Leasehold

Jul 16, 2026

Marriage Value Lease: Avoid Costly Premiums

Navigate marriage value lease in UK law. Learn its impact, calculation, and how to avoid high premiums when your lease is below 80 years.

You own a flat you’re happy in. The mortgage is manageable, the location works, and you’ve always assumed you’d sort the lease extension “soon”. Then a valuation comes back, or the freeholder’s figure lands, and the cost is far higher than you expected. Often the shock arrives when the lease is hovering around the low-80s or has just slipped under a line many owners have never been properly warned about.

That line is where marriage value lease issues start to bite. It sounds like legal jargon because it is legal jargon, but the effect is painfully practical. Delay can push up the premium, narrow your negotiating room, and make the flat harder to sell or remortgage. If you only remember one thing, remember this. Timing is not a side issue in leasehold work. Timing is the strategy.

A common call goes like this. The owner says the lease has 81 years left, so they assume there’s no real urgency. They make a few enquiries, leave it for a while, then come back after another birthday, another service charge cycle, another busy season at work. Suddenly the numbers look very different, and the phrase they keep hearing is marriage value.

That surprise catches people because the flat still feels the same. Same kitchen, same view, same building, same address. But leasehold value isn’t just about bricks and mortar. It is also about time. As the lease term shortens, the legal interest you own becomes less valuable, and once you cross the key threshold, the law can require you to share part of the uplift created by the extension with the freeholder.

Practical rule: A lease can feel healthy to an owner while already being in the danger zone financially.

Owners often get frustrated. They think, reasonably enough, that extending the lease should mean paying for the extra term. In reality, the premium can include other valuation elements, and marriage value can become the part that changes the conversation from “annoying but manageable” to “why is this suddenly so expensive?”

Three things usually follow that first shock:

If your lease is already in the low-80s, you’re not being alarmist by looking into it now. You’re being sensible. In leasehold matters, acting early isn’t overcautious. It’s often the cheapest decision you’ll make.

Marriage value is the increase in a flat’s market value when a lease extension brings the leaseholder’s interest and the freeholder’s interest together on better terms.

In plain English, a short lease usually drags down what a buyer will pay. Once that lease is extended, the same flat often becomes more valuable because it is easier to sell, easier to mortgage, and closer in appeal to a long-lease property. That increase in value is the “marriage value”.

The term refers to two separate legal interests. The leaseholder owns the right to live in the flat for the years left on the lease. The freeholder owns the reversionary interest, which is the long-term ownership that comes back into full control when the lease expires. A statutory lease extension changes both positions. The leaseholder gets a longer, more marketable asset. The freeholder gives up part of that future interest. The law treats the uplift as something created by those interests combining.

A practical comparison often helps here. A flat with a short lease can trade like a product with an expiry date that is getting uncomfortably close. Extend the lease, and you push that date far enough away that buyers and lenders stop worrying in the same way. The flat itself has not changed physically, but its market position has.

That is why marriage value matters to your wallet, not just your solicitor’s paperwork.

For many leaseholders, the frustration is obvious. You are paying for the lease extension, yet part of the gain can be shared with the freeholder. The reasoning is that the extension does not create value from the leaseholder’s side alone. It also reduces the value of the freeholder’s future rights, so the law splits part of the uplift between the two parties.

In short:

Where this becomes a strategic issue is timing. Owners often assume marriage value is only a problem once the lease looks obviously short. In practice, the sensible window for review starts earlier. If your lease is sitting around 82 to 85 years, that is usually the point to get valuation advice, check eligibility, and decide whether to act before the cost base worsens.

A good surveyor will not look at marriage value as an abstract legal phrase. They will look at it as a timeline issue. Every year you wait, the lease can become less attractive to the market and more expensive to correct. That is why experienced leaseholders treat marriage value as an early warning sign, not a last-minute surprise.

The most important line in this whole subject is 80 years. In UK leasehold law, marriage value becomes payable when a residential lease falls below 80 years remaining, significantly increasing the cost of statutory lease extensions under the Leasehold Reform, Housing and Urban Development Act 1993. The leaseholder must pay 50% of that marriage value to the freeholder, and a commonly cited illustration shows a property valued at £300,000 with a 99-year lease potentially falling to 85% of that value, or £255,000, at 70 years, creating £45,000 in marriage value, with £22,500 payable to the freeholder according to the marriage value summary.

Clients often ask whether 80 years and a few months is “basically the same” as 79 years and a few months. Legally and financially, it isn’t.

That’s why surveyors describe it as a cliff edge. Above the threshold, marriage value is taken as nil for the statutory calculation. Below it, a new and often expensive component enters the premium. The flat hasn’t changed physically overnight, but the valuation basis has.

This is also why timing beats haggling. A strong negotiation helps, but it can’t undo the effect of crossing the line if the statutory valuation date falls after the lease drops below it.

The practical protection many leaseholders need to understand is the Section 42 notice. If served in time, it fixes the valuation date by reference to that notice. In plain terms, that can stop the clock for valuation purposes even if the legal process itself carries on afterwards.

If you’re already approaching the line, good professional coordination is of paramount importance. Your valuer and solicitor need to work in step, not in sequence.

Here’s the broad logic:

Check the lease term properly

Don’t rely on memory, a sales brochure, or an old mortgage offer.

Get a valuation before you react to the freeholder

A formal valuation gives you a grounded opening position.

Serve the statutory notice in time if that route suits your case

Timing can be more valuable than trying to shave a little off the premium later.

A short visual explanation often helps:

Owners often focus on the premium figure. The bigger issue is the valuation date behind that figure.

The lesson is simple. If your lease is anywhere near the threshold, don’t treat this as paperwork you can leave until next quarter. The 80-year rule is where leasehold theory hits your wallet.

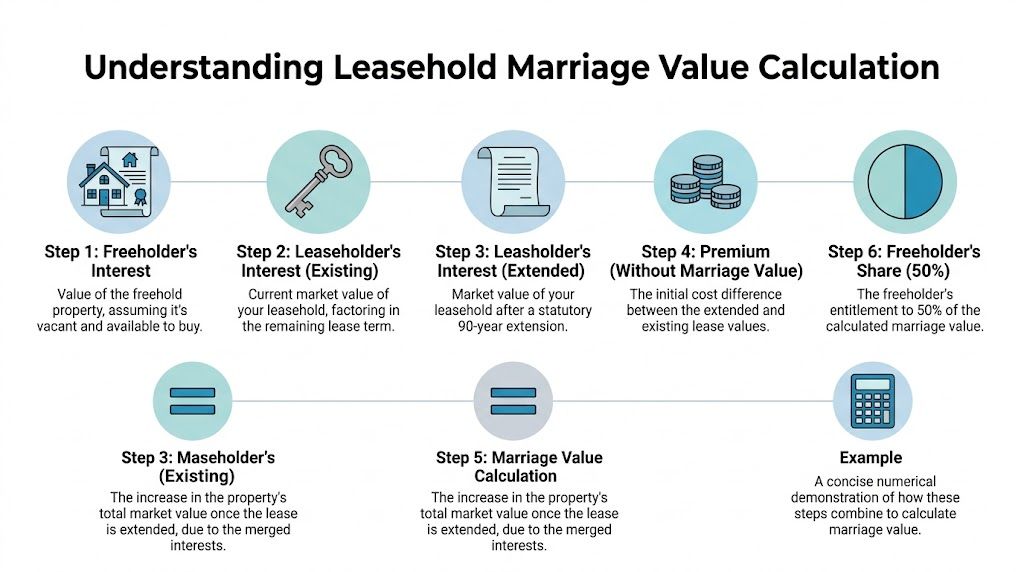

A marriage value calculation answers one practical question. How much extra value is created when a short lease is turned into a long one, and how is that gain split?

For leaseholders, this matters because the bill can change sharply once the term has fallen below 80 years. The calculation is technical, but the logic is not. A short lease and the freeholder’s interest sit side by side like two separate pieces of a property puzzle. Extend the lease, and those pieces fit together more profitably. Under the statutory method, the freeholder is entitled to half of that uplift.

A surveyor will usually break the exercise into four moving parts:

The difference between the combined “before” figure and the combined “after” figure is the uplift. Under the statutory approach, marriage value is 50% of that uplift.

That sounds abstract, so it helps to put it into ordinary language. A flat with a short lease is often worth less than the same flat with a long lease. The freeholder also holds value because they will one day get the property back and may receive ground rent in the meantime. Once the lease is extended, the leaseholder’s interest becomes more valuable and the freeholder’s position changes. The law measures that change and divides the marriage value element equally.

If you want a practical sense check before instructing a valuer, this lease extension value estimator guide gives a useful overview of the pricing mechanics.

Take a flat worth £150,000 with a short lease. After a lease extension, suppose it would be worth £200,000. The uplift is £50,000. If that uplift were treated entirely as marriage value for a simplified example, the freeholder’s 50% share would be £25,000.

That example is useful for understanding the principle, but real valuations are less tidy. A surveyor does not just compare sale prices and stop there. The calculation also has to reflect the freeholder’s existing interest and the terms of the current lease.

Here is a second example using larger numbers. Suppose a flat with a short lease is worth £255,000, but with a long lease it would be worth £300,000. The uplift is £45,000. On the same simplified basis, the freeholder’s 50% share would be £22,500.

| Example | Short lease value | Extended lease value | Uplift | 50% share |

|---|---|---|---|---|

| Flat example | £150,000 | £200,000 | £50,000 | £25,000 |

| Higher-value illustration | £255,000 | £300,000 | £45,000 | £22,500 |

The point is not that your premium will match either figure. It is that delay becomes expensive fast. Once marriage value is in play, even a modest increase in value can produce a meaningful extra cost.

Many leaseholders look only at what the flat might be worth after extension and subtract today’s value. That is a rough classroom version of the idea, not a figure to negotiate from.

A proper valuation also considers:

In practice, the hardest part is not the arithmetic. It is judging the inputs. Small changes in relativity, deferment, or comparable evidence can move the premium by thousands.

That is why timing matters as much as method. If your lease is in the low 80s, the smart move is usually to value early, while you still have options, rather than wait until the numbers harden against you.

A common pattern goes like this. A flat owner notices the lease has slipped to 81 years, assumes there is still plenty of time, and waits until a sale or remortgage forces action. By then, the timetable is tighter, the negotiation is harder, and the premium is usually less forgiving.

The practical window is earlier than many people expect. Start at around 82 to 85 years. That period gives you time to confirm the lease term, obtain valuation advice, consider the right route, and act before delay starts costing real money. In survey terms, it is the difference between planning a job and firefighting one.

I usually explain the process as a staged plan rather than a single event. A lease extension is closer to preparing for a house move than buying an insurance renewal. The earlier you organise papers, advice, and timing, the more control you keep.

At about 85 years

Check the lease term from the actual lease and title documents, not from memory or an old sales brochure. This is also a sensible point to review the wider lease terms, including rent provisions. If you want a straightforward explanation of that part of the lease, What is ground rent UK? covers the basics clearly.

At 83 to 82 years

Instruct a RICS-chartered valuer and a solicitor who handles lease extensions regularly. This is the stage for understanding likely premium ranges, documents needed, and whether the statutory or informal route makes better sense for your position.

Before 80 years

If the statutory route is suitable, leave enough time for the formal notice to be prepared and served properly. Waiting until the clock is nearly at 80 often turns a manageable job into a rushed one.

Lease extension negotiations have two tracks running at the same time. One is valuation. The other is procedure. If either track slips, the other usually suffers as well.

Start with a valuation you can defend. A freeholder is unlikely to reduce their figure because you feel it is too high. They are more likely to move when your surveyor can point to comparable evidence, lease terms, and accepted valuation assumptions.

Then get the legal timing right. Missing a date or approaching the freeholder too casually at the wrong stage can weaken your position before the actual negotiation has started. Clients often assume the difficult part is agreeing the number. Often, the more expensive mistake is poor sequencing.

A calm response matters too. The opening figure from the freeholder is often a negotiating position, not the number the matter will settle at. Good advice helps you separate a realistic counter from a figure that wastes time.

If you want a clearer explanation of how offers, counter-offers, and sticking points are usually handled, this ultimate lease extension negotiations guide is a useful next step.

One point is easy to miss. Delay does not only affect the premium. It can also reduce your room to negotiate, especially if a transaction deadline is approaching and the freeholder knows you are under pressure.

Early instruction improves options. It gives your valuer time to inspect and analyse the evidence properly, and it gives your solicitor time to keep the process on track. That combination often saves more money than people expect.

Leaseholders often hear that marriage value is “being abolished” and assume it’s safe to wait. That’s risky thinking. Reform discussions have been active for some time, but the current legal position still matters when you’re making decisions today.

Marriage value is a leasehold enfranchisement concept tied to the statutory framework for residential lease extension and related rights. It isn’t a catch-all charge for every property with a time-limited interest.

In practice, the first question is always what kind of property interest you hold and what rights apply to it. Some owners assume every short lease has the same route and the same valuation treatment. It doesn’t.

The reform debate has centred heavily on the 80-year threshold. Government proposals to abolish marriage value for leases under 80 years have been discussed, but legal hurdles remain. The 2016 Upper Tribunal rulings in Sloane Stanley Estate v Mundy & Lagesse and Aaron v Wellcome Trust Ltd rejected lower valuations and enforced methods that favoured freeholders, according to this Simmons & Simmons analysis of leasehold reform and enfranchisement.

That matters because some owners delay in the hope that tomorrow’s law will be cheaper than today’s. It might be. It might not. Freeholders have argued that abolition interferes with property rights, and wider reform proposals have also included changes to capitalisation and deferment rates. One adjustment can reduce cost in one area while another can affect value elsewhere.

For a broader look at the changing legal situation, this leasehold reform update from January 2024 helps frame the uncertainty.

The practical conclusion is not especially glamorous, but it is reliable. Make decisions on the law that applies now, not the law you hope might arrive in time.

This happens more often than people expect, especially where ownership has changed hands or management is poor. The answer isn’t to ignore the problem. Speak to a solicitor with lease extension experience. There are legal routes for dealing with absent freeholder situations, but they need to be handled properly and early because delay still harms the leaseholder’s position.

Sometimes yes, sometimes with difficulty. Lenders grow more cautious as the term shortens, and that caution can affect marketability and resale as well as finance. In practical terms, that means fewer willing buyers, more questions during conveyancing, and more pressure on price negotiations.

It depends on the facts. An informal deal can sometimes move faster and feel more flexible, but flexibility isn’t always your friend if the proposed terms introduce something unfavourable elsewhere in the lease. The statutory route is more structured and can give clearer legal protections, especially where timing around the key threshold matters.

A good rule is this:

The premium is only one part of the picture. Most leaseholders should also budget for their own valuation fees, their own legal costs, and the freeholder’s reasonable professional costs where the law requires them to be met. The exact mix depends on the route taken and how straightforward the matter becomes.

There isn’t one universal timetable. Some matters settle by agreement without major friction. Others drag because the parties start too late, dispute value aggressively, or let deadlines slip. The sooner you instruct the right professionals, the more control you usually keep over the process.

If your lease term is already causing you stress, the answer is usually not to wait for clarity. The answer is to create clarity.

If your lease is edging towards the low-80s or has already dropped below that point, a professional valuation can help you understand the likely premium, decide whether to serve notice, and negotiate from evidence rather than guesswork. Survey Merchant connects property owners with UK surveyors for lease extension and enfranchisement instructions, including RICS valuation work where marriage value may be in play.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes