Valuation

Jul 16, 2026

Independent Property Valuation: Your 2026 Guide

Your 2026 guide to independent property valuation. Learn the process, costs, and how to choose a certified RICS valuer with Survey Merchant.

You might be staring at three different figures for the same property and wondering which one is real. An estate agent has suggested an asking price. A lender has arranged its own valuation. A solicitor, accountant, or family court process is now asking for a formal figure that can stand up to scrutiny. At that point, “roughly what it might sell for” isn't enough.

That's where an independent property valuation matters. If you're buying your first home, handling probate, negotiating a divorce settlement, disputing tax, or working out a lease extension, the value needs to be more than plausible. It needs to be impartial, evidence-based, and clearly explained.

The true extent of the difference is often underestimated. A simple price check helps you get a feel for the market. An independent valuation gives you a figure you can use in negotiations, legal proceedings, and regulated decisions. Its strength comes from one thing above all else: impartiality. When the valuer's role is to follow the evidence rather than chase a sale, please a lender, or support one side of a dispute, the report becomes a tool you can rely on.

A common example is probate. One sibling thinks the house should be sold quickly and priced keenly. Another believes it's worth much more because of the area, the garden, or improvements made over the years. An estate agent may give a marketing opinion, but if the figure is being used for tax, legal paperwork, or a future dispute, the family usually needs something more substantive.

The same problem appears in divorce cases. One party may suspect the other is relying on an optimistic or convenient figure. In a purchase, a buyer may worry that the agreed price reflects sales pressure rather than fair market evidence. In each case, the issue isn't just value. It's trust.

That's why independent valuation has such practical power. It gives everyone a shared reference point built from inspection, market evidence, and professional judgement.

An impartial valuation often reduces arguments because the discussion moves away from opinions and back to evidence.

People often confuse this with a survey, a lender's check, or an estate agent's estimate. They overlap, but they aren't interchangeable. A valuation answers a specific question: what is the property worth on the stated basis, for the stated purpose, at the stated date? A good report also shows how the valuer got there, what assumptions were made, and what factors may affect marketability.

If you're new to the process, the jargon can feel heavy. Terms like market value, special assumption, comparables, yield, and Red Book sound technical because they are. But the underlying logic is straightforward. A valuer inspects the property, studies the evidence, chooses the right method, and gives a single reasoned opinion.

That single, defensible figure is often your best protection in critical financial situations.

Independence isn't just a nice quality. It's the feature that gives the valuation weight.

Think of an independent valuer like a referee. The referee doesn't play for either side. Their job is to apply the rules, assess the evidence, and make a decision that can be justified. In property, that means the valuer's opinion shouldn't be driven by a sales target, a commission, or pressure from a party who wants the number to land in a particular place.

A valuation is independent when the professional giving the opinion is free to act objectively and explain their reasoning transparently. That matters most when people disagree or when the figure will be examined later by a lender, accountant, solicitor, court, tax authority, or auditor.

In the UK, this is strongly anchored by the RICS Red Book framework. As set out in the INREV summary of property valuation standards, Red Book valuations must be prepared by an independent valuer and state a single market value, rather than a range or a marketing estimate. That's especially important in regulated and audited contexts such as lending, taxation, probate, and matrimonial matters.

This is the point many readers miss. Independence doesn't mean the valuer has no opinion. It means their opinion is formed from evidence and professional standards, not from someone's preferred outcome.

Clients sometimes ask why the report can't say, “between X and Y”. In a casual conversation that might feel more realistic, but formal valuation practice usually needs one stated opinion of value at a specific date. A lender, solicitor, or court can't work with a vague range in the same way they can work with a properly reasoned figure.

That discipline becomes more important when the market feels uncertain. If buyer demand shifts, finance tightens, or sentiment changes quickly, a property's value can move. In those periods, a report grounded in evidence is far more useful than a hopeful estimate.

Practical rule: If the number may be challenged later, treat independence as a requirement, not a preference.

You can usually spot a properly independent approach by these signs:

That's why an independent property valuation is far more than a price opinion. It's a professional judgement designed to stand up when someone asks, “How did you arrive at that figure?”

Most confusion starts because different property professionals use the word “valuation” to mean different things. A homeowner hears one figure from an agent, another from the lender's valuer, and a third from an independent surveyor, then assumes one of them must be wrong. Often, they're doing different jobs.

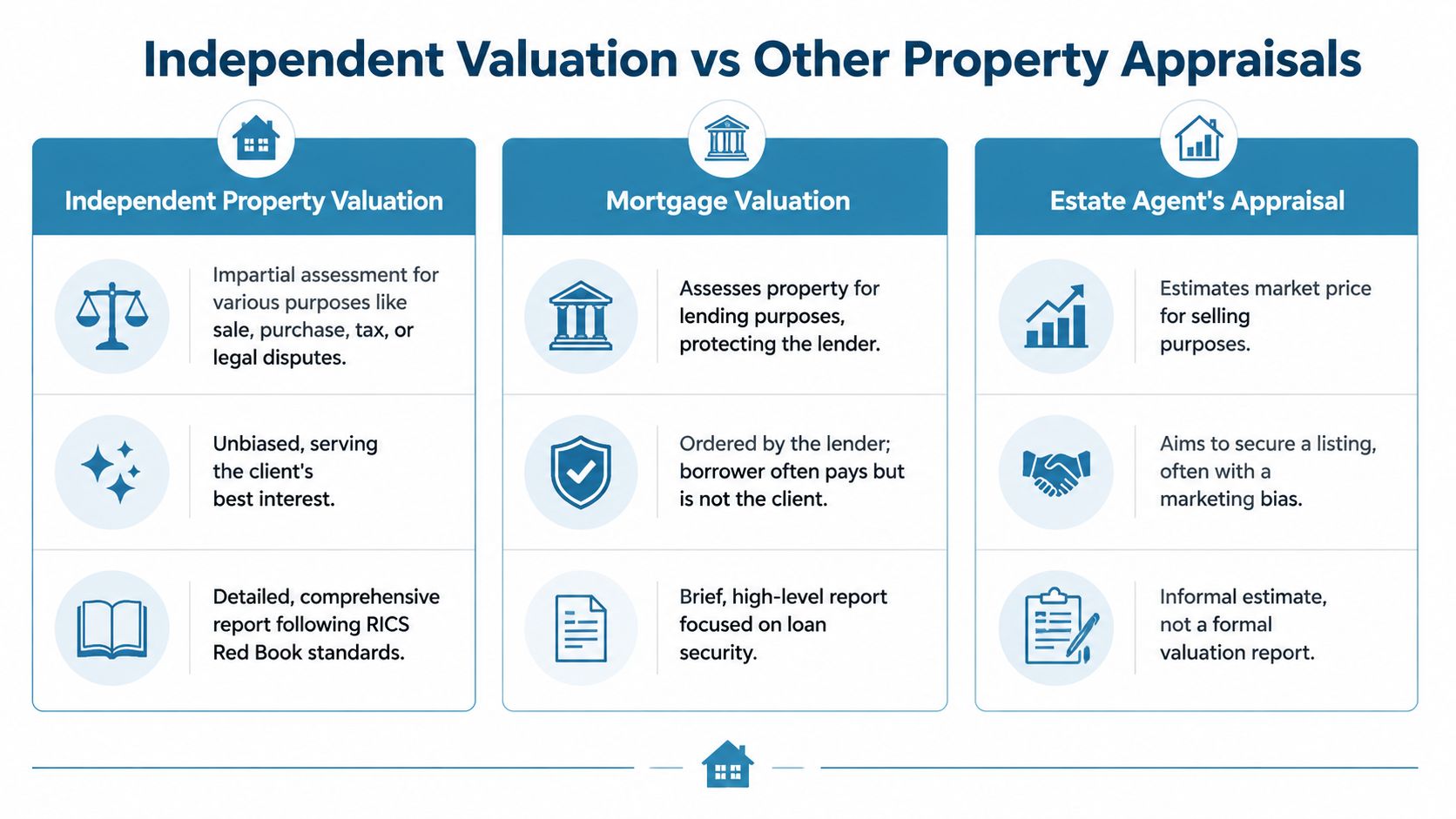

An estate agent's appraisal is usually about marketing. It helps decide an asking price and sales strategy. The agent may know the local market very well, but the purpose is to win instructions and generate interest from buyers.

A mortgage valuation is usually for the lender's benefit. The borrower often pays for it, but the report is there to help the lender judge the property as security for the loan. It isn't the same as a full survey, and it isn't necessarily designed to support your legal or tax position.

An independent property valuation is different because its role is to provide an impartial opinion for a defined purpose. That purpose might be probate, divorce, tax, shared ownership staircasing, leasehold work, or a pre-sale decision where you want a neutral benchmark.

If you're comparing remote and in-person options, this overview of desktop property valuations UK can help clarify where a desktop instruction may fit and where a full inspection matters more.

| Feature | Independent Valuation (RICS) | Mortgage Valuation | Estate Agent Appraisal |

|---|---|---|---|

| Primary purpose | Formal opinion of value for a stated purpose | Assess suitability as loan security | Suggest likely marketing price |

| Who it serves | The instructing client and the stated purpose of the report | The lender | The seller, with a marketing focus |

| Independence | Built around impartial professional judgement | Limited by the lender's brief | Can be influenced by instruction-winning |

| Report detail | Usually structured and reasoned | Usually brief and high level | Usually informal |

| Legal or dispute use | Often suitable where evidence is needed | Limited outside lending context | Not a substitute for formal valuation |

| Condition focus | Relevant as it affects value | Limited to lending risk | Often secondary to saleability |

A simple way to remember it is this:

If you need leverage in a negotiation, the most useful figure is usually the one least tied to anyone's sales incentive.

That impartiality can change the tone of a discussion. Instead of debating whose estimate sounds more convincing, you're working from a report that explains method, assumptions, and evidence.

Some situations leave room for a rough market view. Others don't. If the figure affects tax, court papers, a formal settlement, or a legal right, an independent valuation is usually the sensible route.

Take probate. Executors need a supportable figure for the property at the relevant date, not a sales pitch. If you're dealing with HMRC paperwork or trying to avoid later disagreement between beneficiaries, a formal opinion is far safer than relying on informal estimates. For readers handling that process, this guide to Estate valuation for Inheritance Tax gives useful context on why the valuation basis matters.

In divorce or matrimonial proceedings, the issue is fairness. If one side produces a high estimate and the other side produces a low one, the dispute can drag on. An independent valuation gives both parties a neutral starting point.

For lease extensions, enfranchisement, and shared ownership staircasing, the property figure can directly affect what someone pays or receives. The same applies in some tax matters, including calculations where the property value has to be justified rather than guessed.

For broader context on standards and report expectations, it's worth reading a 2026 Red Book valuation guide.

When value is contested, the report does more than provide a number. It creates a framework for discussion.

A first-time buyer can also benefit. If you're purchasing an unusual property, one with limited comparable evidence, or one where family members are contributing funds and want reassurance, an independent property valuation can help anchor the deal in reality.

That's why these reports matter beyond legal formality. They give you a defensible basis for decisions when the cost of getting the value wrong could be emotional, financial, or both.

For many clients, the most unsettling part is not knowing what happens between instruction and the final report. In reality, the process is orderly. A valuer doesn't walk through the front door, glance around, and invent a figure.

Here's the process in a practical sequence.

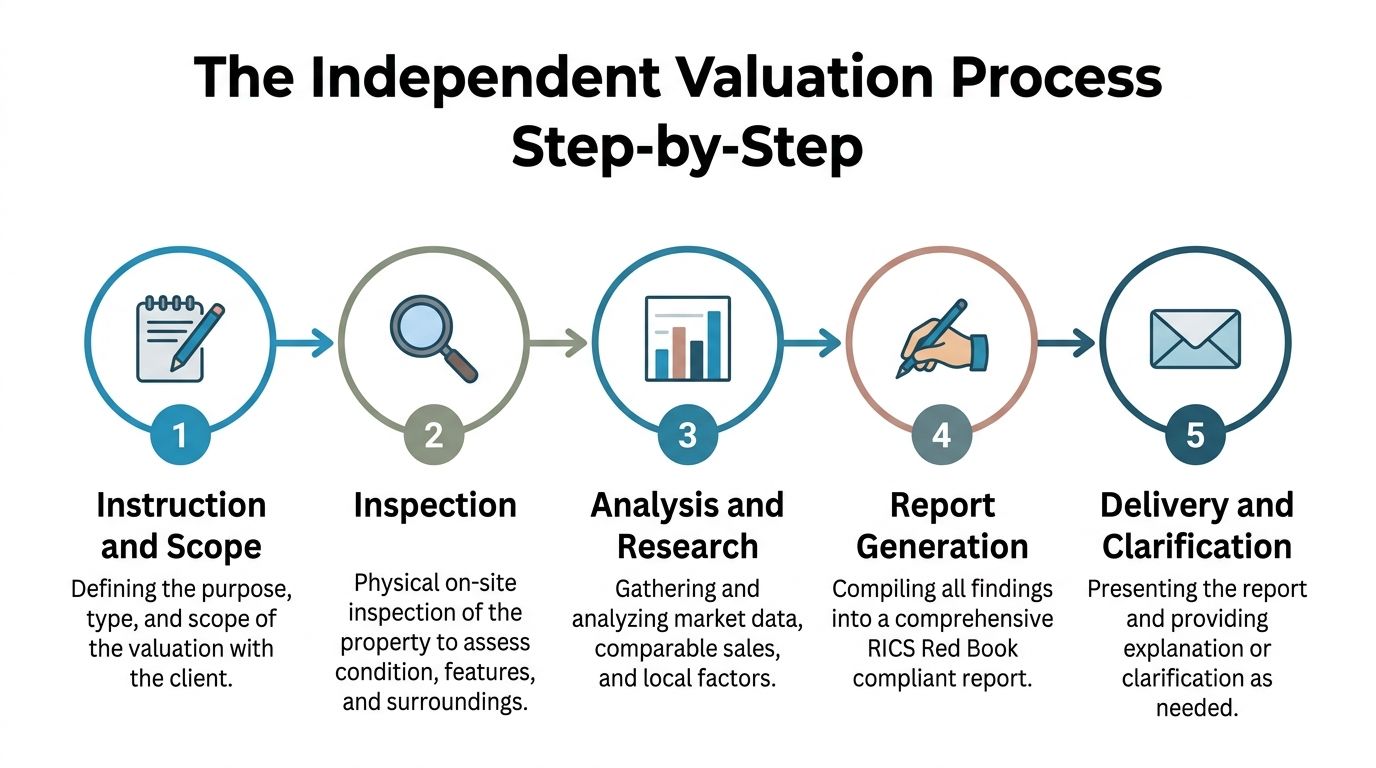

Instruction and scope

The valuer first needs to know the purpose of the report. Probate is different from matrimonial work. A tax valuation may require a different emphasis from a valuation for negotiation before sale. The instruction should pin down the property, the client, the purpose, the valuation date, and any special assumptions.

Desktop research

Before the inspection, the valuer gathers background information. That can include title details, planning context, location analysis, and available market evidence. This stage helps frame the inspection and highlights issues that may need closer attention on site.

Inspection

The valuer visits the property and records what exists. Size, layout, condition, accommodation, construction, location, outlook, access, and obvious defects can all affect value. A good inspection also checks whether the property matches the assumptions the market would make about it.

A short explainer can help if you want to see the process in action:

After inspection comes the analytical work. As explained in Dealpath's summary of real estate appraisal methods, valuers primarily rely on three evidence-based approaches: the sales comparison approach, the income approach, and the cost approach. Comparable sales are most useful where there's liquid market evidence. Income is central for income-producing property. Cost is often relevant for specialised assets where direct comparables are less helpful.

That choice of method matters. The same property can look different depending on whether it's owner-occupied, investment-led, or specialised. An independent valuer must justify the method against the property's use and the evidence available.

A sound valuation is not just about the answer. It's about whether the route to the answer makes sense.

The valuer weighs comparable evidence, adjusts for differences, considers market tone, and reconciles the evidence into a conclusion. Such a process requires professional judgement.

Final report

The report records the instruction, assumptions, method, market commentary, and concluded figure. It should be clear enough that a solicitor, accountant, lender, or informed client can understand how the valuation was formed.

The process feels less mysterious once you see the logic. Every stage exists for one reason: to make the final opinion explainable.

Choosing the right valuer is not just a box-ticking exercise. If the report will influence a negotiation, tax return, or legal outcome, the person behind it matters as much as the process.

Start with RICS membership and valuation competence. In UK practice, that's the clearest sign that the valuer is working within recognised professional standards. You should also check that they regularly handle the kind of instruction you need. Probate work, leasehold matters, matrimonial cases, and standard purchase valuations aren't identical.

A second check is Professional Indemnity insurance. If someone is giving you an opinion that could affect major financial decisions, they need the appropriate cover.

Third, look for local market understanding. Valuation is evidence-based, but evidence still needs interpretation. Two streets that look similar on a map can behave differently in the market because of school catchments, road noise, parking pressure, lease terms, layout, or buyer profile.

As noted in this academic discussion of valuation objectivity and transparency in contested cases, professional standards and transparency around valuation independence matter because small assumption differences can have a meaningful effect in high-value or disputed matters. That's one reason to spend time on choosing the right property valuer.

You don't need to interrogate the valuer, but a few practical questions are worth putting on the table:

A good valuer won't be evasive. They should be able to explain the process in plain English, state the fee clearly, and tell you where the limits of the report are.

That clarity is part of independence too. The less opaque the process feels, the easier it is to trust the result.

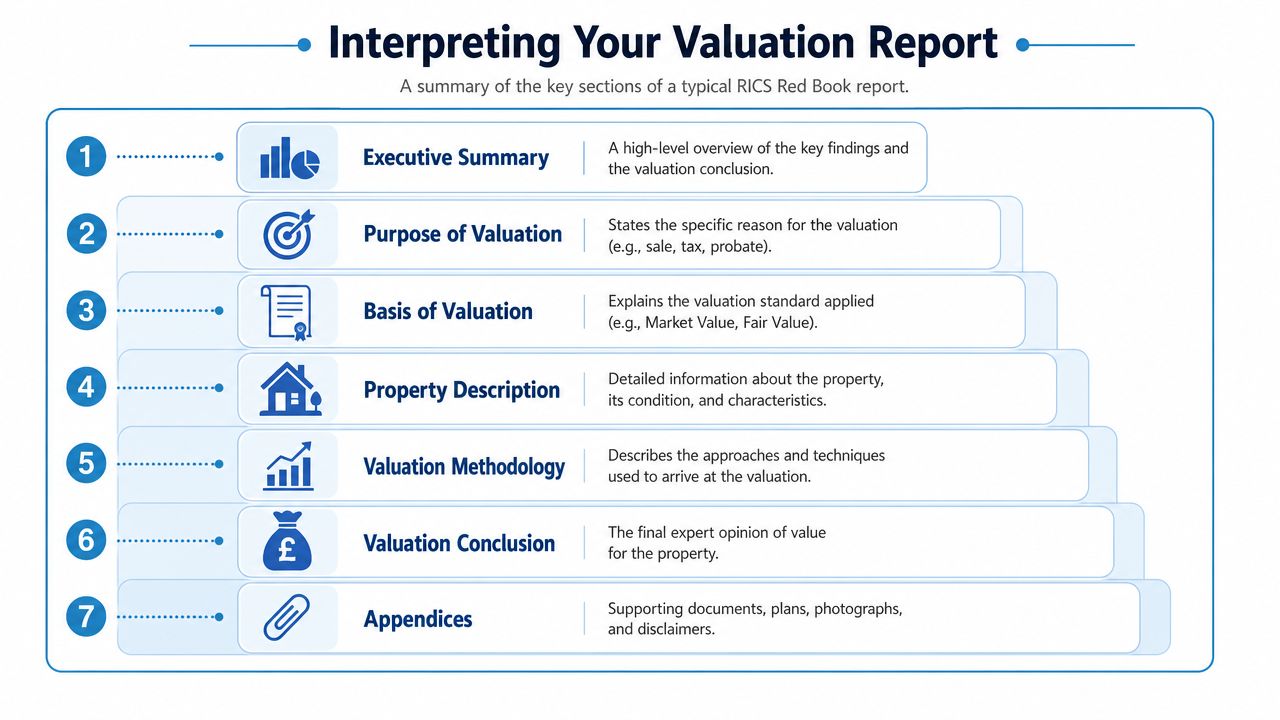

When the report arrives, recipients often turn straight to the final figure. That's understandable, but it's not the best place to start. The value only makes sense when you read it alongside the basis, assumptions, and commentary that support it.

Look first for the purpose of valuation. A report prepared for probate may not be framed in quite the same way as one prepared for negotiation before purchase.

Then check the basis of valuation and the valuation date. Those two details are essential. Value is always tied to a defined basis and a point in time.

After that, read the assumptions and any special assumptions carefully. Clients often skim this part, yet it can materially affect the conclusion. If the report assumes the property has no hidden defects, vacant possession, or a certain legal position, you need to understand that.

The methodology and market commentary show how the valuer reasoned through the evidence. This is the part that gives the number its authority.

A strong report should also reflect modern risks that affect marketability and future value. One area that deserves more attention is climate risk. The Lincoln Institute notes that around 6.3 million properties in England are at risk of flooding from rivers, the sea, or surface water, and that valuation should consider how flood exposure and insurability affect current marketability and future value, as discussed in this analysis of land valuation and climate-related risk.

That doesn't mean every property in a risk area is automatically blighted. It means a careful valuer should think about how buyers, lenders, and insurers may react.

Read the report like evidence, not like a brochure. The useful parts are often in the assumptions and commentary, not just the bold number at the end.

If you're wondering what improvements may support value before a future sale, this practical guide on how to find high-value home upgrades is a sensible companion read. Just remember that improvements don't always add pound-for-pound value, and some works mainly improve saleability rather than headline price.

If anything in the report looks unclear, ask. A valuation should be technical, but it shouldn't be impenetrable.

Fees vary by property type, location, purpose, and complexity. A straightforward flat for private decision-making will usually differ from a valuation for probate, dispute work, tax, or leasehold matters. The right way to think about cost is not “What is the cheapest report?” but “What level of evidence do I need this report to provide?”

There isn't a universal expiry date that fits every case. Value is always tied to the valuation date, and markets can move. If the report is being used later, especially in a shifting market or a contested matter, your solicitor, lender, accountant, or adviser may ask whether an update is needed.

Start by reading the assumptions, property details, and basis of value. Many disagreements come from factual issues, missing information, or misunderstanding the purpose of the report. If you still have concerns, raise them calmly with the valuer and provide any relevant evidence. In some cases, a review or a second independent opinion may be appropriate.

Yes. Sellers often do this when they want a neutral figure before setting an asking price, handling a family transaction, or preparing for a sensitive sale. It can also help where there's likely to be disagreement between co-owners or beneficiaries.

No. A valuation answers the question of value for a stated purpose. A building survey focuses on condition, defects, repair, and risk. The two can inform each other, but they are not the same service.

Not in the way many first-time buyers assume. The lender's valuation is primarily for the lender's lending decision. If you need a valuation that serves your own negotiation, legal, or tax position, you should consider your own independent instruction.

If you need a formal valuation from a qualified professional, Survey Merchant connects property owners, buyers, and advisers with a nationwide panel of surveyors for impartial, clearly explained reports across residential and commercial property.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes