Valuation

Jul 16, 2026

Cost of Reinstatement: A 2026 UK Property Guide

What is the cost of reinstatement for your property? Our 2026 guide explains how it's calculated, why it differs from market value, and how to get it right.

Your renewal notice arrives. The insurer asks for a sum insured. You glance at the purchase price, maybe check a portal estimate, and pick a figure that feels sensible. That's how many owners end up exposed.

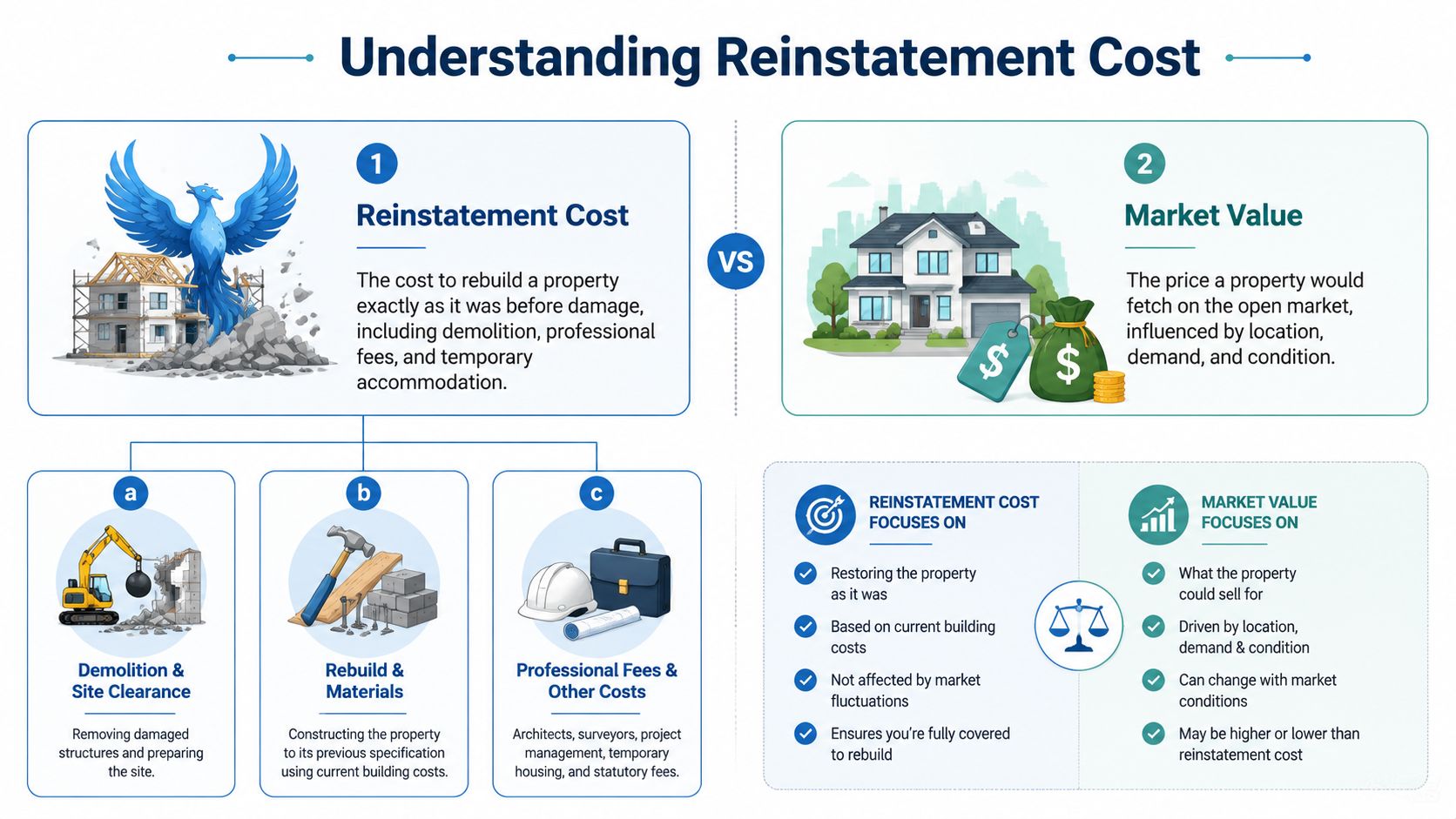

The problem is simple. Your property's market value is not its insurance value. One reflects what a buyer would pay for the plot, the location, and the building as a whole. The other reflects what it would cost to put the building back if fire, flood, collapse, or another insured peril destroyed it.

That difference is easy to ignore until there's a claim. Then it becomes expensive.

A stark UK example came from the 2019 fire at Nottingham's Grade II-listed Lenton Laundry building. A professional recalculation by BCIS found the true reinstatement figure was £6.17 billion rather than £5 billion, leaving the property underinsured by £1.17 billion according to this report on the Nottingham Lenton Laundry case. The scale is unusual, but the lesson is not. Outdated reinstatement figures create real financial shortfalls.

Owners often assume a valuation done for sale, probate, tax, or lending will answer the insurance question as well. It won't. If you need the open market figure, that's a different exercise entirely, and a RICS Red Book valuation serves a different purpose from an insurance reinstatement assessment.

Most owners first meet the phrase cost of reinstatement when they're buying cover, renewing a policy, or being asked awkward questions by a broker after a survey has flagged something unusual. They often assume the figure should sit somewhere near the sale price. In practice, that can be badly wrong.

A market value includes land and location. A house on a desirable street may command a strong price because buyers want the postcode, school catchment, transport links, or future development potential. None of that helps you rebuild after a total loss. Insurance is concerned with the building and the cost of putting it back.

For a listed building, a converted barn, or a house with specialist finishes, the reinstatement figure can be higher than the market value. For a modern house on expensive land, the reinstatement figure may be lower. That's why owners who “round it up a bit” are often still guessing.

Practical rule: If the figure wasn't produced for insurance, assume it may not be suitable for insurance.

The Nottingham Lenton Laundry fire makes the point brutally well. The building was insured for one figure, but the professional rebuild assessment came out far higher. The underinsurance gap was enormous, and the underlying issue was familiar: an outdated reinstatement figure on a building where specialist reinstatement requirements mattered.

Owners usually mix up these three questions:

| Question | Correct figure |

|---|---|

| What could I sell it for? | Market value |

| What would a lender consider it worth? | Lending valuation |

| What would it cost to rebuild after major damage? | Reinstatement cost |

That confusion is understandable because all three involve property value in ordinary conversation. In professional work, they are different instructions with different methods and different outcomes.

Insurers don't ask for a sum insured to fill space on a form. They use it to assess whether the property has been insured on a proper basis. If the figure is too low, the policyholder may not receive the full cost of reinstatement. That's where underinsurance stops being an abstract risk and becomes a cash problem for the owner.

A proper assessment is not paperwork for its own sake. It is a risk management tool. It gives the owner, broker, and insurer a defensible figure based on the building that exists, not the number someone hopes will be enough.

A lot of owners think the cost of reinstatement means bricks, timber, roofing, and labour. That's only part of it.

The easiest way to explain it is with a practical comparison. Market value tells you what the whole property is worth in the market. Reinstatement cost tells you what it takes to start again and rebuild the structure after insured damage.

Replacing a kitchen illustrates the core concept. The sale price of the house doesn't tell you what the units, worktops, strip-out, fitting, waste removal, design work, and compliance costs will be. A rebuild assessment works the same way, but across the whole building.

Here's the difference in simple terms:

| Factor | Market Value | Reinstatement Cost |

|---|---|---|

| What it measures | Sale price in the open market | Cost to rebuild after destruction |

| Includes land value | Yes | No |

| Affected by location demand | Yes | Indirectly, through build costs and logistics |

| Includes demolition and clearance | No | Yes |

| Includes professional fees | No | Yes |

| Used for insurance sum insured | No | Yes |

When a chartered surveyor assesses the cost of reinstatement, the figure usually needs to account for far more than the shell of the building.

Reinstatement cost is a project budget, not a rough estimate for materials.

Older houses and unusual buildings regularly carry hidden reinstatement complexity. Decorative detailing, non-standard roof forms, specialist joinery, stonework, heritage windows, difficult access, and constrained urban sites all alter the figure. So do outbuildings, boundary walls, retaining structures, and site-specific constraints if they form part of the insured risk.

This is why basic calculators can mislead. They may give a broad indication for a straightforward modern house, but they don't inspect the building, they don't diagnose complexity, and they don't exercise professional judgement. For anything atypical, the number can be false comfort.

If the building is standard, the broad principle is straightforward. If the building is old, altered, listed, or defective, the assessment becomes much more technical. That's where a proper survey earns its keep.

The professional method is more disciplined than many owners expect. It isn't a guess, and it isn't a recycled market valuation with a different title.

A chartered surveyor usually starts with the building itself. That means inspecting the property, identifying the construction type, noting unusual features, checking extensions and alterations, and measuring the relevant areas properly. Gross Internal Area is commonly important because cost data often depends on measured floor area.

The surveyor then considers what would need to be rebuilt. On a simple house, that may be relatively direct. On a large detached property, a converted building, or a period structure, the exercise broadens quickly. Roof form, wall thickness, internal specification, ancillary structures, access constraints, and heritage details all affect the figure.

A useful overview of that professional workflow appears in this explanation of the reinstatement cost assessment process for property insurance.

Surveyors don't price the rebuild line by line in the same way a contractor tenders a completed design. They usually apply recognised cost data as a base and then adjust for the building in front of them. In UK practice, BCIS data is central to that exercise.

That's where experience matters. Cost data is only the starting point. The surveyor still has to adjust for specification, age, complexity, region, access, external works, and the requirements of compliance.

One major complication is regulation. Post-2024 changes to UK building regulations, particularly Part L and emerging 2025 Future Homes Standard previews, mean RCAs must factor in 15-20% higher costs for low-carbon materials, enhanced insulation, and mandated features such as EV chargers or heat pumps, which can add £10k-£25k to an average semi-detached rebuild cost, as noted in this discussion of UK reinstatement cost changes and low-carbon rebuild requirements.

That doesn't mean every owner should inflate a sum insured casually. It means the assessment has to reflect the regulatory and practical basis on which a damaged building would be reinstated.

A reinstatement figure that ignores current compliance requirements can be out of date before the policy even starts.

Some practices also use specialist digital tools to organise measurement, costing assumptions, and reporting. Platforms such as Exayard construction estimating software can help structure estimate inputs, but software still needs a competent professional behind it. The judgment sits with the surveyor, not the dashboard.

A short video can help if you want a visual sense of how rebuild cost thinking differs from ordinary property value work.

What works is current measurement, current cost data, and adjustments for the actual building. What doesn't work is copying last year's sum insured, relying on a lender's valuation, or assuming a sale price covers the insurance question.

For standard stock, the process is efficient. For listed, altered, or defective buildings, it becomes a specialist exercise. That's not overkill. It's the only way to produce a figure with any real credibility.

Even when owners accept the principle, they often underestimate how quickly the number can move.

The most obvious driver is location, but not in the same way it affects market value. Build rates vary across the UK. BCIS indices show a 45% national increase in reinstatement costs from Q1 2020 to Q4 2025, with London averaging £3,200 per sqm in 2025 compared with £1,800 per sqm in the North East, according to this review of key UK reinstatement cost considerations.

That matters because owners still use broad national assumptions when the local build environment is doing something very different. A London townhouse, a rural stone cottage, and a North East semi may all have similar sale prices within their own local markets, but their rebuild profiles are not remotely interchangeable.

Other common drivers include:

The most common mistake is using a number that was never prepared for insurance. The second is failing to revisit the figure after time has passed, works have been carried out, or regulations have changed. The third is forgetting the non-build elements already discussed earlier in the article.

On site: The buildings that create the biggest insurance disputes are rarely the obvious ones. They are the altered houses and older properties where somebody relied on a figure that sounded reasonable.

Online calculators can be acceptable as a very rough starting point for a plain modern house. They are much less reliable for listed buildings, heavily extended homes, converted properties, or buildings with unusual construction. They don't inspect access, they don't pick up specialist materials, and they don't challenge bad assumptions.

A second trap is false economy. Owners sometimes lower the declared sum insured to reduce premiums. That can work until a claim exposes the gap. At that stage, the premium saving usually looks trivial compared with the uninsured loss.

The cost of reinstatement becomes clearer when you apply it to real property types rather than treating it as an abstract insurance term.

Take a straightforward modern three-bedroom semi-detached house. The surveyor's task is usually manageable because the construction is familiar, the detailing is standard, and replacements are generally available through ordinary supply chains. The assessment still needs proper measurement and a professional allowance for demolition, clearance, fees, and compliance, but the range of unknowns is narrower.

In that scenario, the market value may be heavily influenced by the area, transport links, and buyer demand. The reinstatement figure is driven more by current build costs, the building's size, and the specification in place. That's why sale price and rebuild cost often diverge.

Now compare that with a Grade II listed period property. The market may value it for character and scarcity, but the rebuild question is harder. Reinstatement may involve specialist timber sections, heritage-compatible windows, lime-based materials, decorative work, and approvals that slow the process and increase cost.

If a survey also identifies structural movement, the risk profile changes again. For example, rectifying subsidence in a typical Victorian terraced home can cost between £5,000 and £50,000, with an average of £15,000 to £25,000. That's a meaningful issue in any broader insurance and repair strategy, but the source link for that range has already been used earlier in this article, so the key point here is practical rather than repetitive: defects discovered during a survey can materially affect how an owner thinks about reinstatement risk, remedial budgeting, and insurance adequacy.

A standard house may suit a broad-brush approach better than a heritage property, but neither should be insured on guesswork. The more unusual the building, the more dangerous assumptions become.

The discipline is the same in both cases. Measure the property properly, identify the actual construction and constraints, account for all rebuild-related costs, and insure on that basis. One size does not fit all, and with older stock it rarely comes close.

Most owners wait too long to commission an assessment. They do it when an insurer asks awkward questions, after a major extension, or when a claim has already exposed a problem. That's late.

The sensible times are straightforward:

If you need a formal instruction route, Survey Merchant's insurance reinstatement service is one example of how owners can source an appropriate surveyor for this type of report.

An assessment report only helps if you use it. Send it to your broker or insurer and make sure the sum insured reflects the report, not an older figure sitting on file. Keep the date in mind. Reinstatement is not a once-and-done exercise, especially where the building is unusual or costs are moving quickly.

The reason is the average clause. The same RICS guidance notes that if a property needing £500k of cover is insured for £400k, it is insured for 80% of the correct amount. In that example, a £100k claim would only receive 80%, not the full loss amount. Underinsurance affects partial claims as well as total losses.

Don't file the report away as evidence you “dealt with insurance”. Use it to set the declared figure, review the policy wording, and revisit the number when the property changes.

It also helps during ownership decisions. If a purchase survey reveals compliance issues, ageing fabric, or services that will require specialist reinstatement in a claim scenario, you can factor that into negotiation and future holding costs. For buildings with fire protection upgrades or post-works commissioning requirements, practical handover items matter too. On refurbishment projects, documents such as professional fire alarm handover requirements can form part of the wider compliance picture that owners shouldn't leave vague.

A sound approach is simple:

That is how the cost of reinstatement moves from a misunderstood insurance term to a practical layer of asset protection.

If you need an accurate reinstatement figure for a house, flat block, commercial premises, or unusual property, Survey Merchant can connect you with a suitably qualified surveyor from its UK panel for an insurance-focused assessment.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes