Valuation

Jul 16, 2026

What Is a RICS Valuation? Your 2026 Guide

Unsure what is a RICS valuation? Our 2026 guide covers the Red Book standard, costs, process, & why it's vital for UK property.

A RICS valuation is a legally sound, impartial assessment of a property’s true market value, carried out by a qualified surveyor to strict Red Book standards. In the UK, pricing commonly starts from £349 including VAT for smaller properties, which is why it’s often the practical choice when you need a figure that can stand up to lender, legal, or tax scrutiny.

If you're buying a home, dealing with probate, redeeming a Help to Buy loan, or trying to settle on a realistic asking price, the number attached to the property stops being a casual estimate very quickly. It becomes the figure other people rely on. Your lender relies on it. Your solicitor may rely on it. In some situations, a court or government scheme may rely on it too.

That’s where many owners and buyers get caught out. They assume a bank’s mortgage valuation tells them what the property is worth, or they treat an estate agent’s appraisal as if it carries the same weight as a formal valuation. It doesn’t. Those misunderstandings can be expensive.

The question 'what is a rics valuation' often arises when a property decision suddenly becomes real. You’ve had an offer accepted, a family member has died, a remortgage deadline is approaching, or you need a value for a legal process and nobody wants a guess.

In those moments, “roughly what it’s worth” isn’t enough. You need a figure that is evidence-based, independent, and defensible if someone challenges it. That’s the gap a RICS valuation fills.

A proper valuation matters because property value isn’t just about floor area and postcode. A surveyor looks at the construction, condition, visible defects, local demand, recent comparable sales, and the market conditions on the valuation date. A tired flat on a good street may not perform like the better-presented one next door. A house with dampness or structural movement may not support the figure an owner has in mind.

Practical rule: when the valuation will affect borrowing, tax, a legal settlement, or a binding financial decision, use a formal valuation rather than an informal opinion.

The other reason this matters is independence. A RICS valuer is there to provide an impartial opinion of market value, not to secure an instruction to sell the property and not to push a lending decision through.

That distinction sounds technical. In practice, it’s the difference between a useful professional document and a number that only works until somebody asks how it was reached.

A RICS valuation is a professional assessment of a property’s market value carried out by a RICS-registered chartered surveyor under the RICS Red Book Global Standards. That matters because the Red Book is the rulebook that sets out how valuations must be instructed, inspected, evidenced, and reported, creating consistency and transparency across the process, as outlined by Crest Surveyors’ explanation of the RICS valuation standard and pricing.

First, there’s the professional. The valuer does not provide only a personal opinion. They’re acting in a regulated capacity and must be properly qualified and registered to undertake this work.

Second, there’s the standard. The Red Book requires a structured approach. The report must clearly state what is being valued, the basis of value being used, the assumptions made, and the evidence considered.

Third, there’s the purpose. A RICS valuation gives an impartial opinion of market value at a specific date. That date matters because value is always tied to market conditions at that moment, not to what the property might achieve in a stronger market six months later.

A simple way to think about it is this. A Red Book valuation is closer to a formal financial audit than to a quick estimate. It is meant to be checked, relied on, and defended if needed.

The valuation itself is grounded in evidence. A surveyor will typically inspect the property’s size, layout, condition, build quality, and obvious defects that may affect value. They’ll also analyse comparable sales of similar properties, commonly looking at type, size, condition, and proximity, and using recent market evidence.

Key factors often include:

A valuation is not a prediction of the best possible sale result. It is a supported opinion of current market value on the inspection date.

That’s why clients use it for secured lending, probate, matrimonial matters, financial reporting, and Help to Buy. It is designed to stand apart from optimism, pressure, and sales tactics.

This is the misunderstanding that causes the most trouble. A mortgage valuation and a RICS Red Book valuation are not the same service, even when both involve a figure for value.

A lender’s mortgage valuation exists to protect the lender. Its job is to help the bank decide whether the property is suitable security for the loan. Your interests are secondary. In some cases, the inspection may be limited, and the detail you receive can be minimal.

A Red Book valuation is different. It is a formal, independent valuation prepared to professional standards for the purpose stated in the instruction. If you are the client, the report is prepared for your decision-making, not just the lender’s risk control.

| Feature | RICS Red Book Valuation | Mortgage Valuation |

|---|---|---|

| Primary purpose | To provide an impartial, evidence-based opinion of market value | To help the lender assess loan security |

| Who it is for | The instructing client and any stated relying parties | The mortgage lender |

| Standard used | RICS Red Book standards | Lender-specific requirements |

| Inspection scope | Structured inspection with evidence gathering for valuation purposes | Often more limited and lender-focused |

| Report detail | Formal report explaining basis, assumptions, and valuation evidence | Usually brief, sometimes with limited commentary |

| Use in disputes or legal matters | Suitable where a defensible valuation is needed | Usually not an adequate substitute |

| Independence | Impartial opinion under professional standards | Still professional, but commissioned for lender protection |

If you are buying, the bank’s valuation does not tell you whether you are paying a sensible price in any broader sense. It tells the lender whether the property appears adequate security for the mortgage amount.

That distinction is particularly important if the property has defects, unusual features, short lease issues, or a local market that moves unevenly. In those cases, buyers often assume, “The lender valued it, so it must be fine.” That’s a poor working assumption.

UK evidence from the MSCI UK Annual Property Index, analysed by RICS, found that 82% of properties sold within plus or minus 20% of their prior RICS valuation and 60.4% sold within plus or minus 10%, which is why the Red Book framework is relied on for high-stakes decisions, as shown in the RICS analysis of valuation and sale price alignment.

Sometimes a mortgage valuation is enough. If your only concern is that the lender is prepared to lend and you are comfortable with the broader risks, you may leave it there.

In many cases, that isn’t enough.

You should think carefully about a proper valuation when:

If you want a fuller explanation of the bank-side process, Survey Merchant has a useful guide on what a mortgage valuation is.

A RICS valuation becomes important when the number has consequences. The most common mistake I see is people waiting until the deadline is close and then discovering the figure has to satisfy a lender, solicitor, scheme administrator, or court.

A buyer may want an independent value before committing to a purchase price. A seller may need a formal valuation when family members disagree on price expectations. In both situations, the value needs to be rooted in evidence rather than enthusiasm.

This is also where a formal valuation can calm a transaction. It gives everyone one document to discuss instead of three competing opinions from online tools and local agents.

Probate is a common trigger. Executors often need a defensible value for the estate, and it helps if the valuation is prepared by a regulated professional using a recognised standard.

Matrimonial matters are another. When a property forms part of a financial settlement, both sides need a figure that is independent and capable of withstanding scrutiny. As noted by Aston Knowles on RICS valuation uses in lending and legal settings, RICS Red Book valuations for Help to Buy cost around £250 and are accepted by 95% of UK lenders, while RICS evidence in matrimonial cases carries substantial legal weight.

In contentious situations, the most useful valuation is rarely the highest one. It is the one that is easiest to defend.

Help to Buy redemptions regularly catch owners off guard. The scheme doesn’t work off an estate agent’s marketing figure. It requires a compliant RICS valuation.

Shared ownership staircasing can create similar pressure. If the valuation isn’t prepared correctly, the process can stall while the deadline keeps moving.

Later in the process, this short explainer is worth watching because it helps people understand why formal valuations are used in scheme and lending contexts:

Remortgages can also call for a formal valuation, especially where the property has changed, the title is unusual, or the lender needs stronger support for the figure. Survey Merchant also has a practical article on home valuation for remortgage decisions.

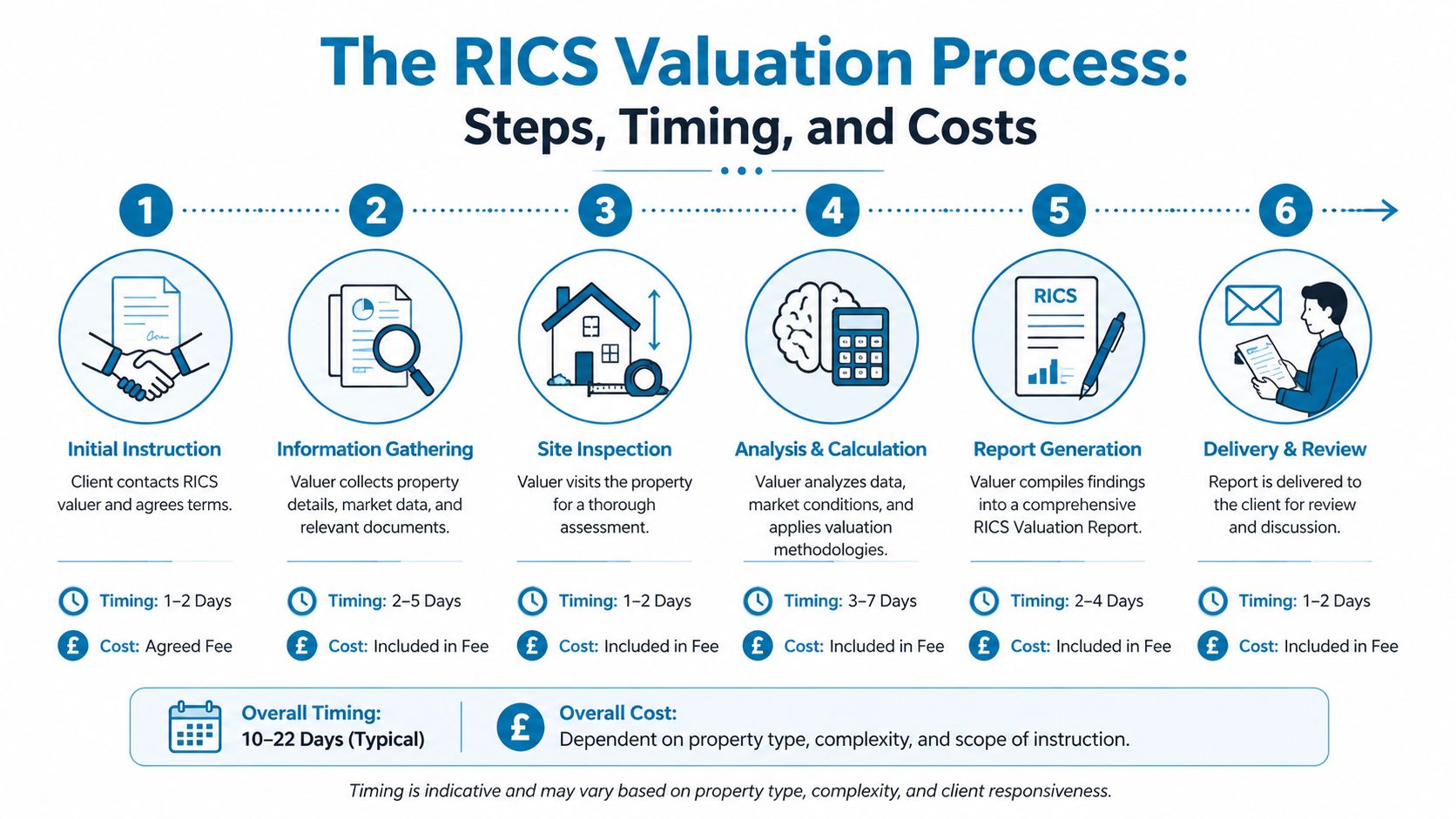

Clients often assume valuation is a black box. It isn’t. The process is structured, and once you know what the surveyor is doing, the report makes more sense.

The technical framework sits within VPS 1-5, which governs the terms of engagement, inspection, investigations, reporting, basis of value, and valuation approaches. That discipline is one reason UK commercial valuations have been shown to average within 5-10% of subsequent sale prices, according to the RICS Red Book Global Standards and related valuation framework.

The sequence is usually straightforward:

A valuer is not just walking around deciding whether they “like” the house. They’re checking value drivers and value detractors.

That typically includes:

Working rule: tidy presentation can help inspection clarity, but it won't hide defects and it won't turn weak comparable evidence into a stronger valuation.

For residential work, pricing commonly starts from £349 including VAT for up to 2-bed properties, rising to £369 for 3-bed, £399 for 4-bed, and £449 for 5-bed properties, with size, location, and complexity all influencing cost, as set out in the earlier linked Crest Surveyors guidance.

Costs vary because some instructions are simple and others are not. A standard flat in an active market is usually easier to evidence than a large altered house, a mixed-use property, or a building with unusual title or construction features.

If you need help finding a local valuer, Survey Merchant’s London home valuation guide gives a useful sense of what to ask and how local market knowledge affects the instruction.

A valuation tells you what the property is worth. A survey tells you what is wrong with it. Clients mix these up all the time.

That confusion matters because one service cannot fully replace the other. A valuation may note visible matters affecting value, but it is not the same thing as a condition-led inspection such as a RICS Level 2 or Level 3 survey.

A valuation focuses on market value at a particular date. It considers condition only to the extent that condition affects market worth.

A survey focuses on the building itself. It examines defects, maintenance issues, repair priorities, and the practical implications of what the surveyor sees.

That means a survey is generally the right choice if your concern is hidden cost, repair liability, or the general health of the building. A valuation is the right choice if your concern is establishing a formal figure for lending, legal, tax, or negotiation purposes.

Choose a valuation if you need:

Choose a survey if you need:

You may need both if you are buying an older, altered, or visibly tired property. In that situation, knowing the market value without understanding the defect profile can leave a buyer with an incomplete picture.

The valuation may tell you the asking price is defensible. The survey may tell you the building still isn’t a sensible buy at that figure.

That depends on the purpose, but for Help to Buy equity loan redemptions the report is only valid for three months, as explained in Nuven Surveyors’ guide to RICS valuations and Help to Buy requirements. That matters because if the deadline slips, you may need an updated valuation or a new instruction.

The timing issue is not minor. With over 410,000 active Help to Buy equity loans in Great Britain as of March 2024, a lot of owners are dealing with the same expiry problem, particularly when solicitors, lenders, and administrators are all working to different timescales in that same Nuven guidance.

No. An estate agent’s appraisal is usually a marketing opinion. It may be useful for deciding how to launch a sale, but it is not the same as a regulated Red Book valuation prepared by a RICS valuer.

The practical difference is independence and purpose. A formal valuation is produced to assess market value. A sales appraisal is produced in a selling environment.

Start by reading the report carefully. Most disputes come from one of three issues: the client expected a different number, key property information was missing at the time of inspection, or the comparable evidence used doesn’t reflect something material about the property.

If you believe there is a genuine issue, respond with evidence rather than objection. Helpful material may include:

A valuer may review additional evidence, but that doesn’t mean the figure will change. A challenge works best when it addresses facts and comparables, not disappointment.

Defects and expiry. If visible issues are underestimated or not properly factored in, owners can end up with a value that doesn’t align with market reality or with scheme expectations. If the report expires before the redemption process completes, the valuation may no longer be acceptable.

Using a platform that matches clients with surveyors who have suitable local experience can reduce that risk because local evidence and scheme familiarity both matter in practice.

Check that the valuer is appropriately qualified, registered with RICS for valuation work, and experienced in the type of property and purpose involved. A probate flat, a matrimonial house valuation, and a Help to Buy redemption are all formal valuations, but the practical requirements around them can differ.

Ask direct questions. Has the surveyor dealt with this type of instruction before? Will the report be Red Book compliant? Are there any scheme-specific requirements? Good instructions usually start with that basic discipline.

If you need a formal valuation and want help finding the right surveyor for the job, Survey Merchant connects property owners, buyers, and professionals with a nationwide panel of qualified surveyors for RICS valuations, surveys, and related property instructions.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes