You usually discover you need a Red Book valuation at the point when an informal opinion stops being useful. A lender asks for a formal report. A solicitor needs a defensible figure for probate. A court timetable is running. A tax submission has to stand up if questioned later. In those moments, an estate agent's appraisal or a quick online estimate won't do the job.

That's where rics red book valuations matter. They exist for situations where the figure has to be more than plausible. It has to be reasoned, documented, impartial and capable of being defended if someone challenges it. That's why these valuations carry weight with lenders, courts, accountants and tax advisers. They aren't designed to reassure. They're designed to withstand scrutiny.

If you're unsure whether you need one, the starting point is understanding what RICS qualified means. The letters matter because the standard matters, and the standard matters because your financial position may depend on it.

Table of Contents

- Understanding the Gold Standard of Property Valuation

- Why the framework matters

- How the principles protect you

- Can I use a Red Book valuation for a mortgage application

- How long is the valuation valid

- What if I disagree with the valuation figure

Understanding the Gold Standard of Property Valuation

A Red Book valuation is a formal valuation carried out under the RICS Valuation standards. In UK practice, that makes it markedly different from a market appraisal, an asking price suggestion, or an agent's view of what a property might sell for. Those other opinions may be useful in the right context. They are not built for regulated, legal or contentious situations.

The reason clients call it the gold standard is simple. It is meant to produce a figure that another professional can follow, understand and test. The valuation has to be supported by proper inspection, analysis, assumptions and reporting discipline. If someone later asks, “Why this figure?”, the valuer should be able to show the route taken to get there.

That matters because property value is rarely just about today's sentiment. It can affect tax liabilities, settlement negotiations, lending decisions, financial statements and estate administration. In those settings, a weak valuation doesn't merely create inconvenience. It can expose you to challenge, delay and unnecessary cost.

Practical rule: If the valuation may be reviewed by a lender, court, HMRC, accountant or another surveyor, treat formality as protection, not bureaucracy.

A proper Red Book instruction is therefore less about getting “a number” and more about getting a number that stands up when pressure is applied. That is why clients who first ask for “just a valuation” often need a more careful conversation. The right question isn't only what the property is worth. It's whether the purpose requires a valuation that can be defended.

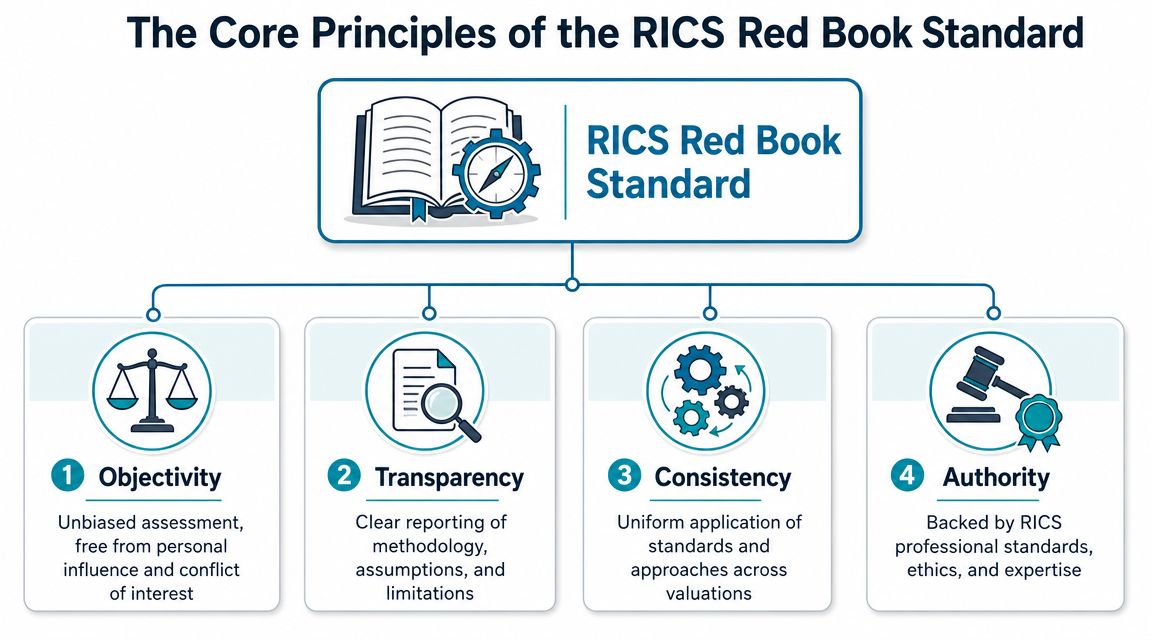

The Core Principles of the Red Book Standard

A disputed valuation rarely fails because nobody could produce a number. It fails because the number cannot be explained, tested or defended once a lender, court, accountant or tax authority starts asking proper questions. rics red book valuations are designed to reduce that risk.

RICS frames valuation practice around consistency, accuracy, objectivity and transparency. Those are not abstract professional ideals. They are the controls that stop a valuation from becoming a convenient opinion shaped by pressure, incomplete information or poor reporting.

Why the framework matters

The Red Book does not tell a valuer to apply the same formula to every flat, shop or industrial unit. Property is too varied for that. Title restrictions, tenancy terms, planning position, repair liabilities, access, contamination risk and local demand can all change value materially, even where two assets look similar from the outside.

What the standard does is control the process. The valuer must confirm the instruction properly, state the purpose, identify the basis of value, inspect and analyse relevant evidence, declare assumptions, and choose a methodology that fits the asset and the brief. That discipline protects the client's position because it limits avoidable errors and makes the reasoning visible.

That last point matters in practice. If a valuation is later challenged, the argument usually centres on evidence, assumptions or methodology. A Red Book report gives each of those issues a paper trail.

How the principles protect you

Objectivity protects you from outcome-driven advice. In probate, divorce, shareholder disputes or secured lending, interested parties often have a preferred figure before the valuer is even instructed. Independence helps keep the report usable when another expert, solicitor or judge examines it.

Transparency protects you from hidden weakness. If part of the property could not be inspected, if tenancy documents were missing, or if the valuation assumes vacant possession, that should be set out plainly. Clients are then able to judge the reliability of the figure and decide whether more information is needed before relying on it.

Consistency protects you where decisions need to stand together. That could mean a portfolio, year-end accounts, a phased tax matter or a dispute involving more than one property. Without a consistent approach to evidence and reporting, comparisons become harder to defend and inconsistencies invite challenge.

Authority comes from the valuer's qualification, regulation and accountability. A Red Book valuation is not stronger only because the surveyor is experienced. It is stronger because the surveyor is working within a professional framework that can be checked against published standards, conduct rules and audit requirements.

A sound valuation is one that can survive scrutiny, not one that avoids it.

The standards also evolve with practice. The 2025 updates tightened requirements around data handling, technology and ESG reporting. That matters for clients because valuation risk changes with the market. A standard that is kept current gives you a report that is better aligned with present-day lending, reporting and dispute conditions, rather than one built on outdated habits.

When Is a Red Book Valuation Necessary

A formal valuation becomes necessary when the value has consequences beyond negotiation. If the number will be used to satisfy a legal duty, support a tax position or evidence fairness between parties, informality usually creates avoidable risk.

Situations where informality creates risk

Probate is a common example. Families often begin with an estate agent's estimate because it's quick and familiar. That can be enough for an early conversation. It may not be enough once the estate value has to be reported properly and defended if queried.

Matrimonial proceedings are another clear case. If a property figure feeds into a financial settlement, neutrality matters as much as technical competence. The same is true for tax matters, company accounts, portfolio reporting, shared ownership staircasing, Help to Buy redemption and disputes involving co-owners.

In all of those settings, the valuation isn't just helping someone decide what to do. It may be used to justify what they already did. That's a far higher threshold.

A formal report is also often needed where one party must rely on a figure prepared by someone independent from the transaction itself. That is one reason a Red Book valuation carries weight in contentious and regulated contexts.

Why authorities and courts rely on it

A Red Book valuation must be carried out by a certified and qualified surveyor holding the RICS Registered Valuer title, which is why such reports are relied on in transactions and litigation where impartiality is essential, according to Eddisons' explanation of Red Book valuation requirements.

That qualification requirement protects the client in two ways. First, it reduces the chance that an unqualified person produces a report that looks formal but lacks standing. Second, it makes the valuer personally accountable to a recognised professional framework.

In practice, many valuation problems start before the inspection. They start when the wrong type of report is commissioned for the wrong purpose.

This short explainer gives a useful overview of where formal valuations sit in practice:

If you're in doubt, ask a blunt question at the outset: “Who needs to rely on this figure, and what happens if they challenge it?” The answer usually tells you whether a Red Book instruction is optional or necessary.

Red Book Valuations vs Other Property Reports

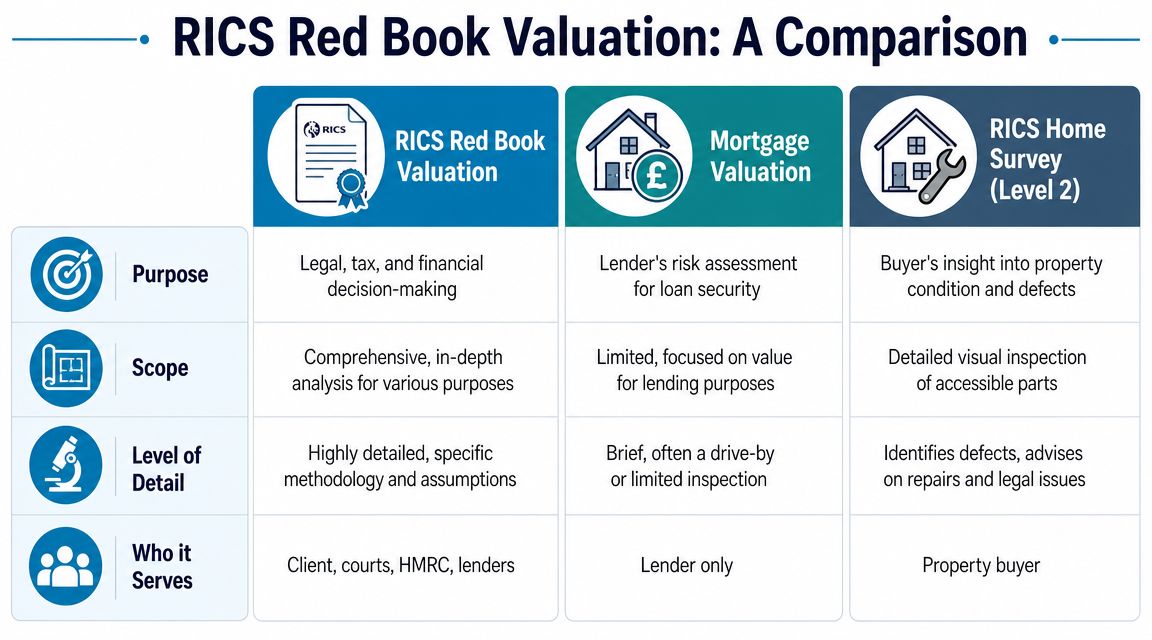

Clients regularly use the word “valuation” to mean three different things. That's how people end up ordering the wrong service. A Red Book valuation, a mortgage valuation and a building survey each answer a different question.

A valuation answers a different question

A Red Book valuation asks: what is the property worth for the stated purpose, on the stated basis, at the stated date?

A mortgage valuation asks something narrower: is this asset suitable security for the lender, and does the proposed loan sit sensibly against that security? If you want a clear primer, this explains what is a mortgage valuation.

A RICS Building Survey asks a different question again: what condition is the property in, what defects are visible, and what risks or repairs should the client understand before committing further money?

That distinction matters because many people expect one report to do all three jobs. It won't.

RICS has made the boundary clear in its guidance framing. A Red Book valuation gives procedural guidance for valuers, but it doesn't prescribe reporting formats for every scenario or replace the need for specialist inspection work. Many consumers assume a Red Book valuation will reveal defects or repair costs, when those issues require a Building Survey, as discussed in this RICS video on valuation scope and limits.

Valuation vs Survey What's the Difference

| Feature | RICS Red Book Valuation | Mortgage Valuation | RICS Building Survey (Level 3) |

|---|---|---|---|

| Purpose | Formal opinion of value for legal, tax, financial or dispute use | Lender's lending risk assessment | Detailed advice on condition, defects and repair issues |

| Scope | Inspection plus valuation analysis and formal reporting | Limited review focused on lending security | Detailed visual inspection of accessible parts |

| Level of detail | Focused on basis of value, assumptions, evidence and reasoning | Usually brief and narrow | Focused on fabric, defects, maintenance and risk |

| Who it serves | Client and any legitimate relying party identified in the terms | Primarily the lender | The buyer or owner commissioning the survey |

A buyer who orders only a valuation may still miss serious building problems. A buyer who orders only a survey may still lack the formal valuation needed for a legal or tax purpose. The right instruction depends on the decision you're trying to support.

“What am I trying to prove, and to whom?” is usually the most useful starting question.

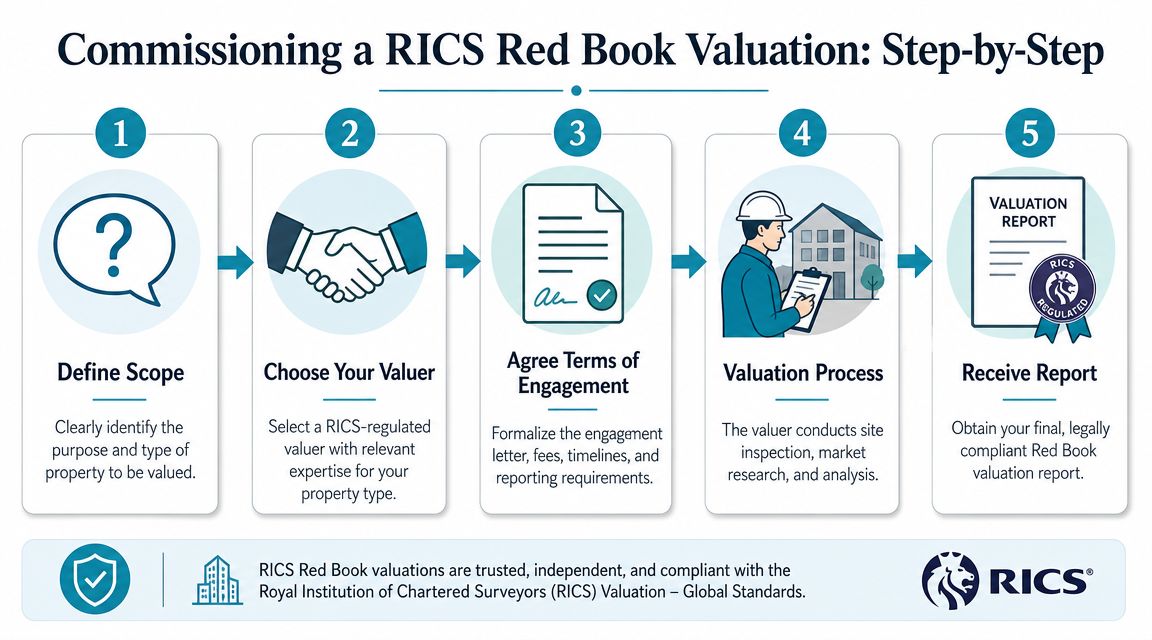

How to Commission a Red Book Valuation

A weak instruction often starts with a simple but expensive mistake. A client asks for “a valuation” without stating whether it is needed for probate, tax, accounts, a dispute, secured lending, or internal decision-making. That omission affects the basis of value, the assumptions the valuer can make, the wording of the report, and whether the final opinion will stand up if someone later challenges it.

Start with the purpose

State the purpose in exact terms. “For legal purposes” is too loose to be useful. “For probate”, “for matrimonial proceedings”, or “for year-end accounts” gives the valuer a defined brief and helps avoid a report that is correct in form but wrong for your actual use.

This is not paperwork for its own sake. The Red Book requires the valuer to be clear about purpose because purpose determines the basis of value, the assumptions that are permitted, and the level of investigation needed. If those points are wrong at instruction stage, the report can be exposed later by HMRC, auditors, solicitors, a lender, or the other side in a dispute.

The next check is competence. A valuer may be experienced and still be the wrong choice for the asset in question. A city-centre flat, a care home, a development site, and a mixed-use parade call for different market knowledge, different evidence, and often different judgement on risk. Choosing the right specialist protects you from a valuation that looks professional on the page but is difficult to defend under scrutiny.

You should then receive formal terms of engagement. Read them carefully.

They should identify the client, the property, the purpose, the basis of value, any assumptions or special assumptions, the extent of inspection, the fee basis, the timescale, and who may rely on the report. Those points matter because they define the valuer's duty and the boundaries of the advice. If a later argument arises, the terms of engagement are often the first document reviewed.

What a properly commissioned instruction looks like

A sound instruction usually follows this order:

- Define the brief clearly. Provide the exact purpose, full property address, tenure details if known, and any fixed deadline linked to court, tax, audit, or transaction requirements.

- Check the valuer's credentials and fit. Confirm the surveyor is a RICS Registered Valuer and has relevant experience in that property type and locality.

- Agree the terms before work starts. Pay close attention to scope, assumptions, limitations, reliance, conflicts, and the reporting format.

- Supply the right documents early. Depending on the asset, this may include title documents, leases, tenancy schedules, plans, service charge information, planning papers, or accounts.

- Arrange access and respond promptly. Delays often arise from practical issues such as absent occupiers, missing keys, or incomplete information rather than the valuation itself.

Each step reduces a different risk. A clear brief reduces the chance of an unusable report. A qualified valuer reduces the risk of poor judgement. Proper terms reduce ambiguity over what was, and was not, commissioned. Good document supply improves the quality of the analysis. Reliable access keeps the inspection from becoming a partial exercise built on assumptions that could have been avoided.

Some clients use a matching service to find an appropriate professional. Survey Merchant is one example of a UK platform that connects clients with surveyors for valuations and related instructions. That can help where the property is unusual or the client is not yet sure which surveying discipline is needed.

A well-run instruction feels orderly because it is. The valuer inspects, checks the legal and occupational context where relevant, analyses market evidence, and reports within the agreed scope. That discipline is what gives a Red Book valuation its weight. If the figure is ever questioned, the strength of the instruction is part of what protects your position.

What to Expect in Your Valuation Report

A dispute usually starts with a simple question. Why is this figure the right one? A Red Book valuation report should answer that question in a way a lender, solicitor, tribunal, accountant, or HMRC can follow and test.

The report is not just a number on headed paper. It is the written record of how the valuer reached that opinion, what evidence was used, what assumptions were made, and where the limits of the instruction sit. If those points are unclear, the valuation is harder to rely on when money, liability, or timing is under pressure.

The parts that really matter

Start with the report's anchors. These usually include the client name, the property address, the purpose of the valuation, the valuation date, the basis of value, and the valuer's identity and status. Those details protect you because they fix the context. A valuation for probate on a past date is a different exercise from a valuation for secured lending today. If the purpose or date is wrong, the figure may be unusable even if the property description is accurate.

Then look at the method and reasoning. A sound report explains what was inspected, the property characteristics that affect value, the market evidence analysed, and how that evidence supports the conclusion. Where assumptions or special assumptions have been used, they should be set out plainly. That matters because assumptions can shift value materially. If a report assumes vacant possession, a new lease, or full compliance with planning and repair obligations, you need to see that in black and white.

Limitations deserve careful reading.

If parts of the property were not inspected, documents were not available, or information was provided by others and relied on without full verification, the report should say so. That is not defensive drafting. It tells you where risk remains and whether further checks are needed before you act on the figure.

Independence should also be stated clearly. If the valuation may be scrutinised by a lender, tax authority, court, or opposing expert, the valuer's objectivity is part of what gives the report weight. An opinion that cannot be shown to be impartial is far easier to challenge.

What modern reports now need to address

Current reporting standards also expect valuers to deal with factors that materially affect value, even where they sit outside the points clients traditionally focus on. That can include sustainability issues, energy performance, flooding, building compliance, obsolescence, or marketability concerns linked to the asset's condition and use. The point is not to turn every report into a building survey. The point is to avoid a figure that ignores a real pricing risk in the market.

The same applies to technology. A valuer may use digital tools, databases, or modelling to support analysis, but professional judgement remains the part that protects you. If the figure is challenged, the defence lies in the reasoning, evidence, and signed opinion of a qualified surveyor, not in software output alone.

Clients sometimes confuse a valuation report with other survey products. If you are comparing service types, this guide for property buyers on RICS surveys helps clarify the difference. A valuation answers what the asset is worth on stated terms and assumptions. It does not replace advice on every defect, repair item, or legal issue unless those matters fall within the agreed scope and materially affect value.

A good Red Book report should leave very little room for ambiguity. You should be able to see what was done, why the opinion was reached, and where the risks sit if any key assumption turns out to be wrong. That clarity is what makes the valuation useful, and defensible, when the figure matters most.

Fees Timelines and Finding an Expert Valuer

Fees vary because instructions vary. A standard flat with good comparables, clear documents and easy access is not the same job as a large country house with outbuildings, title complexity or a deadline linked to litigation. The work behind the figure changes, so the price changes too.

What affects the fee

The main influences are usually:

- Property type. Houses, flats, mixed-use assets and investment properties require different levels of analysis.

- Complexity. Short leases, unusual construction, development potential or legal irregularities increase the time needed.

- Purpose of the report. A valuation intended for a dispute or formal tax matter often requires extra care in scope and wording.

- Location and access. Travel, tenant coordination and inspection practicalities all affect delivery.

- Urgency. If you need a report urgently, that should be discussed up front rather than assumed later.

Turnaround also depends on the instruction quality. Clear documents and prompt access help. Vague briefs and missing lease papers don't.

How to choose sensibly

The cheapest quote is not always the lowest-cost option if the report later needs clarification, amendment or replacement. Ask whether the valuer regularly handles your type of property and your type of purpose. Those are different questions, and both matter.

If you're comparing service types as well as valuation quotes, this guide for property buyers on RICS surveys is a useful companion. It helps clients separate valuation needs from inspection needs, which is where many early mistakes happen.

Frequently Asked Questions About Red Book Valuations

Can I use a Red Book valuation for a mortgage application

Sometimes, but you shouldn't assume it will replace the lender's own process. Many lenders want a valuation instructed through their own panel because the report is part of their lending risk control. A Red Book valuation you commission privately may still be useful for negotiation, internal decision-making or checking whether a lender's figure appears sensible, but it won't automatically substitute for the lender's requirements.

How long is the valuation valid

A valuation is tied to its valuation date, not issued as an open-ended guarantee. Markets move. Evidence changes. A figure that was well supported at one date may need review later, particularly if the property, the market conditions or the purpose have changed. If you need to rely on an older report, ask the valuer whether an update or reinspection is required rather than assuming the original figure still stands.

What if I disagree with the valuation figure

Start by reading the report carefully. Many objections come from misunderstanding the assumptions, the basis of value or the information the valuer had available. If you still disagree, raise specific points rather than general dissatisfaction. That might include comparable evidence you think has been missed, legal facts that were not considered, or physical issues that affect value.

A sensible challenge is evidence-led. “I was hoping for more” isn't a valuation argument. “This tenancy detail was omitted” or “this comparable appears materially superior” is.

If the report is for a contentious purpose, ask the valuer whether clarification, reconsideration or a formal update is appropriate. In some disputes, the answer may not be changing the report. It may be obtaining an independent second opinion on the same defined basis.

If you need a Red Book valuation and want help finding a surveyor with the right expertise for the property and purpose, Survey Merchant can connect you with suitable UK professionals for formal valuation instructions.