Valuation

Jul 16, 2026

Capital gains tax property valuation: UK guide 2026

Discover how to navigate capital gains tax property valuation in the UK. Ensure accurate valuations and maximize your tax strategies for 2026.

Capital gains tax property valuation is the process of establishing market value at a specific statutory date to calculate the taxable gain on a UK property disposal. HMRC does not simply subtract what you paid from what you received. The figure that matters is the market value at the date the law prescribes, whether that is your original acquisition date, a fixed rebasing date, or the date of disposal. Get that figure wrong and your entire capital gains tax calculation is built on a flawed foundation. This guide explains the statutory framework, RICS valuation standards, and the practical steps UK property owners and investors need to take to get it right.

The statutory valuation date is the single most consequential variable in any CGT calculation. HMRC does not always accept your purchase price as the starting point for calculating a gain.

For residential property owned before 5 April 2015, HMRC requires market value at that date as the base cost rather than the original acquisition price. This rebasing rule means a landlord who bought a buy-to-let in 2003 for £120,000 and sold it in 2025 for £380,000 does not automatically calculate a gain of £260,000. The gain is measured from the 5 April 2015 market value instead, which could be substantially higher than the 2003 purchase price and therefore reduces the taxable gain considerably.

For non-residential property and indirect disposals such as shares in property-rich companies, the equivalent rebasing date is 5 April 2019. This distinction matters enormously for commercial investors who may incorrectly apply the residential rebasing date to their portfolio.

The practical steps for applying statutory valuation rules correctly are:

Pro Tip: Retrospective valuations for a date a decade or more in the past are entirely valid under RICS standards. A qualified surveyor uses comparable sales evidence from around the statutory date to form a credible opinion. Commission this before you complete a disposal, not after.

A number, however confidently stated, is not a valuation unless it meets specific professional criteria. RICS defines a valuation as an opinion of value on a stated basis at a specified date, supported by inspection and comparable analysis in line with Red Book Global Standards. This definition has direct consequences for CGT compliance.

The RICS Red Book Global Standards require a compliant valuation report to clearly state:

“A valuation report that clearly documents its purpose, basis, and methodology is far more likely to be accepted by HMRC without challenge than a figure produced informally or without a stated basis.” RICS Red Book Global Standards guidance on scope and purpose

The three primary valuation approaches a RICS surveyor may apply are the market approach, the income approach, and the cost approach. RICS explains that the market approach, which relies on comparable sales evidence, is the most commonly used method for CGT property valuations. The income approach, which capitalises rental income at an appropriate yield, is typically applied to investment properties where comparable sales are limited. The cost approach is reserved for specialist or unusual properties where neither market nor income evidence is readily available.

Understanding RICS Red Book valuations in detail helps you ask the right questions when commissioning a report. A surveyor who cannot clearly articulate which approach they are using and why is not providing a defensible valuation.

Commissioning a valuation for CGT purposes is not the same as commissioning a mortgage valuation or a pre-purchase survey. The scope, purpose, and required output are different, and you need to brief your surveyor accordingly.

The key steps to follow are:

Incorrectly applying statutory valuation dates in CGT property valuations can lead to disputes that are difficult to rectify after the fact. Retrospective adjustments to valuation figures are technically possible but practically very hard to defend without contemporaneous evidence.

Pro Tip: If you are selling a property that you have owned since before 2015, commission the rebasing valuation at the same time as you instruct your solicitor. Waiting until after completion makes the retrospective exercise harder and more expensive.

For further guidance on navigating property valuations in the UK, Surveymerchant provides detailed resources covering the full scope of what a compliant report should contain.

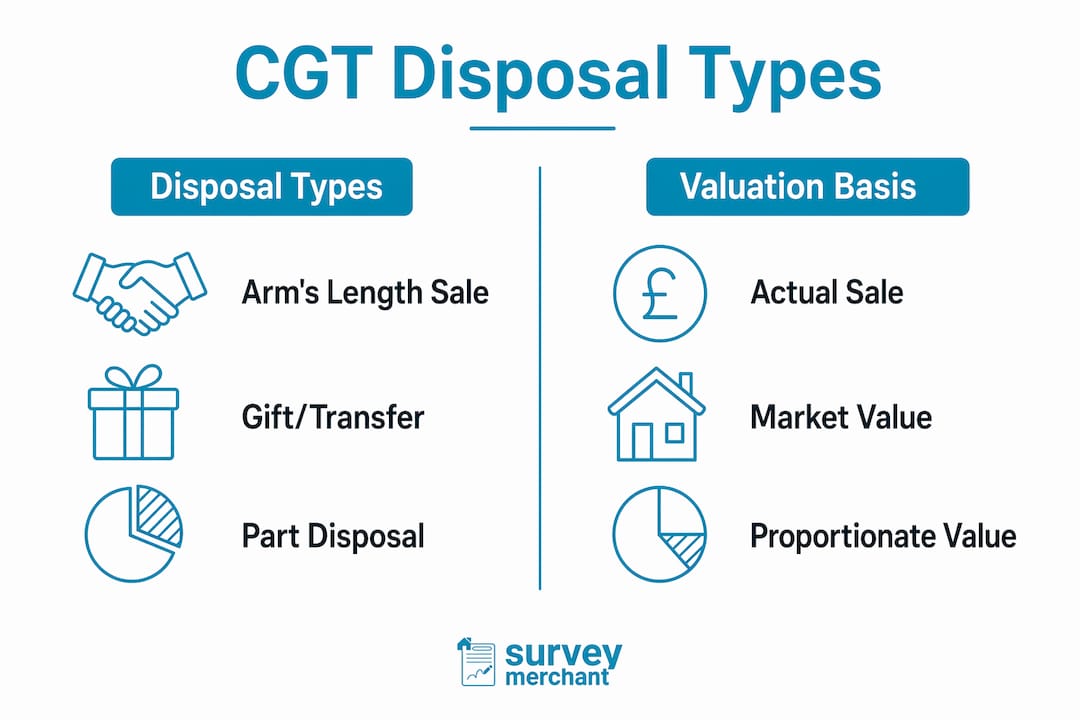

Not every disposal involves a straightforward sale at arm’s length. Gifts, transfers between connected persons, and partnership disposals each trigger different valuation rules under HMRC guidance.

| Disposal type | Valuation basis required | Notes |

|---|---|---|

| Arm’s length sale | Actual sale proceeds | Market value check still advisable if parties are connected |

| Gift or transfer below market value | Market value at disposal date | HMRC treats disposal as occurring at market value regardless of consideration paid |

| Hold-over Relief claim | Estimated market value acceptable | Estimates are not binding and may be challenged by HMRC |

| Partnership disposal | Market value or balance sheet value | HS288 details specific rules depending on the nature of the disposal |

| Connected persons transfer | Market value at disposal date | Applies to transfers between spouses (outside marriage breakdown rules), relatives, and controlled companies |

Transfers at less than market value consistently catch property owners off guard. A parent transferring a buy-to-let to an adult child for £1 does not avoid CGT. HMRC treats that disposal as occurring at full market value on the date of transfer, and the parent is liable for CGT on the gain from their base cost to that market value figure. Valuation evidence is therefore just as important in gifting scenarios as in commercial sales.

One nuance worth understanding involves Hold-over Relief. HMRC clarifies that where Hold-over Relief applies, estimated market values in the tax return do not need to be formal RICS valuations and are not binding in the same way. However, those estimates can still be challenged, and a formal valuation provides considerably stronger protection if HMRC opens an enquiry later.

Accurate capital gains tax property valuation requires identifying the correct statutory date, applying RICS-compliant methodology, and retaining formal documentation before completing any disposal.

| Point | Details |

|---|---|

| Statutory rebasing dates | Use 5 April 2015 for residential property and 5 April 2019 for non-residential or indirect disposals as the base cost. |

| Market value overrides sale price | Gifts and connected party transfers are treated by HMRC as disposals at full market value, regardless of actual consideration. |

| RICS Red Book compliance | A formal valuation report stating purpose, basis, date, and comparables is far more defensible against HMRC challenge than an informal estimate. |

| Commission valuations early | Retrospective valuations become harder to evidence after completion. Instruct a RICS surveyor at the same time as your solicitor. |

| Hold-over Relief estimates | Formal valuations are not always mandatory in Hold-over Relief cases, but estimates remain open to HMRC challenge without supporting evidence. |

Having worked alongside UK property owners and investors for years, the pattern I see most often is not ignorance of the rules. It is timing. People understand, in broad terms, that CGT applies to property gains. What they consistently underestimate is how much the valuation figure itself determines the tax outcome, and how difficult it becomes to establish that figure credibly after the fact.

The 5 April 2015 rebasing date is a perfect example. A landlord who purchased a property in 2001 and sells today has a potential base cost that is far higher than their original purchase price, which could reduce their CGT liability substantially. But if they have never commissioned a 2015 market value opinion, they are either overpaying tax or relying on an unsupported estimate that HMRC can challenge. Neither outcome is acceptable when a single RICS valuation report resolves the problem entirely.

The other misunderstanding I encounter regularly concerns gifts and family transfers. People focus on the legal paperwork and assume that because no money changed hands, there is no tax event. Transfers below market value trigger a deemed disposal at market value under HMRC rules, and the valuation evidence needed to quantify that liability is exactly the same as for a commercial sale.

My practical recommendation is to treat a CGT valuation as a professional instruction with a clear brief, not a conversation with an estate agent. The cost of a RICS-compliant report is modest relative to the tax at stake and the cost of an HMRC dispute. For most property owners, it is the single most cost-effective step in managing their real estate valuation obligations for tax purposes.

— Surveymerchant

Surveymerchant connects UK property owners and investors with qualified RICS surveyors who specialise in tax-related property valuations. Whether you need a retrospective 5 April 2015 market value for a residential property, a current market value for a disposal, or a formal report for a gift or connected party transfer, Surveymerchant’s panel of experts delivers reports that meet RICS Red Book standards and stand up to HMRC scrutiny. Every instruction is matched to a surveyor with relevant experience in RICS valuation services for CGT and tax compliance purposes. Commission your valuation with confidence and protect your position before you complete.

The rebasing date for residential property is 5 April 2015. HMRC uses the market value at that date as the base cost for properties owned before then, rather than the original acquisition price.

Not always. HMRC accepts considered estimates in some cases, particularly where Hold-over Relief applies. However, a formal RICS Red Book valuation report provides significantly stronger protection against challenge and is advisable for any material gain.

HMRC treats a gift as a disposal at full market value on the date of transfer, regardless of the actual consideration paid. The donor is liable for CGT on the gain from their base cost to that market value figure.

The market approach, which uses comparable sales evidence, is the most commonly applied method for CGT property valuations. The income approach is used for investment properties and the cost approach for specialist assets where comparable evidence is limited.

Yes. A RICS surveyor can provide a retrospective market value opinion for a past date, including 5 April 2015 or 5 April 2019, using comparable sales evidence from around that period. This is a standard and accepted practice for CGT compliance purposes.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes