Valuation

Jul 16, 2026

Insurance reinstatement valuation: a 2026 property guide

Discover the essential guide to insurance reinstatement valuation for 2026. Ensure your property is fully protected against rising costs!

Insurance reinstatement valuation is defined as the total cost to completely rebuild a property from the ground up after a total loss, covering all construction, demolition, professional fees, and statutory compliance. This figure is distinct from market value or purchase price, and using the wrong number as your sum insured is one of the most common and costly mistakes property owners make. In 2026, with construction costs rising sharply across the UK, getting this valuation right matters more than ever. Whether you own a Victorian terrace, a commercial warehouse, or a listed building, an accurate reinstatement cost assessment is the foundation of any credible insurance policy.

An insurance reinstatement valuation covers far more than bricks and mortar. The full scope divides into hard costs, soft costs, and statutory requirements, and missing any category leaves you exposed.

Hard construction costs form the core of the valuation. These include all materials, labour, and site work needed to physically reconstruct the building to its original specification. For a standard residential property, this typically covers foundations, structural frame, roofing, external and internal finishes, and building services such as plumbing and electrics.

Soft costs are where many owners and buyers are caught out. Soft costs such as demolition, debris removal, architects’ and engineers’ fees, and statutory approvals can constitute 15–25% of the total reinstatement cost. That is a significant uplift that generic online calculators routinely ignore.

The full list of components includes:

Statutory and compliance costs add another layer. Buildings must be reconstructed to current Building Regulations standards, not those in force when the property was originally built. This can add meaningful cost to older properties where original construction predates modern fire, thermal, or structural requirements.

Pro Tip: Never assume your buildings insurance sum insured matches your reinstatement cost. Request a formal reinstatement cost assessment from a RICS-qualified surveyor before your next renewal, not after a claim.

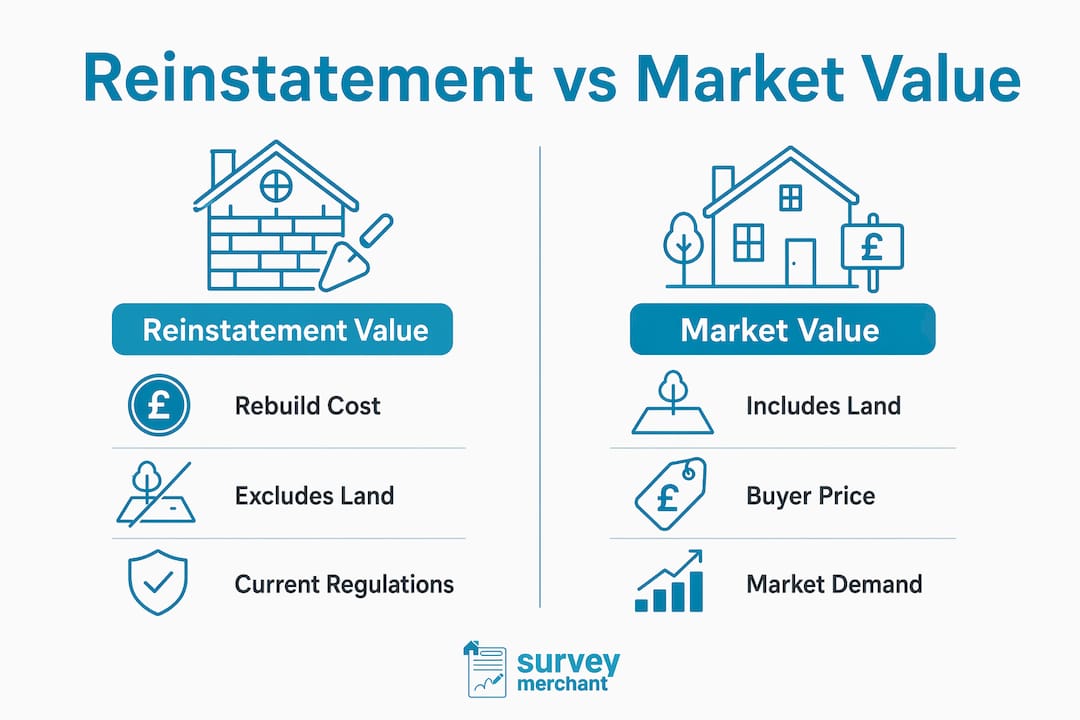

Market value and reinstatement cost measure entirely different things. Market value reflects what a willing buyer pays for a property, including the land it sits on. Reinstatement cost focuses solely on the physical cost of rebuilding the structure. Land is not destroyed in a fire. You do not need to insure it.

The table below shows how these three figures can diverge for the same property:

| Measure | What It Represents | Typical Relationship to Rebuild Cost |

|---|---|---|

| Market Value | Price a buyer pays, including land | Often higher in urban areas |

| Purchase Price | Agreed transaction price | May reflect demand, not rebuild cost |

| Reinstatement Cost | Full rebuild cost, no land element | The only correct basis for insurance |

Property owners frequently use purchase price as their insurance sum insured. This creates two distinct problems. In high-demand locations such as central London, market value far exceeds rebuild cost, so owners overpay on premiums for years. In lower-demand areas or for properties with high specification finishes, rebuild cost can exceed market value, leaving owners severely underinsured.

Location compounds the divergence. A Georgian townhouse in Bath may carry a market value of £900,000, with land accounting for £350,000 of that figure. The reinstatement cost may be £650,000. Insuring for the full market value wastes premium. Insuring for the land-inclusive figure does not protect you from the rebuild shortfall if the property is a total loss.

The insurance valuation process must therefore start with a clear separation of land value from structural rebuild cost. Only then can you set a sum insured that genuinely reflects your exposure.

The case for professional involvement is straightforward. Online rebuild calculators provide only indicative estimates and fail to capture site-specific or heritage-related complexities. A figure generated in two minutes online is not a defensible sum insured when a claim reaches six or seven figures.

A professional reinstatement cost assessment, conducted by a RICS-qualified surveyor or chartered quantity surveyor, follows a structured process:

RICS guidance on reinstatement insurance valuation confirms that professional assessments are particularly critical for complex, historic, or large-scale commercial properties. Standard BCIS calculators miss important nuances around access constraints, non-standard construction, and heritage compliance. The RICS Red Book valuation standards provide the professional framework within which formal assessments are conducted, giving insurers confidence in the resulting figure.

Frequency matters too. Insurers in 2026 enforce strict insurance-to-value ratios with annual portfolio reviews to account for rapid construction cost inflation. A valuation conducted three years ago may now understate your rebuild cost by 20% or more. The standard recommendation is a full professional assessment every three years, with index-linked adjustments applied annually in between.

Expert valuations establish auditable, defensible sums insured that reduce claim disputes and reputational risk. The time to establish the correct figure is before a loss occurs, not during a claim when the pressure is highest.

Pro Tip: Ask your surveyor to provide the reinstatement valuation in a format your insurer or broker can reference directly. A well-structured report removes ambiguity at the point of claim.

Getting the valuation is only half the task. Applying it correctly to your insurance policy is where the financial protection is actually secured.

The core steps for using your property reinstatement value effectively are:

Consider a practical scenario. A commercial property owner insures a warehouse for £1.2 million based on the original purchase price. A professional reinstatement cost assessment establishes the true rebuild cost at £1.8 million. A fire causes £600,000 of damage. Under the Average Clause, the insurer pays only two-thirds of the claim, approximately £400,000. The owner faces a £200,000 shortfall from a single avoidable error in the insurance valuation process.

The Reinstatement Value Clause requires insurers to pay new replacement cost without depreciation, provided the sum insured reflects the full reinstatement cost. Fall short of that figure and the policy reverts to a lower, depreciated settlement. The financial gap can be substantial for older buildings with significant accumulated depreciation.

Heritage and listed buildings present a distinct set of challenges in the valuation for insurance claims. Standard cost data does not apply, and the consequences of undervaluation are severe.

The key cost drivers for heritage properties include:

Heritage building owners face increased reinstatement costs due to compliance with traditional materials and slower construction, making specialist professional teams essential. A standard valuation conducted without heritage expertise will almost certainly understate the true rebuild cost. Heritage compliance uplifts and extended timelines increase total costs beyond normal valuation assumptions, and these uplifts are not captured by generic calculators or non-specialist surveyors.

Professional assessments for complex or historic properties require multidisciplinary teams including conservation architects and heritage consultants. This is not an optional extra. It is the only way to produce a figure that genuinely reflects the cost of rebuilding a listed or historic property to the standard required by law.

Accurate insurance reinstatement valuation requires a professionally assessed rebuild cost that includes hard construction, soft costs, and compliance uplifts, set independently of market value or purchase price.

| Point | Details |

|---|---|

| Reinstatement cost is not market value | Land value is excluded; only physical rebuild costs determine the correct sum insured. |

| Soft costs add 15–25% | Demolition, professional fees, and compliance uplifts must be included in every assessment. |

| The Average Clause penalises underinsurance | Insuring below true rebuild cost reduces claim payouts proportionally, creating a direct financial loss. |

| Professional assessments are non-negotiable | RICS-qualified surveyors produce defensible, auditable figures that online calculators cannot match. |

| Heritage properties need specialist teams | Conservation architects and heritage consultants are required to capture true rebuild costs for listed buildings. |

In my experience working across the UK property sector, the single most persistent mistake is treating the purchase price as a proxy for the rebuild cost. It is an understandable shortcut. The purchase price is a number you know, it is on the contract, and it feels like a reasonable anchor. The problem is that it has almost no relationship to what it would actually cost to reconstruct the building.

I have seen commercial property owners insured for figures that were accurate a decade ago and never reviewed. I have seen residential buyers set their buildings insurance sum insured at the mortgage valuation figure, which is a lender’s risk assessment, not a rebuild cost. Both errors leave owners exposed in ways they do not discover until a claim is refused or reduced.

The other pattern I see regularly is owners of older properties assuming their buildings are worth less to rebuild because they are “just old houses.” The opposite is often true. Older properties frequently use non-standard construction methods, have thicker walls, higher ceilings, and period features that cost considerably more to replicate than modern equivalents. A 1930s semi-detached in good condition can carry a rebuild cost that surprises its owner.

My advice is direct. Commission a professional reinstatement cost assessment from a RICS-qualified surveyor before your next renewal. Review it every three years. Apply index-linked adjustments annually. Treat it as part of your property risk management, not a one-off administrative task. The cost of a professional assessment is negligible compared to the financial exposure of getting it wrong.

— Surveymerchant

Surveymerchant connects property owners and buyers with RICS-qualified surveyors who specialise in insurance reinstatement valuations across residential and commercial properties throughout the UK.

Whether you own a standard residential property, a commercial building, or a listed heritage asset, Surveymerchant’s panel of expert surveyors produces formal, defensible reinstatement cost assessments that satisfy insurer requirements and protect you at the point of claim. Every assessment accounts for hard construction costs, soft costs, and statutory compliance uplifts. Explore Surveymerchant’s RICS valuation services or find out more about commercial property surveys tailored to your specific building type and insurance needs.

An insurance reinstatement valuation is the calculated cost to fully rebuild a property after total destruction, covering all construction, demolition, professional fees, and statutory compliance. It excludes land value and differs from market value or purchase price.

A full professional assessment is recommended every three years, with index-linked adjustments applied annually. In 2026, rising construction costs mean outdated valuations carry a significant risk of underinsurance.

Insurers apply the Average Clause, which reduces your claim payout proportionally to the shortfall between your sum insured and the true reinstatement cost. If you are insured for 70% of the actual rebuild cost, you receive only 70% of any valid claim.

For standard properties, indicative figures from BCIS calculators may suffice as a starting point, but a RICS-qualified surveyor is required for complex, commercial, or heritage properties to produce a defensible and accurate sum insured.

Market value includes land and reflects buyer demand, while reinstatement cost covers only the physical rebuild of the structure. In high-demand urban areas, market value typically exceeds rebuild cost; for high-specification or heritage properties, the reverse can apply.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes