Leasehold

Jul 16, 2026

Ultimate Guide to PI Insurance for Surveyors

Surveyors must secure adequate PI cover: this guide explains RICS rules, claims-made rules, run-off cover and how to avoid crippling claims.

PI insurance (Professional Indemnity insurance) is essential for surveyors in the UK. It protects against claims of financial loss caused by mistakes in advice, valuations, or services. Without it, surveyors risk significant financial exposure, as claims can reach hundreds of thousands of pounds. Key points include:

Surveyors must maintain continuous coverage, meet RICS standards, and tailor policies to their specific services to avoid financial vulnerability.

The Royal Institution of Chartered Surveyors (RICS) establishes the baseline for professional indemnity (PI) insurance across the surveying profession. Every regulated firm must secure cover from a RICS Listed Insurer. These insurers adhere to the Approved RICS Minimum Policy Wording and participate in the Assigned Risks Pool (ARP), which serves as a safety net for firms unable to obtain insurance on the open market, ensuring continuous coverage.

The minimum level of indemnity a firm must maintain is directly linked to its annual fee income:

| Annual Fee Income | Minimum PI Cover Required |

|---|---|

| £100,000 or less | £250,000 |

| £100,001–£200,000 | £500,000 |

| £200,001–£400,000 | £1,000,000 |

| £400,001–£600,000 | £1,500,000 |

| Above £600,000 | £2,000,000+ |

However, many firms exceed these thresholds to meet the requirements of lenders and clients.

Recent updates to RICS regulations include two key changes. From 1st July 2025, a formal two-stage cancellation process for non-payment will apply, involving a 30-day payment window followed by a 30-day notice period before a policy can be cancelled [3]. Additionally, firms must provide six years of consumer run-off cover if any part of the premium has been paid [3]. This run-off cover, which can cost 150%–300% of the final annual premium, is a critical consideration for succession planning.

While meeting RICS minimums is mandatory, surveyors must also navigate additional demands from clients and lenders.

Although RICS sets the minimum insurance standards, mortgage lenders and panel managers often require higher levels of cover, typically ranging from £2 million to £5 million, regardless of a firm's size or fee income [2]. This is especially relevant for surveyors conducting residential mortgage valuations, as the Financial Conduct Authority (FCA) also mandates sufficient PI cover under the Mortgage Credit Directive.

The risks are not hypothetical. For instance, a South London retail property was valued at £2.1 million for lending purposes but later sold for £1.68 million after the borrower defaulted, leaving the lender with a £420,000 loss. The claim was fully paid, along with £78,000 in associated defence costs [2]. Such cases highlight why lenders often demand more than the RICS minimums and why surveyors should treat these minimums as a baseline rather than a practical guideline.

Surveyors should also be cautious about signing contracts with uncapped liability clauses. Standard PI insurance policies only cover up to the policy limit, meaning any uncapped obligations in a contract could leave a firm financially exposed beyond what the insurer will pay [2].

Surveyors working in niche areas face unique insurance challenges. For example, party wall work and dilapidations often come with higher premiums due to the higher likelihood of disputes and the complexity of the legal framework [2]. Firms expanding into these areas should carefully review their PI cover before accepting new instructions.

Fire safety assessments, in particular, have specific insurance requirements. For buildings with four storeys or fewer, full civil liability cover is mandatory. However, for buildings with five storeys or more, RICS permits cover on a negligence-only basis, with a retroactive date of 1st July 2024, excluding work conducted prior to that date [4]. Additionally, surveyors performing Fire Risk Appraisals of External Walls (FRAEWs) on buildings up to 18 metres must complete the RICS external wall systems assessment training before insurers will extend coverage for this type of work [4].

"The changes reflect an improving outlook regarding the future of fire safety exposure and a wider improvement in risk appetite of insurers." - David Burnhope, Client Director, JMG Professional Risks [7]

To effectively manage risk, it's crucial for surveyors to understand what professional indemnity (PI) insurance actually covers. At its heart, PI insurance shields professionals from the financial fallout of errors made during their services. For example, this might include missing structural issues like subsidence or damp, or offering an incorrect property valuation that leads to a client's financial loss [2].

A standard PI policy typically includes legal defence costs. These can cover solicitor fees, barristers, and expert witnesses, which can quickly add up to anywhere between £50,000 and £150,000, even before a case goes to trial [2].

The coverage also extends to issues such as misrepresentation (offering misleading advice), breach of confidentiality, loss of documents, and defamation or accidental intellectual property infringement in professional reports [2][5].

"Professional indemnity insurance is the cornerstone policy for any chartered surveyor. It protects you against claims of negligence, errors, or omissions arising from your professional advice and services." - Thomas Winfield, Specialist UK insurance broker [2]

One important feature of PI insurance is the retroactive date, which determines how far back your cover applies, as long as there hasn’t been a lapse in insurance [8]. If you change insurers, it’s essential to ensure the new policy maintains the same retroactive date as the old one. This is particularly important under the Limitation Act 1980, which allows clients to file negligence claims up to six years after the error occurred - or even up to 15 years if the work was conducted under deed [2]. This means liability can linger long after a project is completed.

If there’s a gap in coverage, all prior work becomes unprotected. Additionally, if you suspect a potential claim, it’s critical to notify your insurer right away. Delaying until you receive a formal complaint could activate the "known circumstances" exclusion, leaving you without cover [2].

These mechanics underline the importance of understanding not only what PI insurance covers but also its limitations, as detailed in the exclusions below.

PI insurance does have its boundaries, and some common exclusions include:

Additionally, the policy won’t cover work performed outside your expertise. For instance, a residential surveyor taking on a complex commercial structural assessment without the necessary qualifications would not be protected [2]. Always review your policy details thoroughly before accepting assignments that lie outside your professional competence.

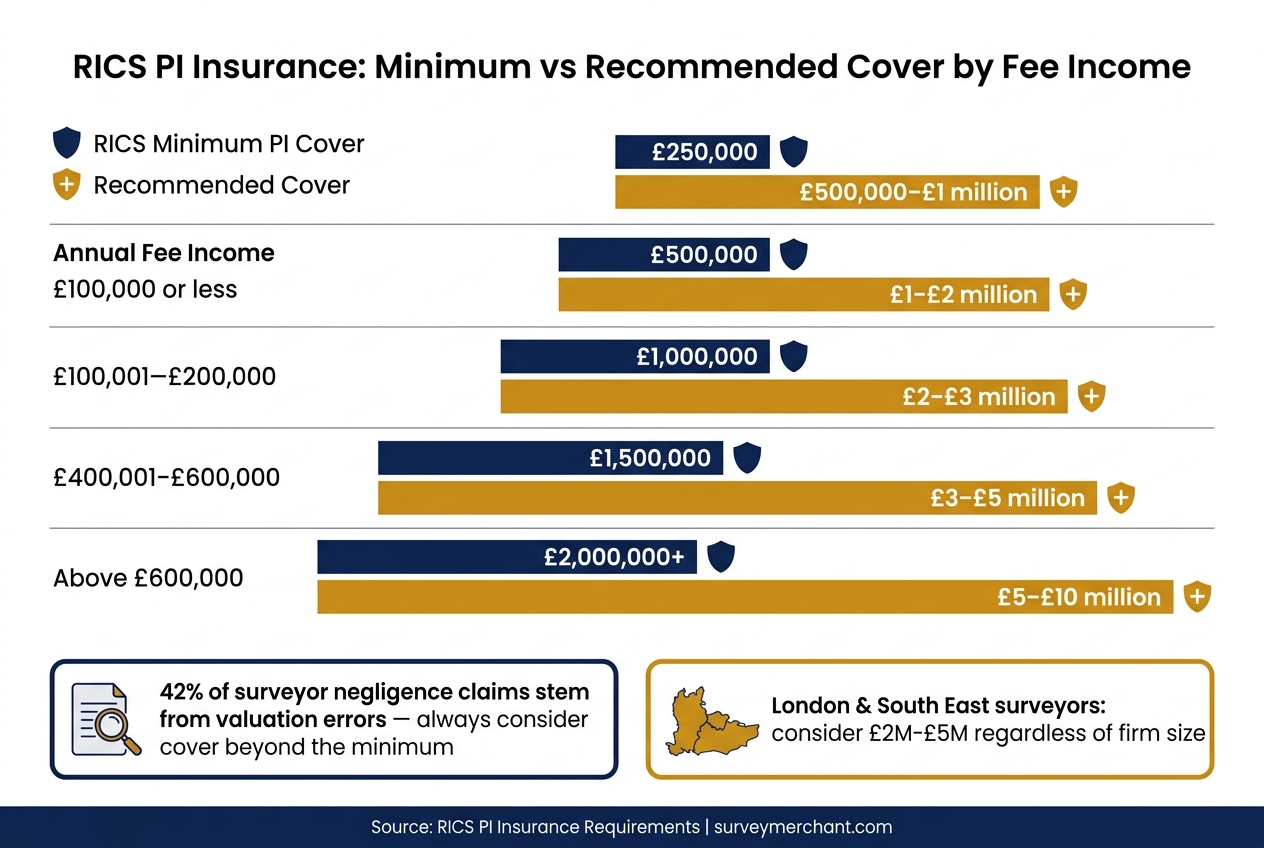

RICS PI Insurance: Minimum vs Recommended Cover by Fee Income

To start, it’s essential to understand the RICS mandatory minimums for professional indemnity (PI) insurance, which are directly linked to your annual fee income. For example, a sole practitioner earning under £100,000 annually must have at least £250,000 in cover. Meanwhile, a firm with fee income between £200,001 and £400,000 is required to hold a minimum of £1 million in cover. While these figures provide a baseline, many practices opt for higher limits to safeguard against larger potential losses.

| Annual Fee Income | Minimum PI Cover Required | Recommended Cover |

|---|---|---|

| £100,000 or less | £250,000 | £500,000–£1 million |

| £100,001–£200,000 | £500,000 | £1–£2 million |

| £200,001–£400,000 | £1 million | £2–£3 million |

| £400,001–£600,000 | £1.5 million | £3–£5 million |

| Above £600,000 | £2 million+ | £5–£10 million |

It’s also critical to consider your maximum potential loss per instruction. For instance, a chartered surveyor once faced a claim of £185,000 after failing to identify active structural movement in a £650,000 Victorian terrace. This amount covered repair costs, loss in property value, and legal fees [2]. For commercial work, these figures can climb even higher.

"A single commercial property valuation error can easily exceed £1 million in damages, especially for high-value assets in London and the South East." - Thomas Winfield, Specialist UK Insurance Broker [2]

Surveyors operating in areas like London and the South East should strongly consider cover ranging from £2–£5 million, regardless of their firm’s size, as the high property values in these regions significantly increase the likelihood of large claims [2].

Once you’ve determined your coverage needs, the next step is ensuring your policy aligns with the specific risks associated with the services you provide.

Not all surveying work carries the same level of risk, and your PI policy should reflect these differences. Insurers often categorise services by their risk levels. For example, residential letting and estate agency work are considered lower risk, while structural surveys, project management, and land surveying are higher-risk activities [1][9]. Among all services, valuation work stands out, as 42% of all surveyor negligence claims stem from valuation errors [2]. These mistakes can lead to severe consequences, with lender claims often exceeding hundreds of thousands of pounds when defence costs are factored in [2].

Surveyors conducting Red Book valuations for mortgage purposes must also comply with Financial Conduct Authority (FCA) requirements under the Mortgage Credit Directive, in addition to meeting RICS standards [2].

If your services include specialised areas like fire safety assessments, asbestos surveys, or environmental reports, it’s crucial to confirm that your policy explicitly covers these activities. Many standard PI policies exclude such services unless specific endorsements are added [2][3]. To manage costs, you might consider increasing your policy excess. A higher excess, typically ranging from £5,000 to £25,000, can reduce annual premiums by 15–35%. This option is often viable for lower-risk services where claims are less frequent [2].

After assessing your coverage needs and aligning them with your service risks, it’s worth considering how your practice integrates with platform-based work. Platforms like Survey Merchant connect clients with a nationwide panel of surveyors offering services such as Level 2 HomeBuyer Reports, Level 3 Building Surveys, Red Book valuations, party wall agreements, dilapidations, lease extensions, project management, and expert witness reports. If you work through such platforms, your PI cover must account for the entire range of services you provide via the platform.

Your indemnity limit should match the potential risk of each instruction, not just the overall profile of your practice. For instance, a surveyor who primarily handles residential HomeBuyer Reports but occasionally takes on commercial project management through a platform needs to ensure their policy covers such instructions and that the cover limit is sufficient for the value involved. Platforms like Survey Merchant require panel surveyors to maintain appropriate PI insurance to address the diverse risks associated with their services. Keeping your insurer informed about every type of service you offer is the easiest way to avoid gaps in coverage when they matter most.

Professional Indemnity (PI) insurance needs to be reviewed every year. This isn't just a formality; it's essential to maintain continuous claims-made coverage. With this type of policy, coverage must be active when a claim is filed, not just when the work was initially completed.

During each renewal, there are three crucial areas to examine. First, check that your indemnity limit matches your current fee income. If your turnover has increased, your RICS-mandated minimum may have risen too. Second, let your insurer know about any new services you've started offering, like asbestos surveys, contaminated land assessments, or high-value commercial valuations. These often require additional endorsements [2]. Third, ensure your policy complies with the RICS Minimum Policy Wording, which was updated on 1 July 2025. This update includes a revised definition of fire safety to cover internal wall components and introduces standardised cancellation clauses. These clauses allow members to cancel with 30 days' written notice under certain conditions, such as a firm merger or material risk changes [11]. Regular reviews like these can help you stay prepared and protected.

Taking proactive steps can significantly lower your risk of claims. Start by issuing written terms of engagement before any project begins. These should clearly outline the scope, limitations, and assumptions of your work. After every phone conversation, follow up with an email summary to create a reliable record. For properties valued over £500,000, ensure a peer review is conducted before finalising your report [2]. Also, keep detailed records, including survey notes, photographs, and correspondence, for at least 15 years. Secure digital backups are a smart way to safeguard these files, especially since the Latent Damage Act 1986 allows for extended limitation periods [2].

When reviewing client contracts, watch out for unlimited liability clauses. Agreeing to these could mean your insurer won't cover claims beyond your policy limits, leaving you personally liable [2]. Negotiate for net contribution clauses instead. Keeping thorough Continuing Professional Development (CPD) records is another good move. Insurers often reward evidence of ongoing competence with premium discounts of 5–15% [2]. Additionally, a claims-free history spanning five years or more can reduce your annual premiums by 10–25% [2].

Planning for risk management isn't just about day-to-day operations. It's also about preparing for the future, including the end of your practice.

Your PI obligations don't end when you retire, sell your firm, or close your practice. Claims can still arise from past work, and you'll need an active policy to handle them. RICS mandates a minimum of six years of run-off cover for firms that cease trading [2][10].

"If you cease trading and don't arrange run-off cover, you have zero protection for past work." - WS Insurance [2]

From 1 July 2025, the RICS Minimum Policy Wording ensures run-off cover automatically attaches for six years after a firm stops trading, even in cases of insolvency [11]. This change eliminates the need to notify insurers formally, offering better protection for consumers.

Budgeting for run-off cover is crucial. It typically costs 150–300% of your final year's premium [2]. The first year mirrors your last active-year rate, while subsequent years may decrease by 10–20% annually if no new claims are made [12]. If retiring from a partnership, get written confirmation that the continuing firm's policy will cover you for the required period [13]. To limit liability, use simple contracts instead of deeds, as these reduce the contractual liability period from twelve years to six [12].

"RICS requires surveyors to maintain PII for at least six years after they cease practising." - Alexandra Anderson and Jonathan Angell, Partners/Consultants, Reynolds Porter Chamberlain [13]

Surveyors in the UK must prioritise Professional Indemnity (PI) insurance. With over 40% of surveying firms encountering claims during their operations - often exceeding £75,000 - legal defence costs can quickly escalate, even before a case reaches trial [2].

To stay compliant and protected, ensure you maintain a claims-made policy with indemnity limits aligned to your fee income, as outlined by RICS. It's crucial to secure your policy through an RICS Listed Insurer that adheres to the Minimum Policy Wording. Additionally, notify your insurer whenever you expand your services to avoid gaps in coverage [3].

Operational diligence is another key to minimising risks. Equally important is planning for run-off cover when closing or merging your practice. RICS mandates six years of run-off protection, whether you're retiring, merging, or winding down. Since run-off cover can cost between 150–300% of your final year's premium, budgeting for this early will help you manage expenses effectively [2][3].

The indemnity limit your firm needs is tied to your annual fee income. According to RICS guidelines, the minimum levels of cover are as follows:

However, many surveyors opt for higher limits, sometimes reaching £10,000,000, to protect themselves against substantial financial risks. This includes not just claims but also the potentially hefty costs of legal defence.

To maintain protection under a claims-made policy, it's crucial to renew it without interruption. These policies only cover claims reported during their active period, meaning a lapse could leave you exposed for previous work. If your business ceases trading, consider obtaining fully retroactive run-off cover to protect against any future claims related to past activities. Be sure to inform your insurer before winding down operations to ensure a smooth transition in your coverage.

When you decide to retire or close your practice, it’s essential to keep your professional indemnity insurance active to cover any claims related to your past work. Since claims are dealt with on a claims-made basis, this coverage remains crucial even after your practice ends.

The Royal Institution of Chartered Surveyors (RICS) mandates that surveyors maintain run-off cover for a minimum of six years. To arrange this, inform your insurer about your plans so they can set up appropriate run-off terms. Additionally, it’s vital to keep your project records for at least six years, though holding them for 15 years is strongly advised to ensure you’re fully protected.

It’s always a good idea to speak with your broker to confirm that you’re meeting all the necessary requirements.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes