Leasehold

Jul 6, 2026

How to Choose a Surveyor for Your Property Purchase

Choose a RICS-qualified, locally experienced surveyor with proper insurance and the right Level 2 or Level 3 report to avoid

When buying property in the UK, hiring the right surveyor is crucial to avoid costly surprises. A good surveyor can spot issues like damp, subsidence, or Japanese knotweed, which might not be visible during viewings. Here's a quick guide to help you choose:

A detailed survey can help you negotiate repairs, adjust your offer, or avoid risky purchases altogether. Choose wisely to protect your investment.

When selecting a surveyor, their credentials should be your first consideration. One of the most reliable indicators of expertise is membership with the Royal Institution of Chartered Surveyors (RICS). This global professional body enforces high standards across property, construction, and land management [5]. Let’s break down what these qualifications mean and why they matter.

Look for designations like MRICS (Member of RICS) or FRICS (Fellow of RICS). These titles signify chartered status, achieved through an RICS-accredited degree, practical training, and passing the Assessment of Professional Competence (APC) [5][6]. Another designation you might see is AssocRICS, which reflects an entry-level qualification. While it’s a step towards chartered status, it doesn’t yet represent the full professional recognition [5].

An FRICS title reflects exceptional achievement and extensive experience, while MRICS indicates a high level of professional competence. With over 500 RICS-accredited surveying degree courses offered at UK universities, these qualifications ensure surveyors undergo rigorous and standardised training [5].

Beyond checking qualifications, confirm that the surveyor actively maintains their professional standards through Continuing Professional Development (CPD). CPD ensures they stay informed about updates to building regulations and property legislation, which is crucial for providing accurate advice [5][6]. A surveyor who skips CPD risks falling behind on changes that could directly impact your property decisions.

Additionally, ensure the surveyor specialises in residential properties if that’s your focus. RICS offers various specialisms, and for home purchases, you’ll want someone trained specifically in the "Residential" pathway. This guarantees their expertise is tailored to homes rather than commercial properties or infrastructure, helping safeguard your investment [5].

When choosing a surveyor, their experience with your type of property and familiarity with the local area are crucial. These skills build on the accredited standards mentioned earlier, ensuring a thorough and tailored evaluation. It's worth digging into their background to confirm they understand the unique challenges of your property and the specific risks in your area.

Every property comes with its own set of quirks and potential issues. A surveyor who has experience with properties like yours will be better equipped to spot these. For instance, period homes often come with challenges like timber rot or damp, so you'll want someone who has dealt with these before. On the other hand, if you're buying a new build, look for a surveyor who specialises in snagging surveys (which typically cost between £320 and £600) to catch any construction defects [2].

A good question to ask is: "When was the last time you surveyed a property like mine?" An experienced surveyor should be able to provide specific examples. Go a step further - ask to see a sample report. Does it include clear explanations and photographs? For older homes, a Level 3 Building Survey, which can take an entire day, should provide far more detail than a quick, surface-level check [2].

But property type is only one part of the equation. A surveyor's knowledge of the local area is just as important.

A surveyor with a solid grasp of your area's characteristics can identify risks that someone from outside might overlook. Marc Shoffman highlights this point:

"It's also worth considering picking someone local who has a grasp of the prevalent risks in the area - for example, properties in several areas in London are at particular risk of subsidence due to the city's clay soil" [1].

Local experts bring an understanding of regional construction styles and environmental conditions. For example, they might be familiar with old colliery housing in the North East or know how coastal weathering affects properties by the sea [9].

You could ask: "What specific problems have you encountered with properties in this neighbourhood?" A knowledgeable surveyor might mention issues like Japanese knotweed or ground instability, which could be common in your area [1][7]. As Nick Cobb, a Chartered Surveyor, explains:

"Local surveyors have an intimate understanding of the area's regulations, environmental factors, and historical considerations" [8].

This kind of insight ensures you're not left with a generic, one-size-fits-all report from a national chain that may lack familiarity with the unique aspects of your neighbourhood [9][10]. Instead, you'll get a detailed and relevant evaluation tailored to your property and location.

Level 2 vs Level 3 Property Survey Comparison Guide UK

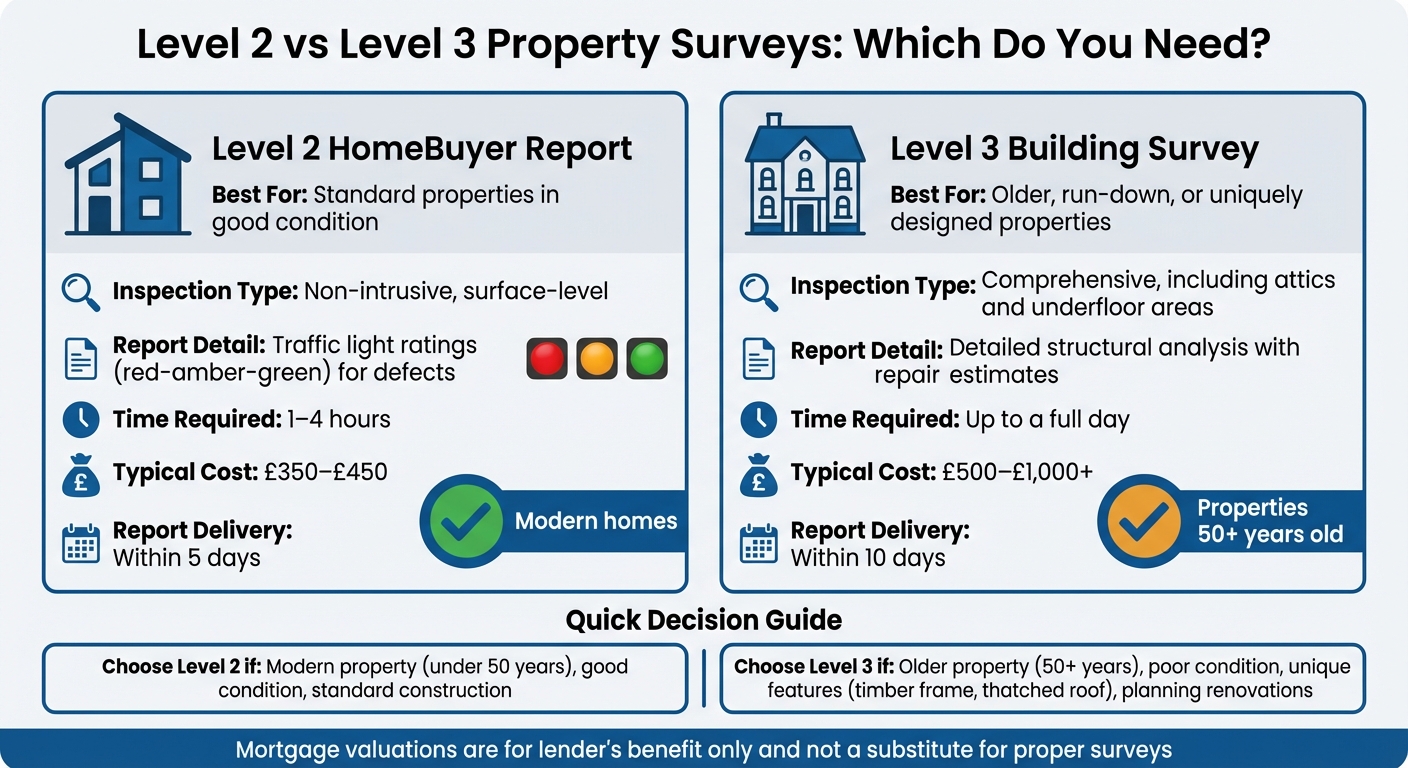

Selecting the right survey is all about matching it to your property's condition and potential risks. Building on the credentials discussed earlier, your choice should cater to your property's specific needs. Typically, the decision boils down to two key options: the Level 2 HomeBuyer Report and the Level 3 Building Survey. Each serves a unique purpose, so choosing wisely can help you avoid overlooking critical issues or paying for unnecessary details.

The Level 2 HomeBuyer Report is ideal for standard properties that are in good condition. This survey is non-intrusive, taking between 1 and 4 hours, and focuses on visible issues without delving into hidden areas [2]. It uses a straightforward 'red–amber–green' rating system to identify concerns [3]. Costs typically range from £350 to £450, and you can expect the report within 5 days [3][4]. As Savills highlights:

"The HomeBuyer Report... can pay for itself many times over by highlighting issues that might become more expensive in the future" [4].

On the other hand, the Level 3 Building Survey is more detailed and can take an entire day. It provides a thorough structural analysis, including repair recommendations and cost estimates [3]. This survey is best suited for older properties (over 50 years), those in poor condition, or buildings with unique designs - think timber-framed cottages [3]. It covers areas like attics and underfloor spaces, often including timelines and costs for repairs [3]. As Savills explains:

"A building survey gives you a complete breakdown of the structure and condition of a property, and can include projections on the time and cost needed to fix any issues" [4].

The cost for a Level 3 survey starts at £500 and can exceed £1,000 for more complex properties, with reports taking up to 10 days to complete [3][4]. While more expensive, the detailed insights can strengthen your negotiating position, allowing you to request price reductions or have repairs addressed before finalising the purchase [3][4].

| Feature | Level 2 HomeBuyer Report | Level 3 Building Survey |

|---|---|---|

| Best For | Standard properties in good condition | Older, run-down, or uniquely designed properties |

| Inspection Type | Non-intrusive, surface-level | Comprehensive, including attics and underfloor areas |

| Report Detail | Traffic light ratings for defects | Detailed structural analysis with repair estimates |

| Time Required | 1–4 hours | Up to a full day |

| Typical Cost | £350–£450 | £500–£1,000+ |

| Report Delivery | Within 5 days | Within 10 days |

It’s worth noting that a mortgage valuation is designed solely for the lender’s benefit and often doesn’t include a physical inspection, making it unsuitable as a substitute for a detailed survey [3].

Surveyors also offer additional services tailored to specific needs. For instance, snagging surveys - costing between £300 and £600 - are great for new builds. These surveys identify both cosmetic and structural issues before completion, even if the property comes with a 10-year guarantee [2][3].

If you're planning an extension or a loft conversion, you'll need a party wall agreement to avoid disputes with neighbours [2]. For other situations, like probate, divorce settlements, or Help to Buy equity loan repayments, valuation surveys provide independent market assessments [2][11].

When structural concerns arise - such as subsidence or sagging roofs - a structural engineer's report may be required. These reports include detailed calculations and solutions [2][11]. Surveyors can also arrange specialist reports to address specific risks, such as asbestos, drainage, electrical systems, flood hazards, or Japanese knotweed. These targeted inspections are especially useful when standard surveys flag potential issues that need further investigation.

Before hiring a surveyor, it’s crucial to check their credentials and ensure they have Professional Indemnity Insurance (PII). This not only protects you financially if something goes wrong but also gives you insight into their reliability through real client experiences.

Professional Indemnity Insurance safeguards both you and the surveyor if negligence occurs. It covers the costs of defending against claims and compensates clients for financial losses caused by mistakes, poor advice, or overlooked issues. For instance, if your surveyor fails to detect a major problem like subsidence - an issue that can be expensive to rectify - the insurance ensures you aren’t left footing the bill [12][1].

This type of insurance also covers legal defence costs, even if a claim turns out to be unfounded. However, most policies operate on a "claims-made" basis, meaning they only cover claims made while the policy is active. This makes it essential for surveyors to maintain continuous and up-to-date coverage.

To confirm your surveyor has adequate insurance, check whether they are regulated by a recognised body like the Royal Institution of Chartered Surveyors (RICS) or are members of the Residential Property Surveyors Association (RPSA). Look out for designations such as MRICS or FRICS, and make sure they are part of a complaints scheme like The Property Ombudsman or the Property Redress Scheme.

Once you’ve verified their insurance, take time to assess the surveyor’s reputation. Client reviews are a great way to understand how they perform in real-world situations. Focus on aspects like communication, punctuality, and the clarity of their reports. Ask yourself: Were they responsive to queries? Did they deliver the report on time? Was the report detailed yet easy to understand?

You can find genuine reviews through personal recommendations, online property forums, or platforms like Reallymoving and HomeOwners Alliance. Both the RICS and RPSA websites also list professionals, often with client feedback included. For extra assurance, request a sample report to see if it’s written in clear language, includes photographs, and highlights key concerns.

Jonathan Rolande from the National Association of Property Buyers advises:

"A good surveyor will reassure you, or highlight things you may not have seen, such as dampness, water corrosion, roof issues, woodworm or asbestos."

Pay close attention to reviews that mention local expertise. Surveyors familiar with your area are more likely to spot region-specific risks, like clay-soil subsidence or invasive plants.

After verifying insurance and reading reviews, it's time to make your final choice. This step ties together all the research and comparisons you've done, helping you pick a surveyor who suits your property's needs. At this stage, you'll weigh up costs, confirm timelines, and ensure the surveyor's expertise matches your specific requirements.

Start by gathering detailed quotes from at least three surveyors. This will help you compare their services and pricing side by side. Survey costs can vary significantly, with basic assessments starting around £300 and more complex property surveys exceeding £1,500. For a Level 1 or Level 2 survey, expect to pay between £500 and £1,000, while Level 3 structural surveys typically range from £700 to £1,500 [1][2].

When reviewing quotes, make sure they outline exactly what's included. Look for details like photographic evidence, investigations into specific concerns, and valuation information. Be mindful of any additional fees, such as travel costs or charges for revisits. It's also worth steering clear of surveyors recommended by estate agents, as these might come with extra referral fees [2].

Pin down two key dates: when the physical inspection will take place and when you'll receive the final report. Request these dates in DD/MM/YYYY format for clarity, and ensure they align with your solicitor's timeline. Delays in receiving the report can hold up your property transaction, so it's crucial that the surveyor's availability fits within any deadlines set by your solicitor or mortgage lender.

Once you've compared costs and confirmed availability, focus on whether the surveyor's experience suits your property's unique characteristics. As mentioned earlier, a surveyor familiar with local issues is essential for spotting potential hidden problems. If you're purchasing an older, listed, or unusual property - like one with a thatched roof or timber frame - ask specifically about their experience with similar buildings. Enquire about common issues they've encountered in such properties [2]. Angela Kerr, Director at HomeOwners Alliance, advises:

"Always get quotes from a few firms and compare" [2].

Request a sample report to check for clarity and the inclusion of photographs. This ensures you'll understand the findings when your own report arrives. Keep in mind that 60% of consumers value regulated qualifications and membership in professional bodies as the most important qualities in a surveyor [13]. Before making your final decision, verify that they hold MRICS or FRICS credentials for added peace of mind.

By following the outlined steps, you can find a surveyor who aligns with your property's specific needs. It's crucial to select a professional with the right qualifications, such as MRICS or FRICS credentials from RICS, or membership with the RPSA. These credentials ensure adherence to strict professional standards and provide access to redress schemes if needed. Early identification of potential issues can save you from costly repairs down the line, and a surveyor's local expertise can be invaluable in spotting region-specific risks.

When choosing a surveyor, prioritise those with local knowledge and experience relevant to your type of property. The survey level should also match your property's age and condition: a Level 2 survey is generally suitable for modern homes, while a Level 3 structural survey is recommended for older properties or those with unique features. As previously mentioned, credentials like MRICS or FRICS, combined with a solid track record, are key factors to consider.

Additionally, as covered in the quotes and availability section, it’s essential to compare quotes, reviews, and sample reports. This ensures you receive detailed feedback tailored to your property. As Rob Houghton, Chief Executive of Reallymoving, aptly puts it:

"There's no point getting an inadequate survey which isn't right for your property" [1].

Choosing the right surveyor not only protects your investment but also provides peace of mind. A thorough survey equips you with the insights needed to address risks, negotiate repairs, adjust your offer, or, if necessary, step away from a property that may present significant challenges.

When choosing a surveyor, it’s essential to ensure they are RICS-regulated and hold chartered status, which you’ll recognise by the letters MRICS or FRICS after their name. This designation ensures they adhere to strict professional standards and participate in ongoing training. You can verify their credentials using the RICS directory and confirm that their firm is approved by the institution.

Experience plays a key role as well. Seek out a surveyor with a solid track record of working on properties similar to yours. Whether it’s a period property, a new-build, or a unique construction type, their expertise should align with your needs. Local knowledge is another crucial factor, as it allows them to identify potential regional issues such as subsidence or damp. They should also be able to advise you on the most suitable survey level - whether that’s Level 1, 2, or 3 - based on the property’s age and condition.

Lastly, take the time to check their reputation. Look for testimonials or case studies that highlight their ability to provide detailed reports and assist clients with matters like repairs or renegotiations. By thoroughly evaluating their qualifications, experience, and reliability, you can make a confident and informed decision.

The decision between a Level 2 HomeBuyer Report and a Level 3 Building Survey largely hinges on the property’s age, condition, and complexity, as well as the level of detail you need from the inspection.

A Level 2 HomeBuyer Report works well for modern properties in good shape, such as houses, flats, or bungalows built with standard materials. It offers a straightforward summary of major defects, uses a traffic-light system to rate key elements, and can include an optional valuation. This option is budget-friendly and suits properties constructed after the 1990s.

On the other hand, a Level 3 Building Survey provides a much more comprehensive assessment, making it ideal for older, larger, or modified properties. This includes period homes, listed buildings, or properties showing signs of wear, damp, or structural concerns. The survey covers all accessible areas, uncovering hidden problems like rot or hazardous materials, and equips you with the information to plan repairs or negotiate costs effectively.

In general, newer, well-maintained properties are usually fine with a Level 2 report, while older or more complex homes benefit from the detailed insights of a Level 3 survey. Think carefully about the property’s condition and what you need from the inspection before making your choice.

Choosing a surveyor with local expertise can make a world of difference when assessing a property. Their understanding of the area’s specific characteristics - like typical construction methods, local planning rules, and regional risks such as ground movement - enables them to evaluate a property’s condition with greater accuracy.

Beyond the inspection itself, a surveyor familiar with the area can offer personalised advice on issues like hidden defects, estimated repair costs, and even the property’s potential resale value. This kind of insight doesn’t just help you make smarter decisions - it also gives you an edge when negotiating a fair price, helping to safeguard your financial investment.