If you're staring at your lease term and realising the number is getting uncomfortably low, you're not alone. Most owners first look into a lease extension when they want to remortgage, sell, or stop the lease becoming a bigger problem later. Then the quotes start coming in, and the figure that caught your eye at first is usually just the premium, not the full amount you'll need in the bank.

That's where people get caught out. Extending leasehold costs rarely come as one neat bill. There is the payment to the freeholder, your own surveyor and solicitor, the freeholder's professional fees, and sometimes upfront cash demands that arrive before the final price is agreed. If you're also dealing with a sale or wider leasehold concerns, local specialist guidance such as Preston leasehold property advice can help you understand the legal setting around your property.

The most misunderstood part is often the jump in cost once the lease falls below a key threshold. If that part feels vague, Survey Merchant's marriage value article is a useful background read before you start speaking to valuers and solicitors.

Table of Contents

Why Extending Your Lease Can Feel So Expensive

A flat owner gets a valuation and hears a premium figure that sounds difficult but possible. A few weeks later, the actual budget starts to widen. Their own surveyor and solicitor need paying. The freeholder's reasonable legal and valuation costs usually land on the owner as well. There may also be an upfront deposit before the matter is settled. That is often the moment the whole exercise starts to feel far more expensive than expected.

The problem is not just that lease extensions cost money. It is that the number people hear first is rarely the full number.

A lease extension works a bit like planning a loft conversion. The builder's quote may be the main figure, but scaffolding, structural drawings, building control, and contingency decide what leaves your bank account. Leasehold owners face the same issue. The premium is only one part of the total cash outlay.

The figure that gets the attention first

The premium usually takes centre stage because it is the price of the new lease term itself. It is also the figure people naturally ask about first.

That can be misleading.

If you budget only for the premium, you can still run short once the process begins. A proper budget needs to include three layers from the outset:

- The premium paid for the lease extension itself

- Your professional fees, usually your surveyor and solicitor

- The freeholder's reasonable professional fees, plus any upfront deposit or Land Registry and notice costs

That fuller view is what turns a rough estimate into a usable budget.

Owners in the North West often find it helpful to pair valuation advice with local title and leasehold context, especially where ground rent clauses or older lease wording create extra questions. Local Preston leasehold property advice can help frame those practical issues early.

Why the process feels hard to price at first

Part of the discomfort comes from timing. The costs do not arrive in one neat invoice at the end. Some appear at the start, such as valuation advice. Some arise once the claim is underway, such as legal work and the landlord's costs. Some only become clear during negotiation, especially if there is a gap between your opening figure and the freeholder's view.

The valuation itself also feels abstract to first-time clients. Terms such as deferment rate, relativity, and marriage value can sound technical, even though they are different ways of measuring what the freeholder is giving up and what you are gaining. If you want a plain-English explanation of one of the biggest sticking points, Survey Merchant's marriage value article is a useful starting point.

There is another reason the bill feels larger than expected. You are not paying one person to produce one document. You are working through a legal and valuation process with several parties, each protecting their own position.

- Your surveyor assesses the likely premium and negotiates on value

- Your solicitor serves notices, checks deadlines, and completes the legal work

- The freeholder's surveyor and solicitor review the claim and charge reasonable fees that you often have to meet

- Your lender, if you have a mortgage, may need to be involved before completion

Seen that way, the cost starts to make sense. The surprise usually comes from the gap between the headline premium and the actual cash required to get from first advice to completed lease extension.

The Two Halves of Your Total Cost Premium and Fees

To budget properly for a lease extension, split the total cash outlay into two parts: the premium and the fees.

That sounds simple, but it is where many first-time leaseholders go wrong. They focus on the premium because it is the headline number, then discover later that the money needed to finish the job is higher once surveyor's fees, legal costs, the freeholder's costs, and the preliminary deposit are added in.

Premium means the price of the new lease term

The premium is the amount paid to the freeholder for the lease extension itself. Under a statutory claim, you are usually paying for a longer lease and the removal of future ground rent, which becomes a peppercorn, effectively £0.

So the premium is not just a charge for extra years on paper. It also reflects the fact that the freeholder is losing an income stream and waiting longer for the flat to return to them.

If you have already come across terms such as relativity, deferment, or marriage value, do not worry. They are valuation tools used to work out that price. Understanding leasehold valuations explains the mechanics in more detail.

Fees mean the cost of getting the extension completed

Fees sit around the premium, but they are part of the same real-world budget. A client does not complete a lease extension with the premium alone.

The usual costs include:

- Your surveyor's fee: for advice on the likely premium and negotiation with the freeholder's valuer

- Your solicitor's fee: for serving notices, checking title, dealing with the legal work, and completing registration

- The freeholder's reasonable legal and valuation fees: these are commonly payable by you under the statutory route

- The preliminary deposit: often payable after the claim starts, so cash is needed before the matter completes

- Possible lender and Land Registry costs: these can arise if you have a mortgage or if title updates are required

- Extra dispute costs: if the premium is argued over for longer than expected

This is why I encourage clients to ask a better question at the start. Not "What is the premium?" but "What is my total cash outlay likely to be?"

That approach helps in two ways. First, it gives you a more realistic budget. Second, it reduces the risk of starting the process and then running short of funds part way through.

For some owners, finance also becomes part of the picture, especially where the lease is already short and mortgage options are affected. If that applies to you, understanding short lease mortgages can help you see how the lease term may influence borrowing decisions.

A good early estimate separates these two halves clearly. One figure for the premium. One figure for all the surrounding costs. Add them together, and you have the number that usually matters most in practice: the amount of cash you will need to get from first advice to a completed lease extension.

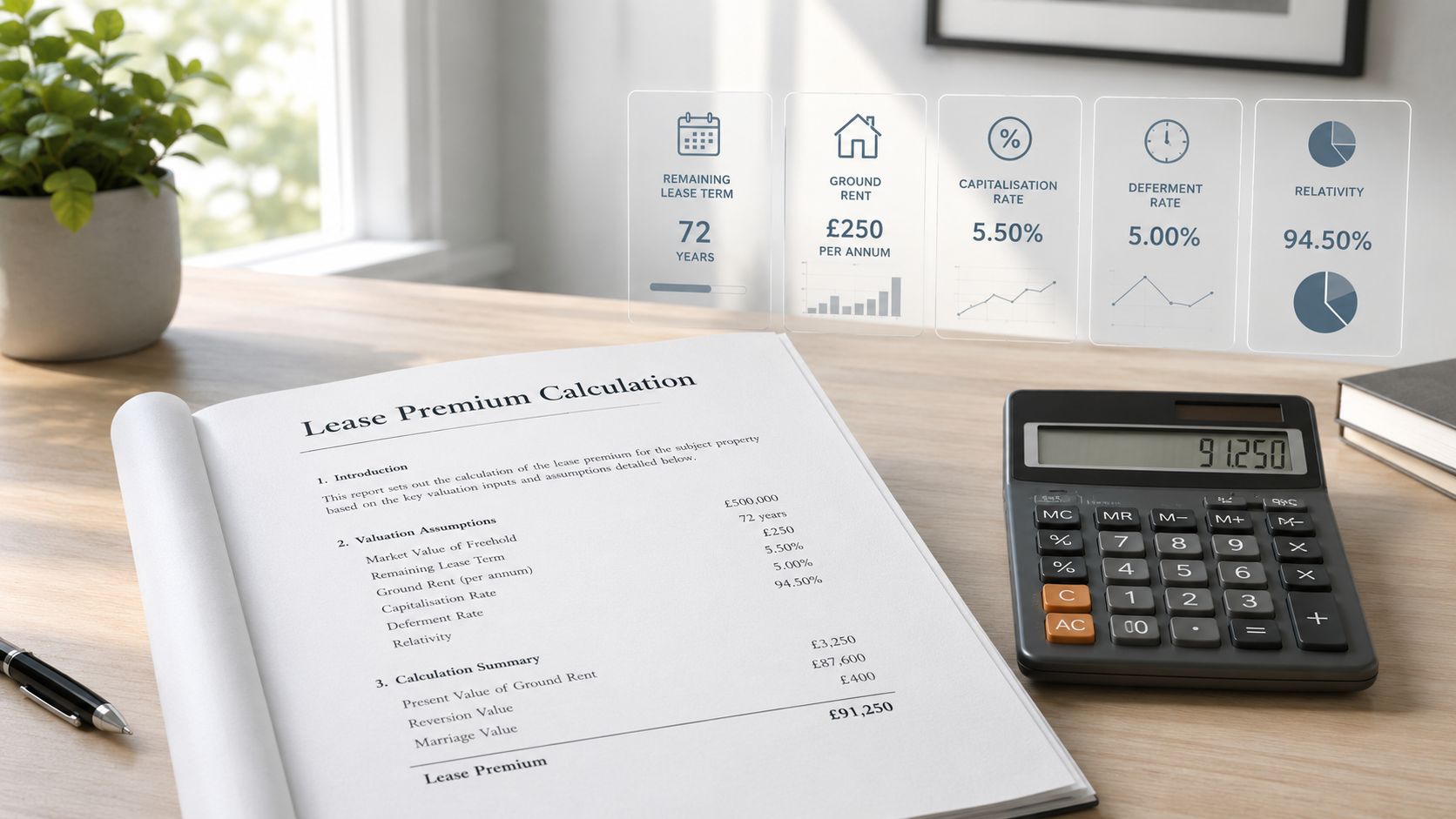

How the Lease Extension Premium is Calculated

You ask for a lease extension quote and the figure feels bigger than expected. The reason is that the premium is not a flat fee or a rough rule of thumb. It is a valuation exercise based on what the freeholder is losing and what your flat is gaining.

A helpful way to view the premium is as the price of reshaping the lease. The valuer is not only looking at the number of years left. They are also measuring how the extension changes value, ground rent, and the freeholder's interest.

What the premium is paying for

Several ingredients feed into the calculation, and each one can push the figure up or down:

- The years left on the lease. As the term gets shorter, the premium usually rises.

- The flat's market value. A more valuable flat often produces a higher premium.

- The ground rent terms. If the freeholder is losing future ground rent income, that loss forms part of the calculation.

- The statutory basis. A formal claim uses a legal valuation framework rather than a purely informal deal.

If the terminology feels technical, Understanding leasehold valuations gives a clearer explanation of the language surveyors use and how it affects the figure you are quoted.

Why 80 years matters so much

This is the point that catches many leaseholders out. Once the lease drops below 80 years, the calculation can include marriage value, and under the statutory route the leaseholder pays 50% of that uplift to the freeholder, according to Connaught Law in its lease extension calculator guidance.

Marriage value sounds more mysterious than it is. In practice, the flat with a longer lease is often worth more than the short lease and freeholder's separate interests taken apart. The law treats that extra uplift as a shared benefit.

A simple analogy helps here. Cutting a cake into slices does not change the total cake. Joining two pieces of property interest back together can increase the total value. Below 80 years, the freeholder is entitled to a share of that increase.

That is why surveyors often refer to the 80-year cliff. To an owner living in the flat, a lease with just over 80 years left and one with just under 80 years may feel much the same day to day. The valuation does not treat them the same way.

| Lease position | What usually drives the premium |

|---|---|

| Above 80 years | The value of the extra years and the loss of ground rent and reversion, without marriage value |

| Below 80 years | The same elements, plus marriage value and stronger short-lease pressure |

The practical message is clear. Checking your unexpired term early can save real money.

Why this matters for your cash planning

The premium is the largest line item in many cases, but it is only one part of the money you need. A higher premium also tends to raise the stakes in negotiation, which can increase valuation and legal work if the matter becomes drawn out.

Under the statutory route, the process starts with a Section 42 notice and each side usually takes valuation advice before negotiating the figure. If the dispute goes to the First-tier Tribunal, Connaught Law says tribunal fees can add £1,200 to £2,000. That will not apply in every case, but it belongs in a sensible budget.

So when you look at a premium estimate, treat it as the centre of the calculation, not the whole bill. Your real budgeting question is broader: what premium is likely, what deposit may be needed along the way, and what total cash outlay will get the matter from first advice to completion?

Worked Examples of Lease Extension Premiums

A flat owner often sees an online premium estimate and thinks, "That feels high, but manageable." Then the actual process starts. The premium is only the headline figure, and the examples below are most useful when you read them as the starting point for your total cash outlay, not the whole budget.

The quickest way to understand lease extension pricing is to compare two flats with broadly similar values but very different lease lengths. It works a bit like insurance excess or mortgage rates. A small change in the trigger point can alter the cost far more than you expect.

Two flats that start in very different places

Earlier in the article, we referred to published examples showing that a flat with a relatively healthy lease can attract a much lower premium than one with a much shorter term left. The exact figure for your property will depend on valuation inputs such as lease length, ground rent, property value, and how the freeholder's surveyor argues the case.

| Cost Component | Scenario A: 85 Years Remaining | Scenario B: 65 Years Remaining |

|---|---|---|

| Starting position | Lease still long enough for the premium to feel more contained | Short lease territory, where price sensitivity is much greater |

| Premium level | Often at the lower end of the range compared with shorter leases | Often materially higher, and sometimes sharply so |

| Main valuation pressure | Loss of ground rent and the freeholder's reversion are usually the main ingredients | Short-lease discount and marriage value can have a much stronger effect |

| What it means in practice | More room to plan, budget, and negotiate | Higher stakes, stronger urgency, and a larger total cash requirement |

That difference catches many first-time owners out.

Two flats can look similar in an estate agent's details. Same block, same layout, similar sale value. Yet one lease extension may feel like a planned maintenance cost, while the other feels closer to a capital project. The lease length is often the reason.

Here is the practical way to read these examples.

If your lease is around 85 years, the premium may still be significant, but it is usually easier to absorb. You are more likely to be dealing with a figure that sits within a planned savings pot, especially if you start early and keep the matter moving.

If your lease has fallen to around 65 years, the calculation becomes much less forgiving. At that stage, many owners focus on the premium alone and miss the wider cash picture. You may also need funds for your valuer, your solicitor, the freeholder's reasonable legal and valuation costs, and the statutory deposit that is usually paid after the formal claim is served. That is why "How much is the premium?" is only the first budgeting question.

A surveyor helps you answer the second question. "What might I need in cash to get this done?"

That is the figure that matters in real life.

For example, an owner with an affordable-looking premium estimate can still run into difficulty if they have not set aside money for the deposit and both sides' professional fees. By contrast, an owner who plans for the full outlay from the start is less likely to stall mid-process or accept a weak informal deal just because the extra costs came as a surprise.

If you are used to standard property appraisals, a general guide to house valuation cost helps explain how valuation fees are commonly structured, although lease extension work is more specialised because the surveyor is valuing legal rights as well as the flat itself.

The lesson from these examples is simple. Do not treat the premium as the whole bill. Treat it as the largest single part of a wider cash plan. That approach gives you a more realistic budget, a calmer negotiation position, and fewer unpleasant surprises once the claim is under way.

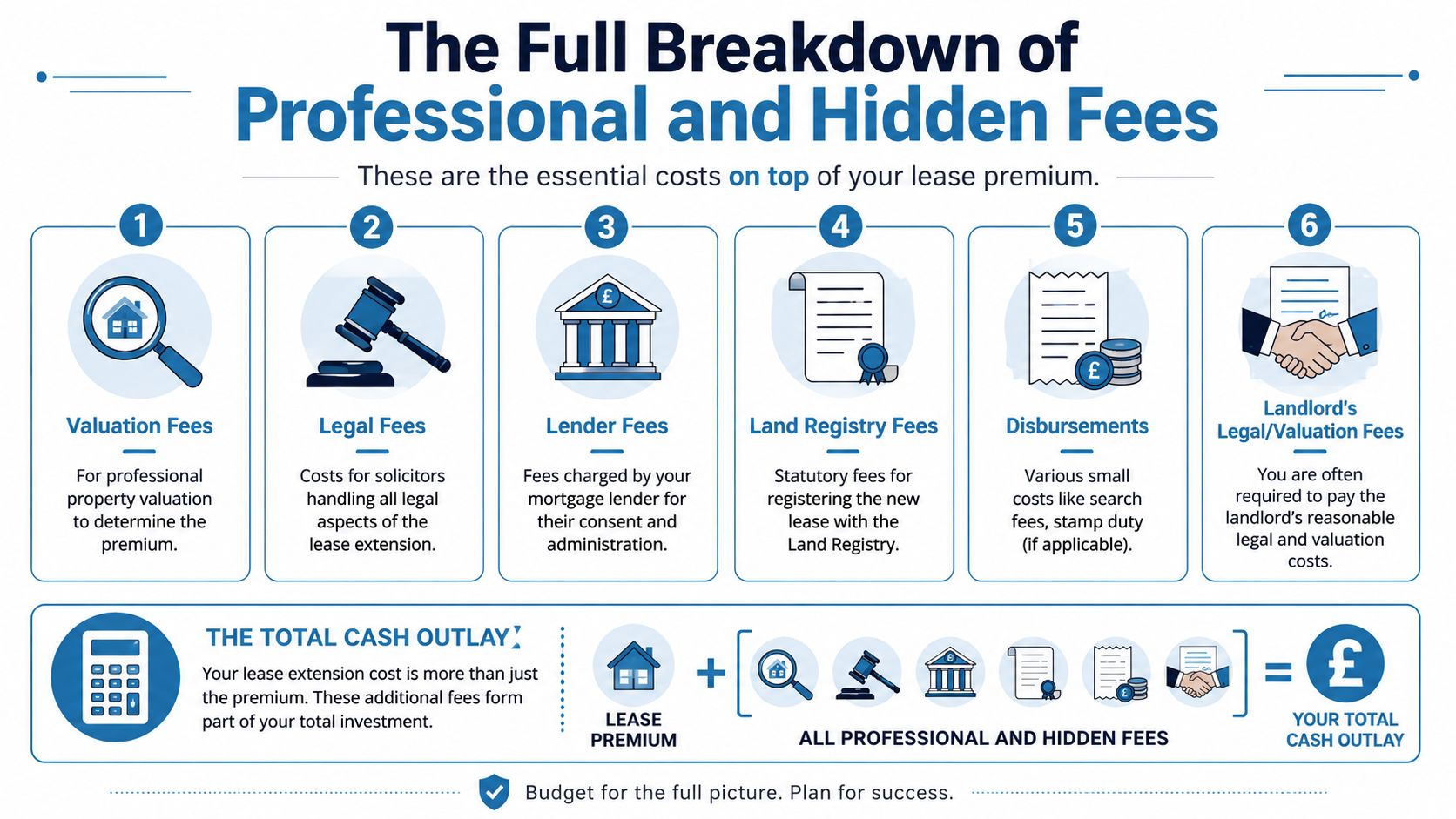

The Full Breakdown of Professional and Hidden Fees

A lease extension can look affordable on paper and still put real pressure on your bank account. The reason is simple. The premium is only one part of the bill. The total cash outlay also includes your own professional fees, the freeholder's reasonable costs, and money you may need to produce early in the process before the final figure is agreed.

The fees many owners budget for

Most owners expect to pay their own solicitor and surveyor. Fewer realise that a statutory claim usually means paying the freeholder's reasonable legal and valuation costs as well. Under Section 60 of the 1993 Act, those costs often sit with the leaseholder, so your working budget needs to cover both sides.

A useful way to view the costs is as four separate pots of money:

- Your valuer's fee. This covers advice on the likely premium, the opening figure to propose, and negotiation strategy.

- Your solicitor's fee. This covers the notice, title checks, legal process, completion, and registration.

- The freeholder's legal fee. You usually pay this if the costs are reasonable.

- The freeholder's valuation fee. You usually pay this as well, again subject to reasonableness.

If you're comparing surveyor pricing more generally, a guide on house valuation cost can help explain how valuation fees are often structured. Lease extension valuation is more specialised because the surveyor is valuing the leaseholder's rights and the freeholder's interest, not only the flat's market value.

The costs that catch owners off guard

The biggest surprise is often timing, not just amount.

Under the formal route, a landlord can require a deposit after the tenant's notice is served. That preliminary deposit is commonly 10 percent of the premium proposed in the notice, subject to the statutory minimum. In practice, that means a low opening offer can reduce the deposit, but an unrealistically low offer can weaken your credibility from the start. Getting the notice figure right matters for both valuation and cash flow.

Some owners also spend money before the claim has real momentum. You may pay for valuation advice early, and if matters become drawn out, extra negotiation time can add to the bill. A matter that looked neat at the start can become more expensive because the parties are further apart than expected.

I often advise clients to think in layers:

- Layer 1: Premium. The final sum for the new lease.

- Layer 2: Professional fees. Your surveyor, your solicitor, and the freeholder's advisers.

- Layer 3: Upfront cash. The statutory deposit and any early-stage costs you must pay before completion.

- Layer 4: Contingency. Extra spend if negotiations drag on or documents reveal complications.

That layered approach works like planning a house move. The purchase price matters, but so do stamp duty, legal fees, removals, and the deposit you need at the start. A lease extension is similar. If you budget only for the headline number, the smaller items can still stop the transaction.

Why this matters in practice

A client may receive a premium estimate that feels manageable, then discover they need several thousand pounds more for fees and upfront payments before the matter completes. That is often the point at which people pause, borrow in a rush, or accept an informal proposal without testing whether the terms are better.

A clearer budget helps you stay in control. You can decide whether to start now, wait and save, or ask your surveyor and solicitor to map out the likely cash calls by stage. If you want a practical overview of the steps involved, this guide on how to extend a property lease is a helpful companion to the cost planning.

This defines the total cash outlay. You are measuring the final bill and the cash you must have available along the way.

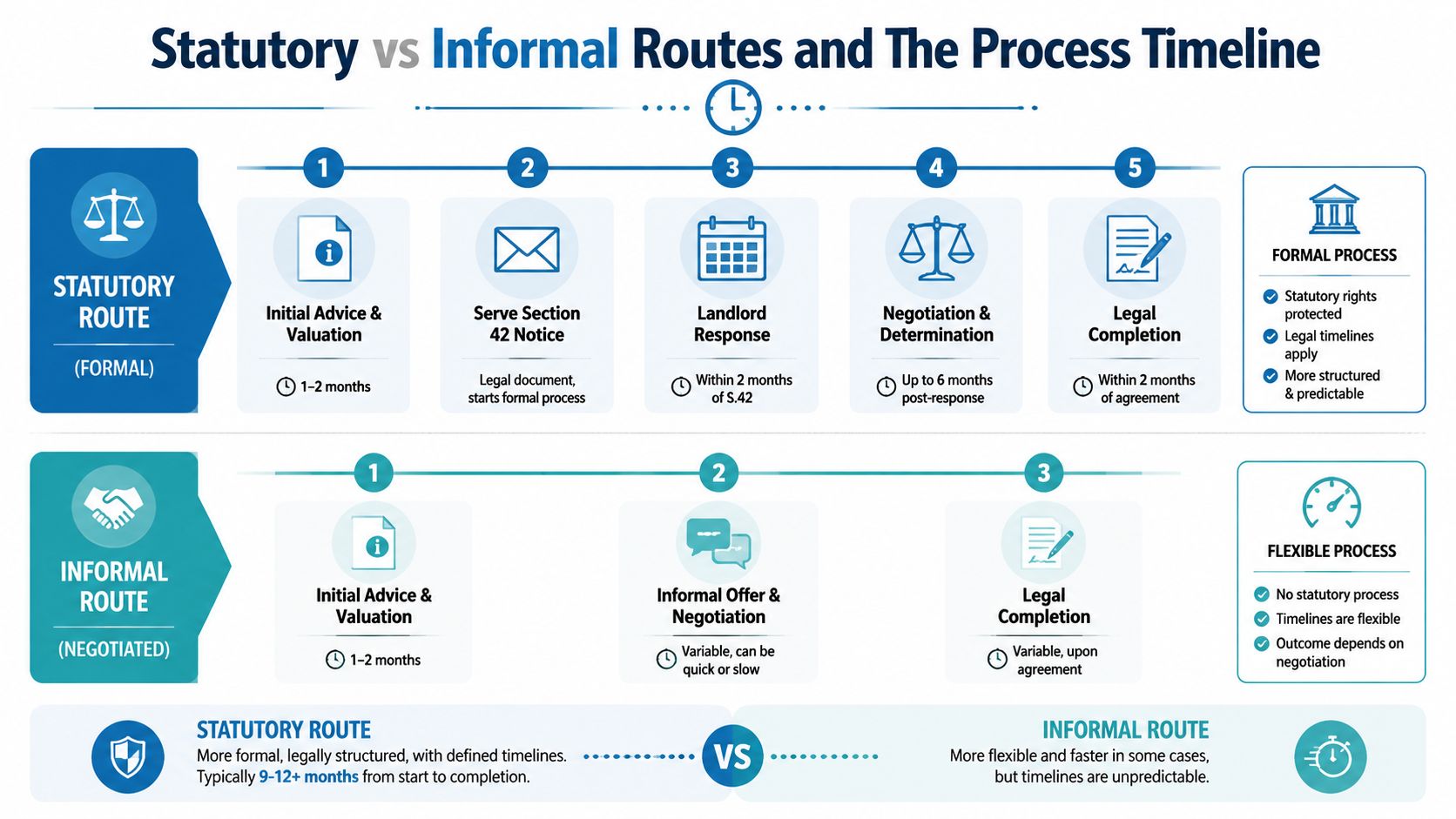

Statutory vs Informal Routes and The Process Timeline

Once you understand the likely outlay, the next question is route. Most owners have two broad options. They can proceed formally under the statutory framework, or they can try an informal deal direct with the freeholder.

How the two routes differ

The statutory route is the formal path. It starts with a Section 42 notice and gives a legal structure for the claim, negotiation, and completion. The big attraction is certainty of framework. You know the process, you know the rights involved, and there is a tribunal route if agreement cannot be reached.

The informal route can be quicker and more flexible. But flexibility cuts both ways. A freeholder may offer terms that sound attractive at first and then attach less favourable lease wording, or change position before completion.

A plain comparison helps:

| Route | Strength | Risk |

|---|---|---|

| Statutory | Legal protections and defined process | More formality and professional input |

| Informal | Potentially simpler negotiation | Terms may be less favourable or unstable |

If you want a practical overview of the steps involved before deciding, this guide on how to extend a property lease is a useful companion.

What the process feels like in practice

The timeline can feel slow because several parties need to act in sequence. Under the statutory route, there is usually an initial advice stage, then the notice, then the landlord's response, then a period of negotiation, and finally legal completion and registration.

The informal route can move faster if the freeholder is cooperative. It can also drift, restart, or produce terms that need detailed legal review. In that sense, "faster" and "cheaper" aren't always the same as "better".

If the freeholder's opening tone is friendly, that's helpful. It isn't a substitute for valuation advice or careful legal drafting.

For first-time owners, the safest mindset is to choose the route that matches your priority. If your priority is legal certainty, the statutory route usually gives more structure. If your priority is speed and the freeholder is straightforward, an informal discussion may be worth exploring first, provided your solicitor reviews the proposed terms carefully.

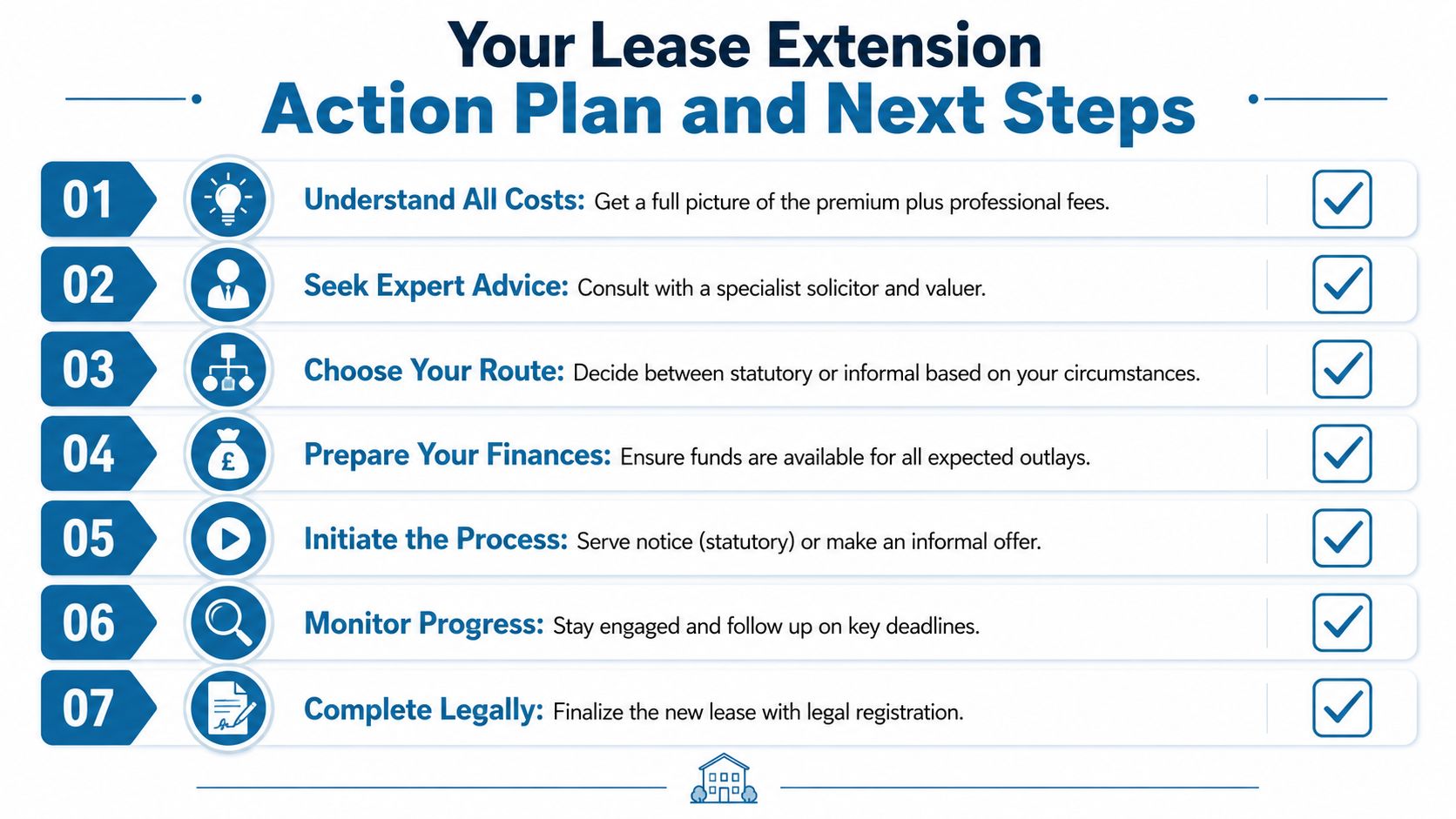

Your Lease Extension Action Plan and Next Steps

A good lease extension starts with preparation, not paperwork. Most problems I've seen arise because the owner started too late, budgeted too tightly, or relied on an untested figure from a quick online conversation.

A practical checklist

Use this as your working plan:

- Check your lease term: Confirm how many years remain. Don't rely on memory or an old sales detail.

- Gather the key documents: Your lease, title documents, ground rent details, and mortgage information all help your advisers move faster.

- Get an independent valuation: This is the foundation of the whole job. You need a specialist opinion before discussing figures with the freeholder.

- Speak to a solicitor early: Deadlines and notices matter. Early legal advice prevents procedural mistakes.

- Budget for total cash outlay: Include the premium, your fees, the freeholder's fees, and upfront cash demands.

- Choose your route carefully: Decide whether statutory protection or informal negotiation suits your circumstances.

- Track the process actively: Keep in touch with your surveyor and solicitor, and don't let avoidable delays eat into your lease term.

The video below gives a useful overview for owners who want to see the process discussed in plain language.

One timing question to raise early

There is one strategic issue worth discussing at the very start. The government guidance indicates that the pending Leasehold Reform Act, expected in 2025 to 2026, aims to abolish marriage value, which could significantly reduce extension costs, according to the official guidance on extending, changing or ending a lease.

That doesn't mean everyone should wait. Timing depends on your current lease length, your sale or remortgage plans, and how much risk you can tolerate. If your lease is already under pressure, waiting for reforms may not be the right move. But it is absolutely a question to put to your surveyor before you commit.

A calm, well-run lease extension usually comes from doing the obvious things well:

- Know your lease position

- Get a proper valuation

- Budget beyond the premium

- Take legal advice before agreeing terms

If you do those four things, extending leasehold costs become far more manageable because you understand not just the headline number, but the whole transaction around it.

If you're ready to start, the smartest first move is to get an independent specialist valuation through Survey Merchant. They can connect you with a qualified surveyor who understands lease extension valuation, explains the likely premium and full cash outlay in plain English, and helps you approach the process with a realistic plan rather than guesswork.