boundaries and property alterations are properly documented and legally updated, providing a more secure foundation for property transactions.

Survey Merchant’s Red Book valuations, for example, deliver RICS-compliant assessments that clarify a property’s actual market value, particularly when title issues affect its saleability. For disputes involving boundaries or encroachments, party wall agreements can formalise shared structures, reducing the risk of costly litigation. Should legal disputes escalate, expert witness reports from Survey Merchant can provide critical technical evidence.

If a property has undergone extensions or alterations since its last registration, a professional resurvey is essential to update the title plan. This step is often necessary to satisfy mortgage lenders and can take approximately three months to complete [1][5]. Resolving any boundary ambiguities well before a sale is crucial, as lenders may refuse to proceed if surveys reveal structures that cross legal boundaries [4]. Addressing these issues early can prevent last-minute transaction failures and ensure a smoother process for all parties involved.

Identifying and addressing title defects early is key to protecting property investments. These issues, such as unresolved liens, restrictive covenant breaches, boundary disputes, or public record errors, can derail transactions, block mortgage approvals, and introduce significant financial risks. Left unresolved, they can turn a promising investment into a costly mistake.

The potential costs are steep. Quiet title actions can range from £3,800 to £11,500 in legal fees [12], and unresolved defects could render a property unmortgageable, particularly leasehold properties with fewer than 80 years left on the lease [4]. UK law holds buyers accountable for all information revealed in standard conveyancing searches, making thorough due diligence a non-negotiable step [2].

Taking preventative steps is the best way to avoid these pitfalls. A pre-purchase title review can uncover issues like missing easements, administrative errors, or outdated records before contracts are signed [4]. For properties with physical alterations, professional resurveys can ensure boundary lines and structural changes are properly documented and legally compliant. If historic defects can't be resolved quickly, indemnity insurance offers a practical safeguard that meets lender requirements [5].

Partnering with experienced professionals is crucial. Expert surveyors, like those at Survey Merchant, can identify and address title defects before they impact investment value. Their RICS-compliant Red Book valuations and expert witness reports provide clarity on property values and support in resolving technical disputes. Meanwhile, conveyancing solicitors can rectify public record errors and uncover overriding interests. Tackling these issues during the due diligence phase is far more cost-effective and less stressful than dealing with them after purchase, ensuring both immediate ownership security and long-term investment stability [3][4].

A title defect can block your chances of getting a mortgage, especially if it impacts the legal ownership or the ability to transfer the property. Typical problems include encumbrances or unresolved legal claims tied to the title. Since lenders often see these issues as potential risks, it's crucial to address them before seeking financing.

If you're facing an unresolved title defect during a property transaction or loan process, title indemnity insurance is worth considering. This type of insurance becomes particularly crucial if a lender insists on protection against potential financial losses caused by these defects. It provides reassurance by reducing the risks associated with unresolved title problems.

When buying a property, it's crucial to spot any issues early, ideally before exchanging contracts. One way to do this is by examining the property's title through HM Land Registry. You can request official copies of the title register and title plan. These documents reveal important details such as ownership, charges, restrictions, covenants, easements, mortgages, and boundary information.

This process can help you uncover potential problems like mismatched ownership names, unresolved mortgages, restrictive covenants, or boundary disputes. Addressing these issues might involve resolving them directly or obtaining indemnity insurance to protect against future complications.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes