Valuation

Jul 16, 2026

How to get a property valuation: a complete guide

Learn how to get a property valuation with our complete guide. Discover the best methods to ensure accurate, reliable property evaluations.

A property valuation is a professional opinion of a property’s market value, based on physical inspection, comparable sales, and defined reporting standards. Whether you are buying, selling, or refinancing, knowing how to get a property valuation correctly determines whether the figure you receive is legally defensible or simply a rough estimate. The difference matters enormously. A formal valuation from a RICS Chartered Surveyor carries weight with lenders, solicitors, and courts. An online estimate from Zoopla or Rightmove does not. This guide covers every stage of the process, from choosing the right valuation type to reading your final report.

Not all valuations are equal. The type you need depends entirely on your purpose, and choosing the wrong one wastes both time and money.

Automated Valuation Models (AVMs) are free online tools offered by platforms such as Zoopla and Rightmove. They generate instant estimates using public records and recent sales data. Free online tools provide a useful starting point but are not accepted for formal decisions. Use them for initial research only.

Estate agent appraisals are free market assessments carried out by local agents. They reflect current buyer demand and are useful when pricing a property for sale. However, legally binding valuations in the UK require a RICS Chartered Surveyor. Estate agent figures carry no formal weight with lenders or courts.

RICS Red Book valuations are the gold standard for formal purposes. These follow strict RICS VPS 1–6 standards and specify the basis of value, purpose, and inspection scope. They are required for mortgage applications, probate, tax, matrimonial disputes, and commercial transactions.

Desktop valuations are conducted without a physical site visit, using available data and photographs. They are faster and cheaper but carry more assumptions. Lenders rarely accept them for high-value or complex properties.

| Valuation type | Typical cost | Accuracy | Best use case |

|---|---|---|---|

| AVM (Zoopla, Rightmove) | Free | Low | Initial research |

| Estate agent appraisal | Free | Moderate | Sale pricing guidance |

| Desktop valuation | £150–£300 | Moderate | Low-risk remortgage |

| RICS Red Book valuation | £300–£1,500+ | High | Mortgage, legal, tax |

Pro Tip: If you are remortgaging, ask your lender whether they accept a desktop valuation before commissioning a full RICS report. Many lenders accept desktop assessments for straightforward residential cases, which can save you both time and fees.

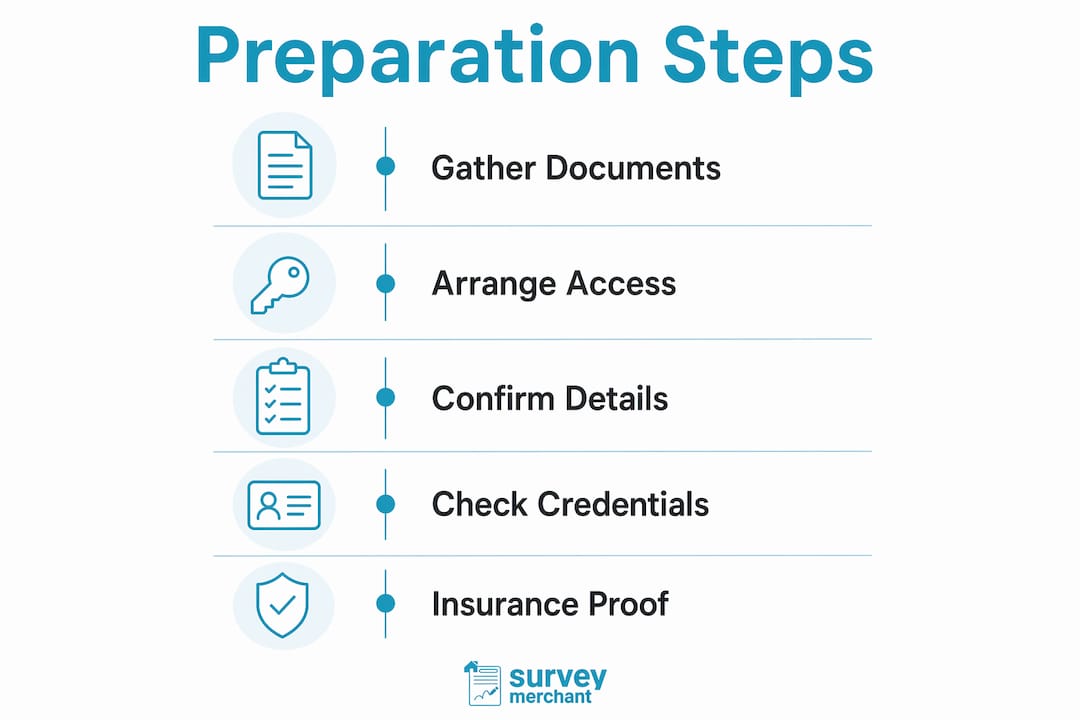

Preparation directly affects the quality and usability of your valuation report. Valuers cannot produce a defensible figure without accurate, complete information.

Defining the valuation purpose and the required valuation date upfront is the single most critical step. Purpose determines the basis of value, the level of investigation, and the report format. A valuation for a mortgage differs structurally from one for probate or a tax tribunal. Getting this wrong means the report may be rejected by the intended user.

Gather the following before instructing a valuer:

Providing access details and tenancy information upfront prevents delays and reduces the risk of the valuer making assumptions that could undermine the report’s accuracy.

For formal valuations, you must instruct a RICS Chartered Surveyor or a registered valuer. In the UK, the RICS register is publicly searchable. Always verify valuer qualifications before signing an instruction letter.

Pro Tip: Request a copy of the valuer’s professional indemnity insurance certificate before instructing them. If the report contains an error that costs you money, you need to know they are covered.

Understanding each stage prevents surprises and helps you manage timelines effectively.

For a purchase, instruct a valuer after your offer is accepted. For a remortgage, instruct after submitting your application. Your lender may appoint their own valuer, in which case you pay the fee but do not choose the professional. For independent valuations, you select and instruct directly.

The valuer visits the property and conducts a physical inspection. Appraisers visit properties for around 30 minutes for modest homes, though larger or more complex properties take longer. The inspection covers condition, layout, construction quality, and any visible defects.

After the inspection, the valuer analyses recent comparable sales, known as comps. Market value is based on what a willing, informed buyer would pay, using comparable sales typically from the past 3–6 months. Valuers commonly use 3–5 comps, adjusting for differences in size, condition, and location.

Report writing takes longer than the visit itself. Mortgage appraisal timelines range from 10 to 16 days from instruction to report delivery. Plan your transaction timeline around the full process, not just the appointment date.

Once you receive the report, check every factual detail. Buyers should verify property details and flag any inaccuracies to the lender promptly. Errors in floor area, bedroom count, or tenure type can affect the valuation figure and delay your transaction.

| Stage | Typical duration |

|---|---|

| Instruction to appointment | 3–7 days |

| On-site inspection | 30 minutes to 3 hours |

| Report drafting and review | 7–10 days |

| Total process | 10–16 days |

Pro Tip: Ask the valuer to confirm receipt of your instruction in writing and to notify you immediately if they identify any access issues or missing information. Early communication prevents last-minute delays.

Most valuation problems are avoidable. They stem from unclear instructions, wrong professional choices, or misplaced trust in informal estimates.

A valuation report is a professional opinion supported by investigation and analysis for a defined purpose and date. It produces defensible figures for intended users such as lenders or solicitors. This is what separates a formal report from a marketing estimate.

Pro Tip: If you are selling and want to sense-check an agent’s asking price, commission an independent RICS valuation. The fee is modest relative to the risk of mispricing a property by tens of thousands of pounds.

A valuation report contains more information than a single number. Understanding its components helps you use it correctly.

The report will state the basis of value (usually market value for residential transactions), the valuation date, the scope of inspection, and any assumptions or special assumptions the valuer has made. Read these sections carefully. An assumption that the property is free of structural defects, for example, means the figure changes if defects are later discovered. For a deeper understanding of formal standards, the RICS Red Book framework explains how these components interact.

A valuation report is a professional opinion, not a guarantee of sale price. The figure reflects conditions on the valuation date. Markets move, and a valuation from six months ago may no longer reflect current conditions.

Use the report to inform your negotiation position, satisfy your lender’s security requirements, or support a legal or tax submission. If the figure surprises you, seek clarification from the valuer in writing before acting. A second opinion from another RICS Chartered Surveyor is always an option for high-value or disputed cases. For guidance on selecting the right professional, the Surveymerchant blog on navigating valuations covers the key questions to ask before instructing.

Valuations and home surveys are different products. A valuation tells you what a property is worth. A building survey tells you what condition it is in. For major purchases, you need both.

Pro Tip: If your lender’s valuation comes in below the agreed purchase price, do not panic. Request the full report, check the comparables used, and ask your solicitor whether a formal challenge or a renegotiation with the seller is the better route.

A reliable property valuation requires the right professional, a clearly defined purpose, and a thorough review of the final report before making any financial decision.

| Point | Details |

|---|---|

| Choose the right valuation type | Match the valuation method to your purpose: RICS Red Book for legal or lending use, AVM for initial research only. |

| Define purpose and date upfront | Unclear instructions produce reports that lenders and courts may reject, costing time and money. |

| Verify valuer credentials | Only RICS Chartered Surveyors produce valuations accepted by UK lenders, HMRC, and courts. |

| Allow 10–16 days for the full process | The on-site visit is brief; report drafting and lender review account for most of the total timeline. |

| Review the report carefully | Check all factual details and flag errors promptly to avoid delays or incorrect figures affecting your transaction. |

Most people treat a property valuation as a formality. They order one because the lender requires it, skim the figure, and move on. That approach costs people money.

The detail that matters most is buried in the assumptions section. I have seen transactions unravel because a buyer accepted a valuation that assumed vacant possession, when the property was actually tenanted. The valuer was not wrong. The buyer simply did not read the report.

The other mistake I see repeatedly is conflating a free estate agent appraisal with a professional valuation. Agents are skilled at reading buyer demand. They are not producing defensible figures under RICS standards. Using an agent’s number to justify a major financial decision is like using a weather app to plan a structural drainage project.

My advice is straightforward. Treat the valuation report as a legal document, because in many contexts it is one. Read every section, not just the headline figure. If something does not make sense, ask the valuer directly. A good professional will explain their reasoning clearly. If they cannot, that tells you something important about the quality of the report.

Property decisions involve large sums and long commitments. A valuation is one of the few points in the process where you get an independent, qualified opinion. Use it properly.

— Surveymerchant

Getting a formal property valuation does not need to be complicated. Surveymerchant connects you with RICS Chartered Surveyors across the UK who deliver accurate, purpose-specific valuation reports for mortgage, legal, probate, and investment use.

Every valuer in the Surveymerchant panel holds verified RICS credentials and professional indemnity cover. Reports are tailored to your stated purpose, whether that is satisfying a lender, supporting a tax submission, or informing a purchase negotiation. Booking is straightforward, with transparent fees confirmed before instruction. If you are ready to commission a formal valuation, visit Surveymerchant’s RICS valuation services to get started. For commercial properties, the commercial surveying services page covers specialist options.

A valuation gives an opinion of a property’s market value on a specific date. A survey assesses the physical condition of the building. For most purchases, you need both.

The on-site inspection typically takes 30 minutes to 3 hours depending on property size. The full process from instruction to report delivery takes 10–16 days.

Yes. UK mortgage lenders require a formal valuation from a qualified professional. For legally binding purposes, a RICS Chartered Surveyor is the required standard.

Yes. Request the full report, review the comparables used, and raise any factual errors with your lender in writing. You can also commission an independent RICS valuation as a second opinion.

Costs vary by property type and purpose. RICS Red Book valuations typically range from £300 to over £1,500 for complex or high-value properties. Estate agent appraisals are free but carry no formal weight.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes