If you’re a professional paid for your expertise—think surveyor, accountant, or IT consultant—your advice is your product. Clients trust you to help them make big decisions, but what happens if that advice, service, or design turns out to be flawed?

A simple oversight could lead to a client losing thousands, or even millions, of pounds. This is precisely where professional indemnity (PI) insurance steps in. It’s a crucial financial safety net for any business that provides professional services.

Think of it as a financial bodyguard for your professional reputation and your company’s bank account. If a client alleges they’ve suffered a loss because of your work and decides to sue for professional negligence, your PI policy is designed to cover the legal defence costs and any compensation awarded. Without it, a single claim could be financially catastrophic.

For a deeper dive into the specifics, especially the distinctions used in different markets, you can review this guide on Understanding E&O coverage.

Who Really Needs PI Insurance?

The short answer is any professional who provides advice, designs, or specialist services for a fee. It’s especially vital in the UK’s property and construction sectors, where the stakes are incredibly high.

The PI insurance market in the UK is a massive ecosystem, generating an estimated £3.3 billion in annual premiums across roughly 1.5 million policyholders. The construction and design industry is the largest single contributor, with surveyors and property professionals alone accounting for an estimated £90 million in yearly premiums. You can explore more about these market figures on professionalindemnity.co.uk.

What It Covers and Why It Matters

PI insurance isn’t just for when you’ve made a genuine mistake. It also provides the funds to defend your business against baseless allegations, which can be just as costly and time-consuming to fight.

To put it simply, PI cover protects you from the financial fallout of a wide range of professional risks. The table below offers a quick summary of what it does and why it’s so essential.

Professional Indemnity Insurance At a Glance

| Aspect | Description | Example |

|---|---|---|

| Who Needs It | Professionals who provide specialist advice, designs, or services to clients. | A chartered surveyor providing a homebuyer report, an architect designing a new build, or an IT consultant managing a client's network security. |

| What It Covers | Claims from clients alleging financial loss due to professional negligence, errors, omissions, or bad advice. | A homebuyer discovers a major structural defect that wasn’t mentioned in their survey report and sues the surveyor for the cost of repairs and the drop in property value. |

| Why It's Essential | It covers legal defence costs and compensation awards, protecting your business from financial ruin. | Without PI cover, the surveyor would have to personally fund a costly legal battle and any damages awarded, which could bankrupt their business. |

Ultimately, having robust PI insurance allows you to operate with confidence, knowing you have a powerful shield in place if a client dispute ever escalates.

Table of Contents

- Who Really Needs PI Insurance?

- What It Covers and Why It Matters

- Upholding Standards With Minimum Levels of Cover

- Why You Need to Verify Their Cover

- Why Should I Care If My Surveyor Has PI Insurance?

- What Is the Difference Between 'Any One Claim' and 'In the Aggregate' Cover?

- Is a Surveyor's Insurance Checked If My Estate Agent Recommends Them?

- What Is Run-Off Cover and Why Is It Important?

Why Is Professional Indemnity Insurance a Requirement?

For many UK professionals, especially those in high-stakes fields like property and construction, carrying professional indemnity (PI) insurance isn't just a good idea—it’s non-negotiable. In fact, for most recognised professional bodies, it’s a mandatory condition of membership.

Think of organisations like the Royal Institution of Chartered Surveyors (RICS) or the Architects Registration Board (ARB). A massive part of their job is to protect the public and uphold professional standards. By making PI insurance compulsory, they make sure that their members are financially accountable for the advice and services they provide.

This requirement does two crucial things. Firstly, it safeguards the integrity of the profession itself. Secondly, and far more importantly for you as a client, it creates a clear path to compensation if a professional's mistake results in a financial loss. This is a core part of what makes credentials like RICS accreditation so valuable.

Upholding Standards With Minimum Levels of Cover

These professional bodies don’t just ask members to get any old policy. They set strict minimum requirements for the level of indemnity, ensuring there’s a proper safety net in place for the public.

While PI insurance has been around for a while, it was a pivotal shift in 1976 that cemented its status from a sensible precaution to a mandatory safeguard for many professions. Today, regulations dictate the minimum standards, with the most common baseline set at £500,000 for each and every claim. Of course, many established firms go much higher, with mid-range businesses often holding cover between £5 million and £10 million, and top-tier firms insured for as much as £250 million.

Client Takeaway: When you hire a professional who belongs to a regulatory body, their mandated PI insurance is your financial backstop. It’s a formal guarantee that funds are available to compensate you if their work is negligent and causes you a loss.

Why You Need to Verify Their Cover

While these organisations enforce the rules, the final check rests with you, the client. Before you hire any professional, you should always ask to see their certificate of PI insurance. Don't be shy about it—it’s standard practice.

This simple act of due diligence confirms three key things:

- Active Cover: It proves their insurance is current and hasn't lapsed.

- Adequate Limit: You can check if their level of indemnity is suitable for the value and scope of your project.

- Credibility: It shows the professional takes their responsibilities seriously and isn’t afraid of accountability.

This applies across the board, from surveyors to estate agents. In fact, this helpful guide to UK estate agency insurance details some of the specific PI considerations for that sector. Ultimately, a professional who readily provides proof of their insurance is sending a clear signal: they are committed to quality work and protecting their clients.

Understanding Your PI Insurance Coverage

So, what exactly does professional indemnity (PI) insurance protect against? Think of it as a crucial safety net for any professional who provides advice or specialist services for a living.

This includes a wide range of experts, from architects and accountants to IT consultants. For property surveyors, however, it’s absolutely essential. The common thread is that clients depend on their professional knowledge, and if that advice turns out to be flawed, the financial fallout can be severe. That’s precisely when a PI policy is designed to step in.

What Does PI Insurance Actually Cover?

A standard PI policy isn’t just for a single, catastrophic mistake. It’s built to respond to a variety of professional slip-ups that result in a financial loss for a client. While the specifics can vary from one insurer to another, most policies will cover a few core areas.

Typically, your protection will extend to:

- Professional Negligence: This is the big one and the most common reason for a claim. It covers mistakes or things you forgot to do in your work, like a surveyor failing to spot and report a serious structural defect during an inspection.

- Intellectual Property Infringement: This protects you if you accidentally use copyrighted material—such as images or text—without getting the right permissions first.

- Loss of Data or Documents: If you were to lose or damage sensitive client files, whether they’re on paper or on a hard drive, the policy could cover the costs to replace or recover them.

- Defamation: This covers you against claims of libel (written) or slander (spoken) if a client argues that something you said or wrote has unfairly damaged their reputation.

For a homebuyer, this coverage is a vital line of defence. Imagine you buy a house for £400,000 based on a valuation report. A few months later, you discover the surveyor’s valuation was inaccurate and the property is actually only worth £320,000. The £80,000 financial hole you’re left with would be the basis for a professional negligence claim against the surveyor's PI insurance.

What Isn't Covered by a PI Policy?

It’s just as important to know what’s covered as what isn’t. No insurance policy is a blank cheque, and PI insurance is no exception. Insurers are very particular about the risks they won’t take on, which almost always involves deliberate or dishonest actions.

Important Note: A PI policy is there to protect against genuine, unintentional errors made in the course of your professional work. It's not a get-out-of-jail-free card for illegal activity or fraud.

You can almost always expect a PI policy to exclude claims that arise from:

- Intentional wrongdoing or fraud

- Criminal acts

- Claims related to bodily injury or property damage (this is usually covered by Public Liability insurance)

- Employment disputes with your own staff

- Insolvency of your own business

By understanding both the scope and the limits of PI insurance, professionals and their clients get a much clearer picture of the protection it provides. It’s a backstop for honest mistakes, not a shield for deliberate misconduct.

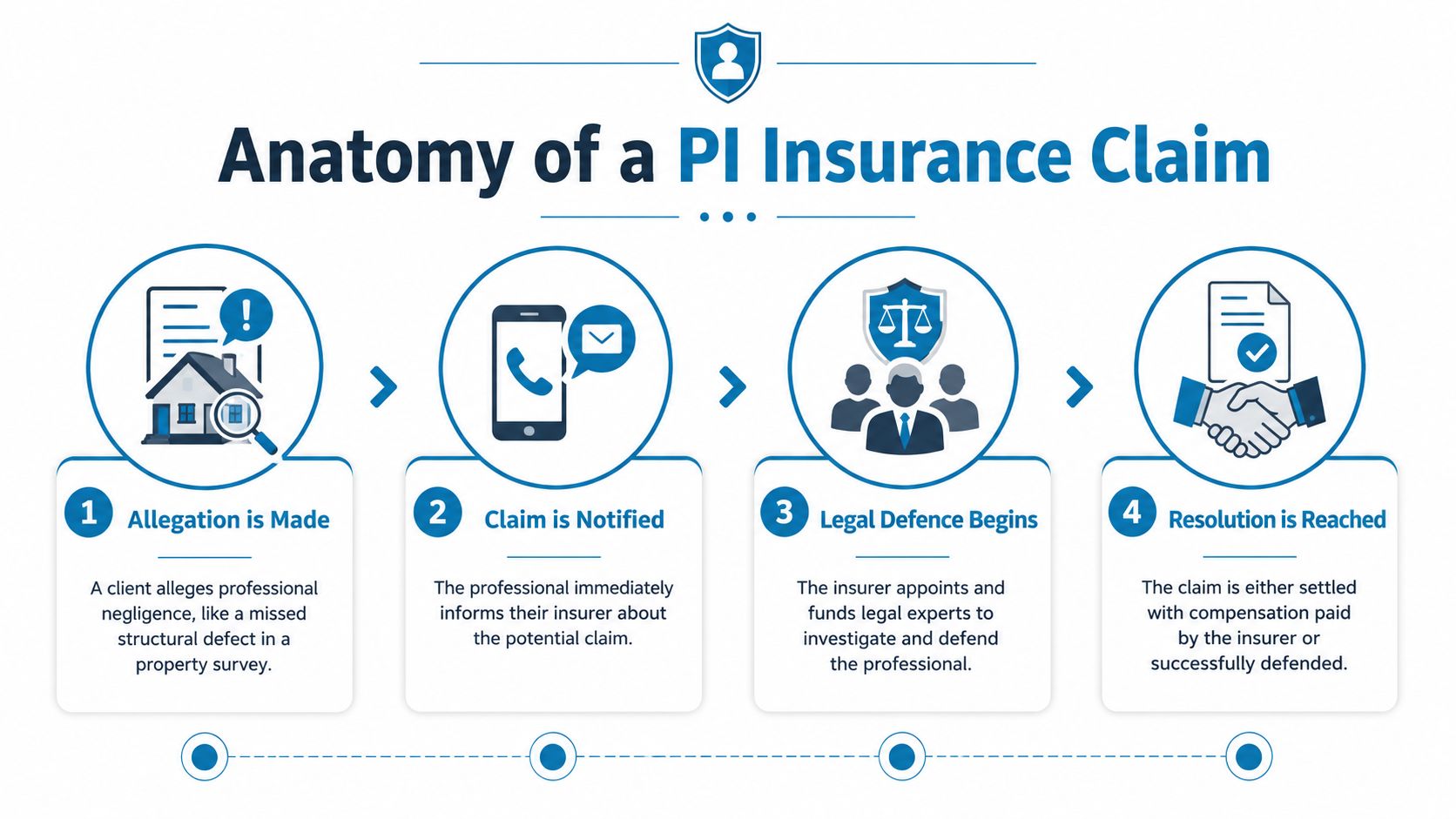

How a Real-World PI Claim Unfolds

It’s one thing to talk about professional indemnity (PI) insurance in theory, but its real value hits home when a crisis strikes. Think of it as a financial backstop that kicks in the moment a client accuses you of negligence, protecting your business from costs that could otherwise be crippling.

Let's walk through a common, and frankly terrifying, scenario for a property surveyor. Imagine a homebuyer proceeds with a £550,000 house purchase, reassured by a clean bill of health from a Level 3 Building Survey. Six months down the line, after a bout of heavy rain, alarming cracks start snaking across the walls. A second opinion from an independent expert reveals historical subsidence—something the original survey completely missed. The estimated repair bill? A staggering £75,000.

This is the exact moment a professional indemnity claim is triggered. The process isn't a chaotic free-for-all; it follows a clear path designed to manage a stressful and complex situation.

Anatomy of a PI Insurance Claim

When that angry letter from the homebuyer's solicitor lands, it sets off a chain of events that the surveyor's PI policy is built to handle. Without that cover, the surveyor would be on their own, facing the full legal and financial weight of the claim.

So, how does it all play out? The table below breaks down the typical journey of a claim, from the initial allegation to the final resolution.

| Stage | What Happens | Who Covers The Cost? |

|---|---|---|

| 1. The Allegation | A client (e.g., a homebuyer) alleges they have suffered a financial loss due to a professional's negligence (e.g., a missed defect in a survey). They send a formal letter of claim. | The professional's time and stress. |

| 2. Insurer Notification | The professional immediately notifies their PI insurer, providing all relevant documents. This is a crucial first step and a policy requirement. | The professional's policy excess (if applicable). |

| 3. Legal Defence | The insurer appoints and funds a specialist law firm to investigate the claim's merits, assess liability, and manage all communications with the claimant's legal team. | The PI Insurer. |

| 4. Investigation & Strategy | The legal team gathers evidence, interviews witnesses, and may appoint their own experts to review the case. They then advise the insurer on whether to fight the claim or seek a settlement. | The PI Insurer. |

| 5. Resolution | The case is either settled out of court or defended. If settled, the insurer pays the agreed compensation. If defended and lost, the insurer pays the court-ordered damages. | The PI Insurer (for both legal costs and compensation). |

As you can see, the insurer takes over the heavy lifting, providing both the legal muscle and the financial safety net needed to navigate the storm.

From Allegation to Resolution

The journey from an initial complaint to a final outcome isn’t instant. It’s a carefully managed process of investigation, legal negotiation, and strategic decision-making, all orchestrated by the insurance provider.

Let’s apply this to our surveyor's £75,000 subsidence nightmare:

Step 1: Immediate Notification: The moment the surveyor receives the claim, they forward it to their PI insurer along with the original report and all correspondence. This fast action is vital and a key condition of their policy.

Step 2: Legal Defence Mounts: The insurer instructs a specialist law firm to take on the case. These legal experts dive into the details, assess whether the surveyor was genuinely at fault, and take over all communication. This immediately shields the surveyor from having to find and pay for expensive legal advice upfront.

Step 3: A Path to Resolution: After reviewing all the evidence, the insurer’s legal team might conclude that the survey was indeed negligent. In that scenario, they would negotiate a settlement, and the PI policy would pay out the £75,000 in compensation, plus all the associated legal fees. Conversely, if they believe the surveyor’s work was sound, the insurer would fund the legal battle to defend the claim in court.

And make no mistake, this isn't a remote risk. UK firms notify their insurers of around 142,000 professional negligence claims each year, with surveyors, valuers, and construction professionals often in the firing line. For a deeper dive into what can go wrong, this UK homeowner's guide on surveyor negligence is an excellent resource.

Without insurance, the cost of defending and settling just one of these claims could easily bankrupt an otherwise successful business.

A Homebuyer's Guide to Verifying a Surveyor's Insurance

When you hire a surveyor, you’re putting a huge amount of financial trust in their professional judgement. So, verifying their professional indemnity (PI) insurance isn't just another box-ticking exercise; it's a vital bit of due diligence that protects your biggest investment. Before you commit to anyone, you should always ask to see their current certificate of insurance.

Any professional and reputable surveyor will expect this request and should provide the document without any fuss. It’s a standard part of their process and a clear sign they take their responsibilities seriously. Honestly, this simple step is just as important as confirming surveyor qualifications in the UK.

Once you have the certificate in hand, you need to know what you're looking for. It’s about more than just seeing the words "Professional Indemnity Insurance" printed at the top.

Key Details on the Insurance Certificate

Think of the certificate as a snapshot of the surveyor’s professional safety net. You'll want to scrutinise it for a few essential details to make sure their cover is solid and actually relevant to your property purchase.

Here’s your verification checklist:

- The Insured Firm's Name: Does the name on the policy exactly match the name of the firm you're hiring? Any difference here could be a major red flag.

- The Insurer's Name: The policy should be underwritten by a well-known, reputable insurer. This indicates financial stability and reliability if a claim is ever needed.

- The Policy Period: Check that the policy is currently active and will cover the date your survey is actually being done. An expired policy gives you zero protection.

- The Limit of Indemnity: This is the maximum amount the insurer will pay out for a single claim. Make sure this limit is high enough to cover the value of your property and the potential financial loss you could face if a serious mistake was made.

Crucial Insight: The level of indemnity is a good indicator of a firm’s ability to manage risk. A low limit of indemnity for a survey on a high-value property suggests the cover might not be adequate.

Understanding the Retroactive Date

This is probably the most overlooked detail on the certificate, but it's absolutely critical. It’s called the retroactive date. Professional indemnity insurance is what’s known as a "claims-made" policy, which means the policy must be active when a claim is made, not necessarily when the original survey was carried out.

The retroactive date tells you how far back their past work is covered. For instance, a policy with a retroactive date of 1st January 2015 will cover claims that arise from any work done since that date. If the date is very recent, it could leave a massive gap, meaning any work the surveyor did before that point is uninsured.

Ideally, you want to see a date that lines up with when the surveyor or their firm first started trading. This ensures all their previous work is properly protected, giving you complete peace of mind.

Your Professional Indemnity Insurance Questions Answered

When you're dealing with something as valuable as property, you hear the term 'Professional Indemnity insurance' thrown around. It can sound a bit like jargon, but understanding what it means is one of the most important things you can do to protect your investment.

Let's break down the most common questions homebuyers, landlords, and even other professionals have about it.

Why Should I Care If My Surveyor Has PI Insurance?

As a homebuyer, this should be one of your top concerns. Think of it as your financial backstop if your surveyor gets something badly wrong.

Imagine you buy a house based on a survey that completely misses a £50,000 structural defect. The surveyor’s Professional Indemnity (PI) insurance is how you’d claim that money back. It's the fund set aside specifically for this kind of situation.

Without that insurance, your only real option is to sue the surveyor or their company directly. That's a notoriously long and expensive route, and there’s no guarantee they'd even have the funds to pay you if you won. A surveyor with proper PI cover isn't just following the rules of bodies like RICS; they're showing they are accountable for their work.

What Is the Difference Between 'Any One Claim' and 'In the Aggregate' Cover?

This is a really important detail that separates a great policy from a mediocre one. It all comes down to how much cover is actually available if things go wrong.

'Any One Claim' Cover: Sometimes called 'each and every claim' cover, this is the gold standard. It means the full policy limit is available for every single claim made. If a firm has a £1 million limit, the insurer could pay out on three separate, unrelated £1 million claims in the same year.

'In the Aggregate' Cover: This policy has a total pot for the year. A £1 million aggregate limit means the insurer will only pay a total of £1 million for all claims combined in that period. One large claim could wipe it out, leaving nothing for anyone else who was affected by a different mistake.

For something as significant as a property survey, 'any one claim' cover gives you far more security.

Is a Surveyor's Insurance Checked If My Estate Agent Recommends Them?

Honestly, you can't assume it is. While estate agents and solicitors have a duty of care when referring you, it’s highly unlikely they’ve sat down and scrutinised the surveyor’s insurance certificate. At best, they've probably just confirmed the surveyor says they have it.

This is where using a dedicated platform that independently vets every single professional comes in. When you find a surveyor through a pre-vetted network, you’re getting an extra layer of assurance that a simple referral can’t offer.

Key Takeaway: Using a service that independently verifies PI insurance gives you confidence that the professional is not just qualified, but also holds current and adequate cover. Even then, it’s always a smart move to ask for a copy of their insurance certificate for your own files.

What Is Run-Off Cover and Why Is It Important?

Run-off cover is a special type of PI insurance that professionals buy when they retire or close their business. It’s absolutely vital because PI insurance is what’s known as a 'claims-made' policy. This means the insurance must be active when a claim is made, not when the work was originally done.

Let's say a surveyor retires in 2026. In 2027, you discover a major defect that they missed on a survey they did for you back in 2024. You can only make a claim if that surveyor has active run-off cover in place in 2027. If they don't, you're left with no financial recourse for their past negligence.

Professional bodies like RICS make it mandatory for their retiring members to have run-off cover for at least six years. It’s another crucial part of the safety net, ensuring clients are protected long after a surveyor has hung up their tools.

At Survey Merchant, we understand that trust is built on accountability. That's why we meticulously verify the professional qualifications and PI insurance of every surveyor on our UK-wide panel, giving you complete confidence and peace of mind. Find your trusted, vetted surveyor today at https://www.surveymerchant.com.