You're often asked for a property value at the exact moment you haven't got time to wait. A lender wants to progress a remortgage. A solicitor needs a figure for probate. You want to sense-check an asking price before committing to a purchase. In each of those situations, the same question comes up: do you need someone to visit the property, or can a valuer reach a reliable opinion from a desk?

That's where desktop property valuations come in. They can be useful, practical and entirely appropriate in the right circumstances. They can also be the wrong tool if the property is unusual, altered, tired, or too uncertain to judge from records and imagery alone.

For first-time buyers and homeowners, the confusion usually starts here. People hear “desktop” and assume it means either a rough online estimate or a second-rate shortcut. Neither is quite right. A proper desktop valuation is a professional judgement. But it is still a judgement made without going inside the property, and that limitation matters more than many borrowers realise.

If you're still getting your bearings, this broader piece of advice for UK homebuyers on valuations gives useful context on how valuations fit into the buying and lending process.

Table of Contents

- An Introduction to Desktop Valuations

- The human expert still matters

- The core assumption behind the method

- The evidence a valuer usually reviews

- What the valuer is actually doing with that data

- Why desktop evidence can still mislead

- The clearest side-by-side view

- Where buyers often get caught out

- Some instructions should not stay desktop

- Common situations where desktop works well

- The purpose matters as much as the property

- When formality matters

- Property types that are poor candidates for desktop-only valuation

- Why these homes are harder to judge remotely

- When a physical inspection becomes necessary

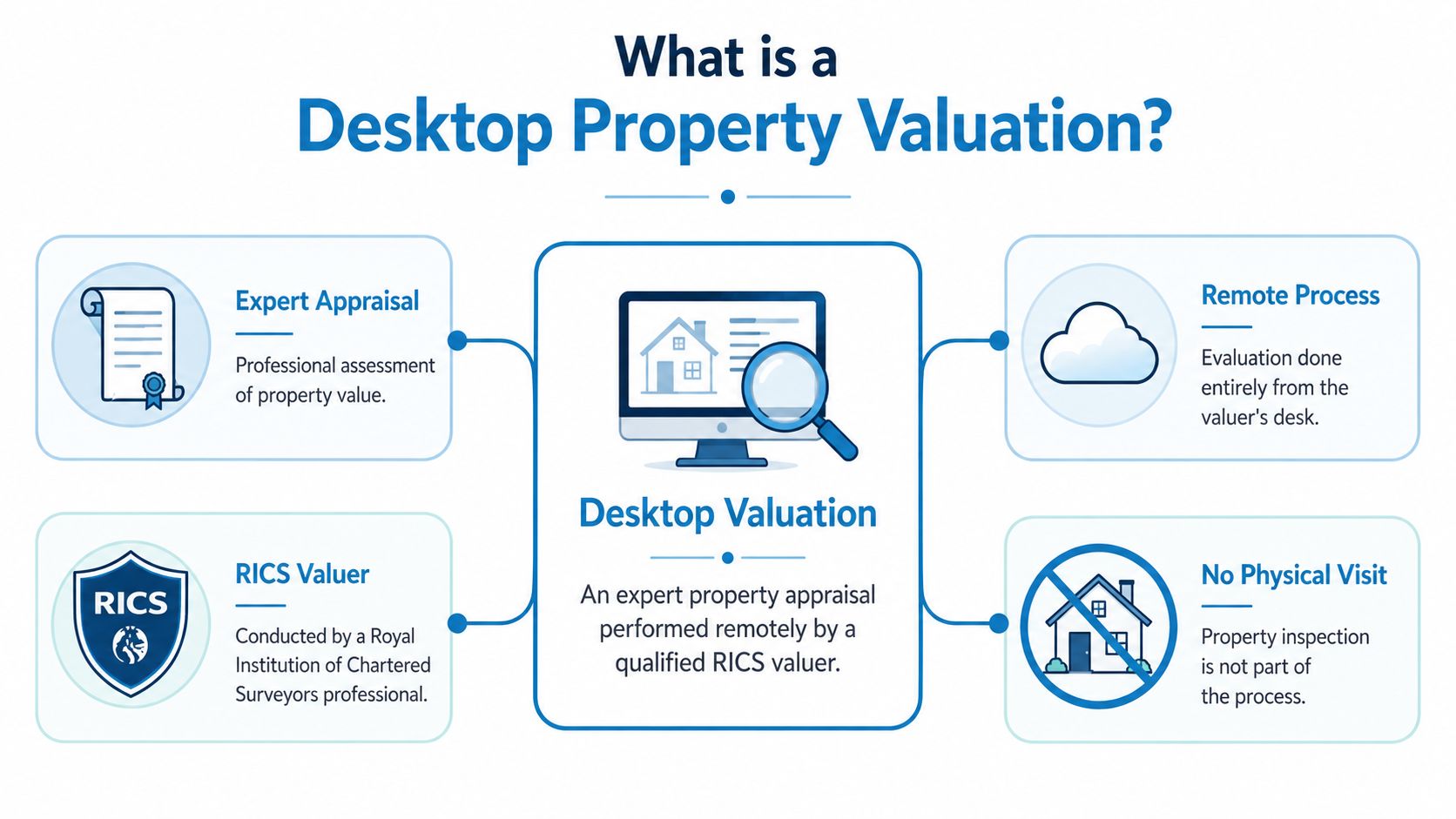

An Introduction to Desktop Valuations

You are remortgaging a 1930s semi. The lender says a desktop valuation may be enough, which sounds convenient until you remember the rear extension, the loft room added years ago, and the patch of damp hidden behind fresh paint. A desktop valuation can be quick and sensible, but only if the paperwork, photos and market evidence still match the property as it stands today.

A desktop valuation is a remote opinion of value based on records and comparable evidence rather than a site visit. The valuer reviews sources such as Land Registry data, past sale details, mapping, planning history, listing photographs and local market evidence, then weighs whether that material is good enough to support a reliable figure.

It helps to picture the process like valuing a car from its registration history, mileage records and sales adverts, without opening the bonnet. You can often get close on a standard model with a clear history. You can also miss the accident damage, poor repairs or modifications that change what a buyer would really pay.

That distinction matters in the UK because many homes are not standard. A modern flat on a well-documented development may suit a desktop approach far better than a listed cottage, a heavily altered terrace, a non-standard construction house, or a property with obvious signs of disrepair. In those cases, the risk is simple. The records may describe one property while the buyer, lender or surveyor is really dealing with another.

A desktop valuation also does a narrower job than many first-time buyers expect. It gives an opinion on market value on stated assumptions. It does not confirm condition, workmanship, layout changes, hidden defects, or whether improvements have the approvals they should have.

For a homeowner or remortgager, that is the practical point.

If the property is unusual, altered, in poor condition, hard to compare, or likely to have defects that photos and databases will not show properly, a physical inspection is usually required. For broader advice for UK homebuyers on valuations, it helps to understand where desktop assessments fit and where they stop being reliable. Readers dealing with shops, offices or mixed-use buildings should also note that residential desktop methods are not the whole picture. This guide to commercial real estate valuation explains how valuation approaches differ for commercial assets.

What Is a Desktop Property Valuation

A desktop property valuation is a professional valuation carried out remotely by a qualified valuer, usually without entering the property. Think of the valuer as a data detective. They gather pieces of evidence from different places, check whether those pieces agree, and then form a reasoned opinion on market value.

What it is not is a casual online estimate produced with no human judgement. A proper valuation still depends on an experienced professional deciding which comparables matter, which records are reliable, and which warning signs suggest the result may be too uncertain without a visit.

A professional valuation that trades a physical inspection for in-depth data analysis.

The human expert still matters

Readers often get the wrong idea. Because technology supports desktop valuations, some assume the process is fully automated. It isn't. A model can pull together data, but it can't think like a surveyor. It can't notice that one comparable sale looked high because of an exceptional refurbishment, or that an “extra bedroom” may in fact be a compromised loft conversion.

A valuer's role is to interpret, not just collect.

For readers who deal with mixed-use or investment assets as well as homes, this broader guide to commercial real estate valuation is useful because it shows how valuation method changes with property type, evidence and risk.

The core assumption behind the method

A desktop valuation works best when the property is standard, well-documented and predictable. The less guesswork involved, the stronger the result. The more the valuer has to assume about layout, condition or specification, the more cautious everyone should be.

That's why desktop property valuations are often acceptable for straightforward lending decisions but less suitable for disputes, unusual homes or cases where the interior condition could materially change value. If the method depends on records rather than direct observation, then the quality of those records becomes central.

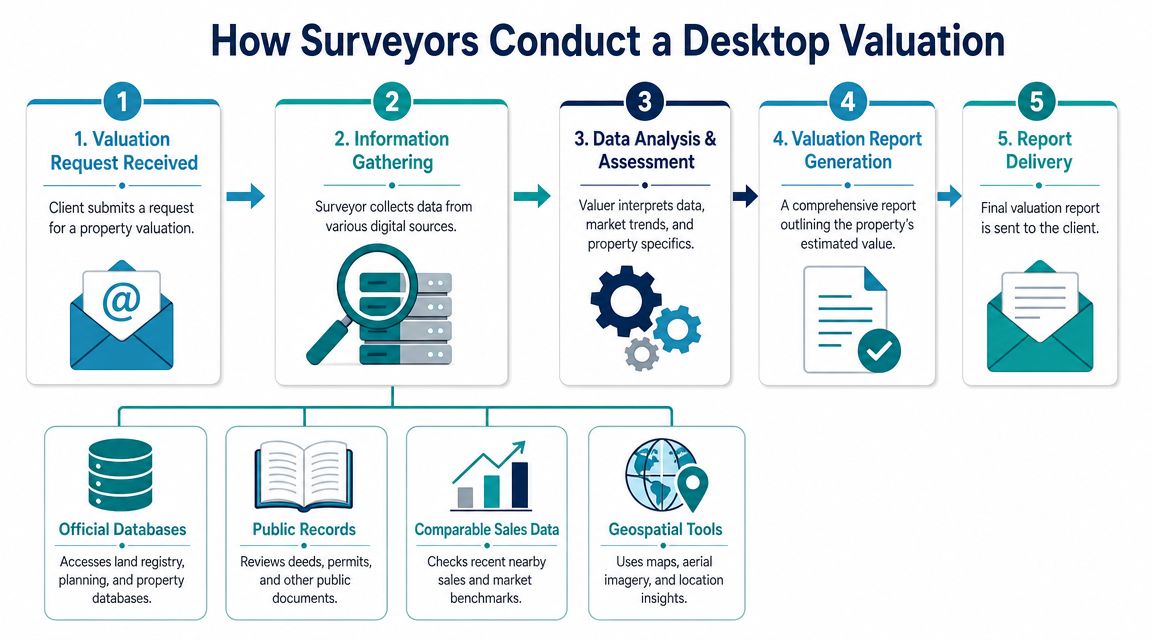

How Surveyors Conduct a Desktop Valuation

A desktop valuation looks simple from the outside. In practice, the valuer is cross-checking several streams of evidence and trying to answer two separate questions at once. First, what does the market suggest this property is worth? Second, is there anything about this property that makes the normal evidence less dependable?

The evidence a valuer usually reviews

Most desktop assignments start with the basic identifiers: address, tenure, property type and known history. From there, the valuer will typically draw on sources such as:

- Land Registry records for past sale prices and transaction dates.

- Comparable local sales to judge how similar homes have been valued by the market.

- Property portal archives such as historic listing details, photographs and prior marketing descriptions.

- Street View and satellite imagery to assess setting, access, surrounding development and external appearance.

- Third-party datasets and digital valuation tools where these support the valuer's analysis.

The UK lender guidance summarised in Advisewise's desktop valuation document describes a desktop valuation as a remote valuation completed from publicly available and third-party data, supported by a RICS risk-managed, data-enabled digital valuation tool. The same guidance also makes the key limitation clear: if the subject property has limited transaction history, unusual specifications, or weak comparable evidence, reliability falls because the model cannot directly verify condition, layout or unrecorded defects.

What the valuer is actually doing with that data

This isn't a box-ticking exercise. A good valuer asks questions like:

| Question | Why it matters |

|---|---|

| Does the sale history make sense? | A stale or odd transaction history may distort expectations. |

| Are the comparables genuinely similar? | A nearby sale isn't helpful if its condition, size or appeal differs materially. |

| Do the photos and mapping align? | If archives show features that current imagery doesn't, the property may have changed. |

| Is anything missing? | Missing floor plans, sparse history or vague descriptions increase uncertainty. |

Why desktop evidence can still mislead

Suppose a two-bedroom flat sold well because it had been renovated to a very high standard. The listing photos looked immaculate. If your subject flat in the same block has an outdated kitchen, water staining and poor flooring, the paper trail may not reveal that difference. The valuer can adjust where the evidence supports it, but only up to a point.

Practical rule: the desktop process is strongest when the available evidence tells a consistent story. It weakens when the story has gaps.

That is the central discipline of desktop property valuations. The surveyor isn't merely collecting facts. They're judging whether the facts are complete enough to trust.

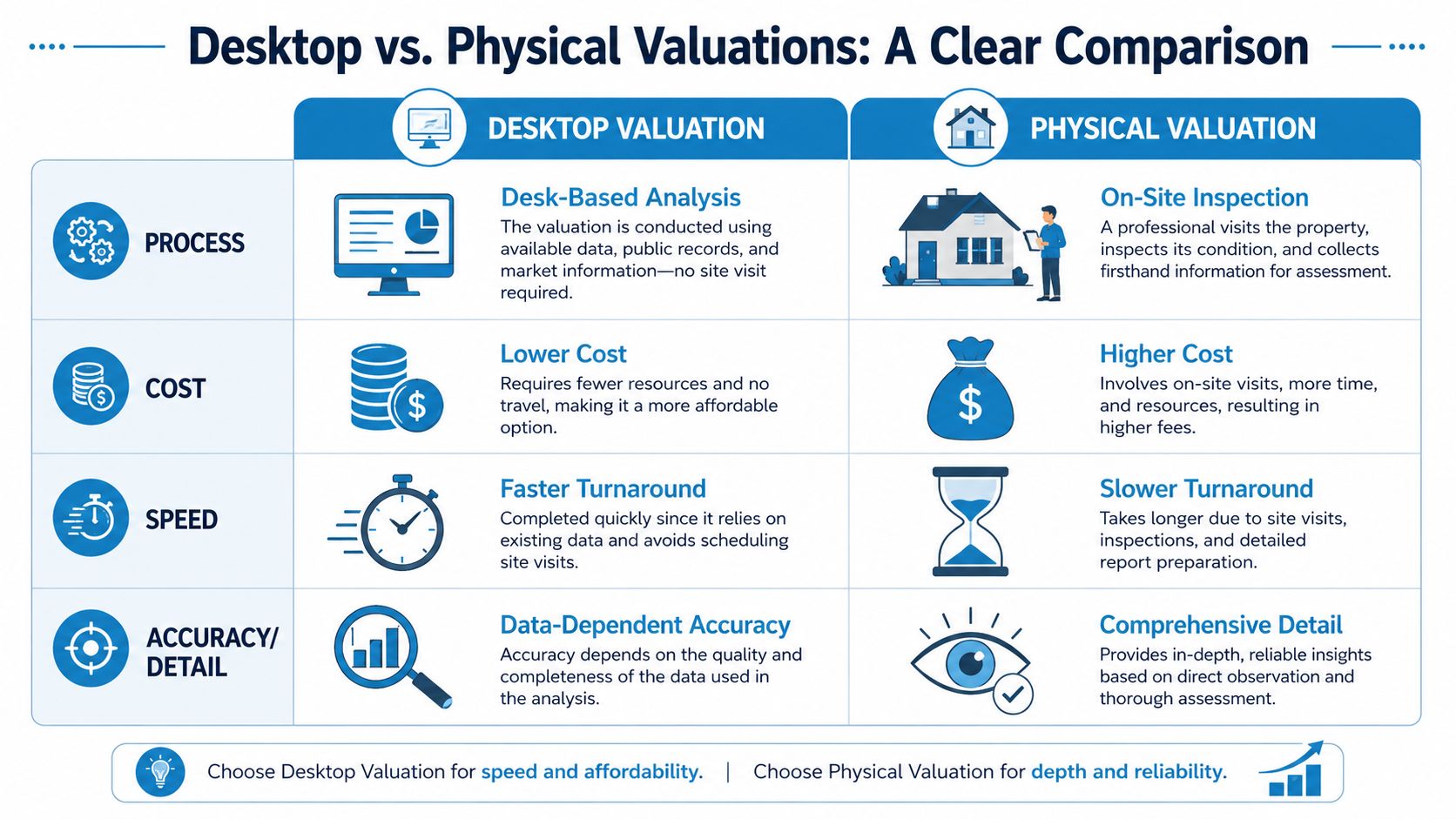

Desktop vs Physical Valuations A Clear Comparison

If you strip the jargon away, the difference is simple. A desktop valuation estimates value from evidence about the property. A physical valuation estimates value from evidence about the property and direct observation of it.

The trade-off is speed versus certainty.

The clearest side-by-side view

| Factor | Desktop valuation | Physical valuation |

|---|---|---|

| Process | Desk-based analysis using records, imagery and sales evidence | On-site inspection plus market analysis |

| Speed | Usually quicker because access and travel aren't needed | Usually slower because inspection must be arranged |

| Cost | Usually lower because the work scope is narrower | Usually higher because the inspection takes more time |

| Certainty | Limited by what can't be seen inside | Stronger because condition and layout can be checked directly |

| Best fit | Standard, low-risk properties with good data | Unusual, altered, older or condition-sensitive properties |

A short visual explanation can help if you want to see the same distinction in another format.

Where buyers often get caught out

First-time buyers sometimes assume a lender's valuation is there to protect them. It isn't the same as a condition survey. A desktop mortgage valuation may satisfy the lender's underwriting needs while telling you very little about hidden defects.

That's why a property can be “good enough” for a lending decision and still be a poor purchase if the building itself has problems. The lender is asking whether the property is acceptable security. You are asking whether you're buying trouble.

For a useful parallel from another market, this buyer's guide to French real estate condition shows how strongly condition evidence affects confidence, regardless of country. The principle is the same. When physical state matters, remote review has limits.

Some instructions should not stay desktop

Leasehold work is one example where the method can become more nuanced. If you're dealing with specialist leasehold matters, this piece on inspection vs desktop for lease extensions shows why some instructions can't be reduced to a simple desk exercise.

A physical valuation becomes the safer option where internal condition, alterations, accommodation, repair issues or non-standard construction may materially affect value. In those cases, a visit isn't an optional extra. It's part of getting the answer right.

When to Use a Desktop Valuation

Desktop property valuations make most sense when the property is straightforward and the purpose doesn't demand a high level of investigative detail. The easiest way to judge suitability is to think about what's at stake and how much uncertainty the client or lender can reasonably tolerate.

Common situations where desktop works well

A remortgage is the classic example. The lender wants an opinion of value to support a lending decision, but the property may already have a known history and the transaction itself may be relatively simple. If the home is conventional and the available market evidence is strong, a desktop approach can be perfectly sensible.

Probate can also be suitable in many cases. Executors often need a properly reasoned valuation for administration purposes, but they may not need the fuller investigative scope that comes with an inspection, especially where the property is ordinary and the records are clear.

A homeowner may also want a professional market figure before a sale, a transfer between family members, or a broader financial decision. In those situations, the speed and lower friction of a desktop instruction can be helpful.

The purpose matters as much as the property

The same house may be suitable for a desktop valuation in one context and unsuitable in another.

- Remortgage on a standard estate home: often a reasonable desktop candidate if the data is clean.

- Probate for a conventional flat: often workable if there's reliable comparable evidence.

- Dispute or negotiation over value: usually calls for greater scrutiny and a stronger audit trail.

- Purchase of a house you haven't lived in: much more caution is needed, because you don't know the condition first-hand.

The right question isn't “Can this be done from a desk?” It's “What would be missed if no one visits?”

When formality matters

Some clients also need a valuation prepared to recognised professional standards, rather than an informal estimate. In those cases, the scope and basis of valuation need to be clearly set out from the start. If that's relevant to your situation, Survey Merchant's Red Book valuation advice is a sensible place to understand the formal framework before ordering anything.

Desktop valuation is a method, not a shortcut. Used in the right setting, it saves time and effort. Used in the wrong setting, it stores up arguments for later.

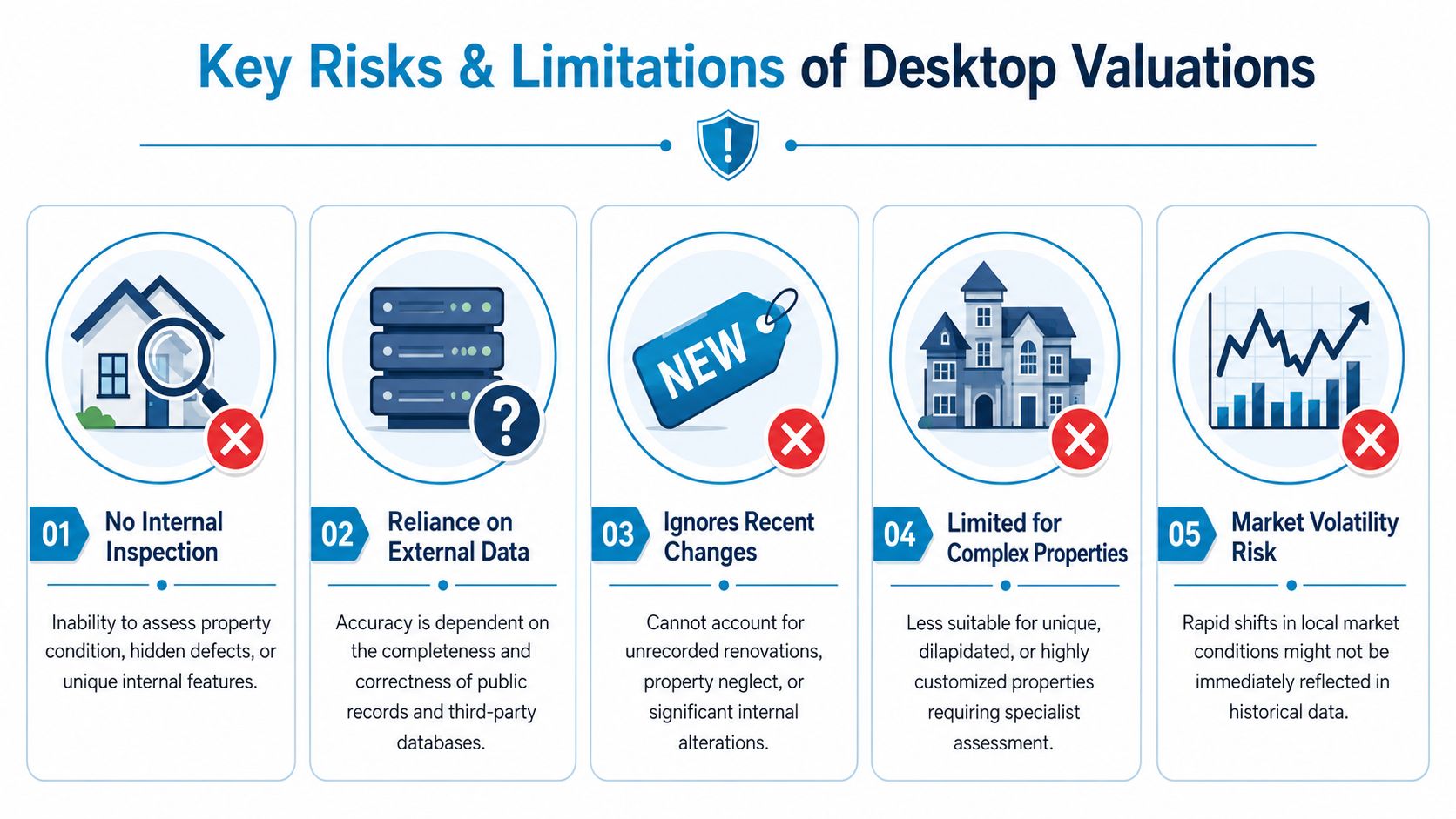

Key Risks and Accuracy Limitations

A desktop valuation can work well for the right property. It can also miss the very thing that makes a property worth more, or less, than the surrounding evidence suggests.

The reason is straightforward. The surveyor is valuing with one eye covered. Land Registry records, EPC data, listing history, mapping, planning records and comparable sales all help, but none of them replaces walking through the front door. A desktop figure therefore depends on assumptions about condition, quality of finish, alterations, repair, and sometimes even how the accommodation flows in practice.

That matters because value is not created by square footage alone. Two houses with the same floor area on the same road can differ sharply in value if one has dated electrics, a poor-quality extension, damp concealed behind fresh paint, or a loft conversion that looks acceptable online but feels compromised on site.

Property types that are poor candidates for desktop-only valuation

For many standard flats and estate houses, desktop evidence can be good enough. For the following property types, caution should rise quickly because the risk of a wrong assumption is much higher:

- Older homes, especially pre-war properties, where movement, damp, timber decay, outdated services or piecemeal repairs may not be visible in records.

- Listed buildings and period properties, where value depends heavily on original features, sympathetic repairs, and whether alterations have been carried out properly.

- Non-standard construction, such as concrete, steel frame, timber frame, cob, thatch or other uncommon forms, where mortgageability and saleability can vary.

- Heavily extended, converted or reconfigured homes, because plans, photos and official records do not always match what exists on site.

- Properties in poor or uncertain condition, including homes with visible neglect, unfinished works, suspected leaks, mould, cracking or long-term vacancy.

- High-value, one-off or architect-designed homes, where there may be few comparable sales and small differences in quality can shift value materially.

- Flats or houses with suspected unauthorised alterations, particularly where walls have been removed, garages converted, or outbuildings turned into living space without clear paperwork.

These are the cases where a desktop valuation is most likely to be led astray by tidy data and incomplete reality.

Why these homes are harder to judge remotely

A desktop valuation works a bit like pricing a used car from registration records, old photos and recent sales of similar models. You can get close if the car is standard and well documented. You can be badly wrong if it has hidden rust, a poor repair, missing service history or modifications that change what buyers will pay.

Property is the same. UK housing stock is full of exceptions.

A Victorian conversion may have charming ceiling heights but weak sound insulation, uneven floors and uncertain fire separation. A 1930s semi may have an extension that looks acceptable on a floor plan yet feels dark, cheaply built or out of character when inspected. A cottage may have mixed construction, low-level damp and irregular alterations carried out over decades. Those details affect saleability as much as headline value.

When a physical inspection becomes necessary

There comes a point where the sensible question is no longer whether a desktop valuation is faster. It is whether the instruction can be carried out responsibly without seeing the property.

A physical inspection is usually required where:

- You already know repairs are needed, or the property has been vacant, poorly maintained or partly refurbished.

- The photos are limited, old or selective, which often means the weaker parts of the property are not being shown.

- The documents do not line up, for example where the floor plan, title, EPC, planning history and sales particulars suggest different layouts or sizes.

- The property is unusual for its location, making comparable evidence thin or unreliable.

- The valuation will support a major decision, such as a purchase, dispute, settlement, secured lending case, or any situation where the figure may be challenged later.

If two or three of those points apply, a desktop-only figure becomes much harder to defend.

The practical risk for a buyer or remortgager is simple. A desktop valuation can be perfectly reasonable for a standard, well-documented property. It becomes less dependable once construction, condition, layout or legal history stray from the ordinary. At that stage, an inspection is not a luxury. It is a requirement if you want a figure grounded in the property itself rather than in assumptions about it.

Cost, Timescales and How to Order Your Valuation

You are remortgaging a fairly ordinary semi-detached house and need a figure quickly. The obvious question is not just "How much will it cost?" It is "Will a desktop valuation be accepted for this property and this purpose, or will I end up paying twice after being told an inspection is needed anyway?"

That distinction matters because desktop valuations are usually cheaper and faster than inspection-based work, but there is no single market price or fixed turnaround that applies in every case. Fees and timescales depend on the purpose of the valuation, the amount of reliable evidence available, and whether the surveyor can give an opinion responsibly without seeing the property.

As noted earlier, UK readers usually want three practical answers. What it costs, how long it takes, and whether the result will be accepted by the lender or other party relying on it. The difficulty is that acceptance depends less on speed and more on suitability. A standard flat with clear recent comparables is one thing. A converted property, a heavily extended house, or a home with signs of poor condition can quickly move into inspection territory.

A simple decision checklist

Before you order anything, check five points:

- Is the property fairly standard for the area? Typical estate houses, modern flats and conventional terraces are easier to assess remotely than unusual homes or mixed-use buildings.

- Is the condition likely to be average? If there may be damp, structural movement, poor maintenance, or very high-spec refurbishment, the value can shift more than desktop assumptions allow.

- Is the paper trail clear? Floor plans, title details, EPC data, planning records and past sales should broadly line up.

- What is the valuation being used for? Routine lending or internal decision-making may suit desktop. A purchase where you are relying heavily on the figure, or any case where the figure may be challenged later, often needs more.

- Will the end user accept it? If a lender, solicitor, court, or tax adviser requires inspection-based evidence, the decision has already been made.

A desktop valuation works a bit like pricing a car from its registration, mileage history and old photographs. It can be sensible for a standard example. It becomes less reliable if the engine has problems, the bodywork has been altered, or the records are patchy.

How to order one sensibly

Start with the reason for the valuation. Tell the surveyor whether this is for remortgage, probate, matrimonial proceedings, tax, shared ownership, or an internal check on likely value. Purpose affects both the scope and the level of caution needed.

Next, describe the property plainly and completely. Mention extensions, loft conversions, non-standard construction, short lease issues, Japanese knotweed history, known defects, flood history, or recent major works. Many delays happen because the property is presented as ordinary at the start, then turns out to have features that make a desktop opinion hard to support.

Then ask three direct questions. Is a desktop valuation suitable for this exact property? What assumptions will the surveyor have to make? Under what circumstances would they stop and recommend a physical inspection instead?

Clear answers are a good sign. Vague answers usually mean the instruction needs a closer look.

If speed is the priority, ask for the likely turnaround before ordering, but treat that as a guide rather than a promise. Delays often come from missing documents, inconsistent property records, or the surveyor spotting an issue that cannot be resolved from a desk. In practice, the quickest valuation is the one ordered on the right basis first time.