Building Surveying

Jul 22, 2026

Why get a pre-purchase survey: protect your property investment

Discover why get a pre-purchase survey is crucial for protecting your property investment. Learn how it offers real insights before you buy.

Most buyers assume that because their mortgage lender arranges a valuation, they have a clear picture of the property’s condition. They do not. Mortgage valuations are limited, lender-focused checks that say almost nothing about whether the building is actually sound. A pre-purchase survey, arranged by you and carried out independently, gives you the real picture before you exchange contracts and commit to one of the largest financial decisions of your life. This article explains exactly what surveys cover, why they matter, and how to use the findings to protect yourself.

| Point | Details |

|---|---|

| Mortgage valuation is not enough | A lender’s check is not a full inspection and cannot replace a survey for buyers. |

| Surveys reveal hidden risks | Pre-purchase surveys uncover costly defects and safety concerns missed in basic valuations. |

| Protect your investment | A survey helps you negotiate, plan repairs, and avoid buyer’s remorse. |

| Real savings over time | Spending on a survey now can prevent thousands of pounds in future losses. |

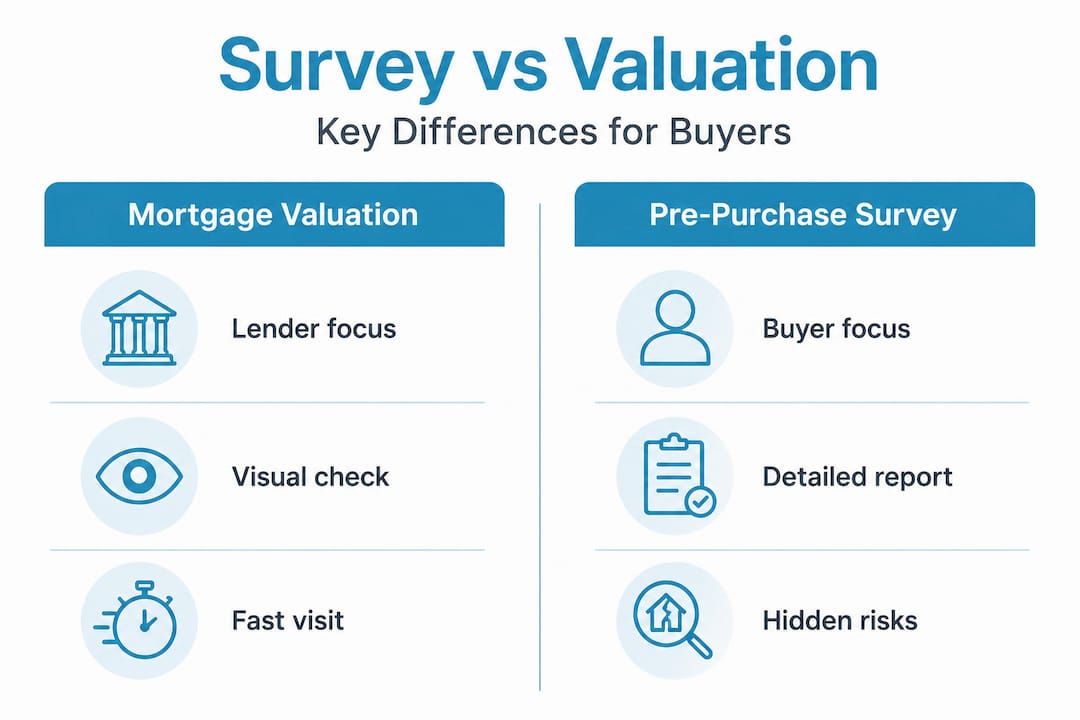

A pre-purchase survey is an independent inspection of a property carried out by a qualified surveyor on behalf of the buyer. It is not the same as a mortgage valuation, and understanding this distinction is absolutely critical before you proceed with any purchase.

When your lender sends a valuer to a property, their job is narrow: confirm whether the property is worth the amount you want to borrow. As mortgage valuations make clear, these are for lending security and include only a limited inspection. The valuer is not checking for your benefit. They will not climb into the loft, test the electrics, or prod around beneath suspended timber floors. Their report goes to the lender, not to you, and it contains only what the lender needs to know.

A pre-purchase survey, by contrast, is entirely in your corner. In the UK, surveys typically fall into three levels, each offering a progressively deeper inspection:

Understanding which level you need is part of the process. For older or structurally complex properties, a property condition survey guide can help you match the right survey type to your specific property.

Typical areas a survey covers include:

| Area inspected | Covered in mortgage valuation | Covered in Level 2 survey | Covered in Level 3 survey |

|---|---|---|---|

| Roof structure | Rarely | Yes | Yes, in detail |

| Damp and timber | No | Yes | Yes, in detail |

| Sub-floor voids | No | Sometimes | Yes |

| Electrics and plumbing | No | Visual only | Visual only |

| Market valuation | Yes | Sometimes | Optional add-on |

| Written advice and recommendations | No | Yes | Yes, extensive |

The scope difference between a valuation and a survey is not marginal. It is fundamental.

Knowing the basics, you may be wondering what exact advantages a survey brings to your purchase decision. The answer goes well beyond ticking a due-diligence box.

Find costly defects before you commit. Surveys routinely uncover problems that are not visible during a casual viewing. Damp patches hidden behind freshly painted walls, failing roof timbers obscured by modern lining boards, or subsidence cracking masked by recent cosmetic work are all examples. Once you have exchanged contracts, remedying these problems becomes your financial responsibility entirely.

Use findings to negotiate the price. If your surveyor flags significant defects, you have documented, professional evidence to go back to the seller and request a price reduction or ask them to carry out repairs before completion. This is one of the most powerful practical uses of survey findings. Buyers who skip surveys lose this leverage entirely.

Walk away without losing your investment. Discovering a severe problem after exchange can cost you thousands in penalties. Finding it before exchange means you can withdraw with minimal financial loss.

Plan your renovation budget accurately. Surveys do not just flag problems; they help you quantify them. Knowing that a roof needs replacing in the next five years, or that the central heating system is near the end of its life, means you can budget realistically rather than be blindsided after moving in.

Avoid buyer’s remorse and legal complications. Properties with undisclosed defects can generate disputes that drag on for years. A buyer’s survey provides an independent assessment of the property’s condition and risks before you commit, which means you make your decision with open eyes.

“The cost of a survey is almost always a fraction of the cost of the problems it can uncover. Buyers who skip surveys in the hope of saving a few hundred pounds regularly face repair bills running into tens of thousands.”

You might be surprised how often survey findings alter the final agreed price. Reviewing property survey problems shows just how frequently issues like damp, drainage failures, and roof defects appear in otherwise attractive-looking properties. Real HomeBuyer survey examples illustrate how surveyors communicate these findings in practice, giving you a clearer sense of what to expect.

Pro Tip: When you receive your survey report, do not just look at the summary ratings. Read the body of the report carefully, particularly sections rated amber (requiring attention) rather than just red (urgent). Amber issues can quietly become red ones if left unaddressed, and they carry real weight in a renegotiation conversation with the seller.

To make this clearer, here is how a pre-purchase survey and a standard valuation differ side by side.

The valuation exists to protect the lender. Full stop. If you are borrowing £300,000 against a property, your lender needs confidence that the property is worth at least that much if they ever need to sell it to recover their funds. That is precisely what the valuation establishes. As the guidance on mortgage valuations makes clear, they are for lending security and not a full inspection for the buyer.

A valuation typically takes between twenty and forty-five minutes on site. The valuer checks the general condition at a high level, confirms the property type and approximate size, and notes anything so obviously wrong that it would affect marketability. They are not obliged to inspect inside roof voids, lift inspection hatches, or comment on the condition of the drains. They will almost certainly not report on decorative condition, minor cracks, or the age of the boiler unless these clearly affect value.

| Feature | Mortgage valuation | Level 2 HomeBuyer Report | Level 3 Building Survey |

|---|---|---|---|

| Who commissions it | Lender | Buyer | Buyer |

| Who benefits | Lender | Buyer | Buyer |

| Time on site | 20 to 45 minutes | 2 to 3 hours | 4 to 8+ hours |

| Roof void inspection | Rarely | Where accessible | Yes |

| Sub-floor inspection | No | Sometimes | Yes |

| Damp and timber checks | No | Yes | Yes, in depth |

| Electrical/plumbing | No | Visual only | Visual only |

| Repair recommendations | No | Yes | Yes, detailed |

| Market valuation | Yes | Sometimes | Optional |

| Suitable for old/complex properties | N/A | Sometimes | Yes |

For properties built before 1950, those with extensions, listed buildings, or any home showing signs of movement or water ingress, a Level 3 Building Survey is not a luxury. Level 2 Building Survey insights explain when a HomeBuyer Report is sufficient and when upgrading to a Level 3 is the wiser choice. The table above makes it plain that a valuation and a survey are performing entirely different functions. One tells the bank the property is worth lending against. The other tells you whether it is worth buying.

Once you receive your survey report, it is important to know the steps to take next. A survey report sitting unread in your email inbox does nothing to protect you.

Read the full report, not just the ratings. Condition ratings (typically numbered 1 to 3 or colour coded) are a useful at-a-glance guide, but the narrative sections contain the detail. Your surveyor explains what they found, what it means, and what you should do about it. Read this carefully, ideally more than once.

Contact your surveyor directly with questions. A good surveyor will speak to you after issuing the report. If something is unclear, particularly around the severity of a defect or the likely cost of repair, pick up the phone. Surveyors are not just report writers; they are advisers. Getting clarity on what is urgent versus what is routine maintenance is enormously helpful in setting your priorities.

Use the findings as a negotiating tool. If the report flags significant issues, collate them and approach the seller formally through your solicitor or estate agent. Request either a price reduction that reflects the cost of works or ask the seller to remedy specific defects before completion. This is where an independent, documented professional report becomes commercially powerful.

Plan for the issues that are not urgent. Even minor issues flagged in a survey represent future expenditure. Use the report to build a maintenance schedule and budget for the first five years of ownership. Knowing the flat roof above a rear extension will need attention within three years, for example, allows you to save accordingly rather than face an emergency spend.

Pro Tip: If your survey flags a major structural problem such as active subsidence, significant roof failure, or extensive hidden damp, consider commissioning a specialist report before deciding whether to proceed. A building defects revealed in surveys breakdown will help you understand what level of specialist input each type of defect requires. You can also take early practical steps before the inspection itself by preparing for a property survey, which helps ensure the surveyor has access to all relevant areas and produces the most complete report possible.

A buyer’s survey provides an independent assessment of the property’s condition and risks before you commit, and using that assessment actively rather than filing it away is what separates buyers who make informed decisions from those who end up with expensive regrets.

With practical steps in hand, here is the overlooked reality most buyers miss when it comes to pre-purchase surveys.

The most common mistake is treating a survey as optional paperwork rather than a genuine risk-mitigation tool. Buyers who have stretched their budget to secure a property often look at survey costs and see an inconvenient extra expense. This is entirely the wrong way to frame it.

Think about what you are actually buying. In most cases, it is a building that may be decades or even over a century old, constructed with materials and techniques that vary enormously in quality and durability. The seller is motivated to present it in its best light. The estate agent’s job is to facilitate a sale. Nobody in that transaction is paid to tell you what is wrong with the building except your surveyor.

Mortgage valuations do not include key home checks and can miss significant problems that only a buyer’s survey will reveal. Surveyors have seen buyers skip surveys on Victorian terraces with undetected active damp courses, only to face replastering and tanking costs exceeding £15,000 within their first year of ownership. Surveyors have seen flat roof extensions passed by valuers that required complete replacement months after completion. These are not rare edge cases. They happen regularly.

There is also a psychological element that is rarely discussed. Buyers who commission thorough surveys consistently report feeling more settled in their purchase, even when the survey flags some issues. Knowing exactly what you are taking on and having a plan for it is far less stressful than wondering what might be lurking beneath the surface after you have moved in.

The buyers who genuinely regret commissioning a survey are extremely rare. The buyers who regret not commissioning one are not. For in-depth survey guidance that covers specific survey types and scenarios, there is a wealth of practical information to help you make the right choice for your property type and circumstances.

A survey is not a nice-to-have. It is one of the very few genuinely independent pieces of professional advice available to you during a property purchase, and treating it as such is one of the smartest financial decisions you can make.

Armed with facts and real-world insight, you can confidently move forward and secure your investment with the right professional support behind you.

At Survey Merchant, we connect buyers across the UK with qualified, experienced surveyors matched to their specific property type and location. Whether you need a detailed Level 3 Building Survey for an older or complex home, a specialist commercial property survey for a business premises purchase, or a reliable RICS valuation for financial or legal purposes, our panel of professionals is ready to help. We prioritise impartiality and quality so that you get the clearest, most accurate picture of your property before you commit. Take the next step with confidence.

Pre-purchase surveys are not legally required, but they are strongly recommended to avoid costly surprises after completion and to make a fully informed purchase decision.

No. A mortgage valuation is carried out for the lender’s security and includes only a limited inspection, meaning significant property defects can go entirely undetected.

A survey can uncover damp penetration, structural movement, failing roof timbers, subsidence, outdated wiring, plumbing problems, and serious timber defects such as rot or woodworm.

Yes. Documented defects from a professional survey give buyers strong, evidence-based grounds to renegotiate the asking price or request that the seller completes repairs before exchange.

Costs depend on survey level and property size. A Level 2 HomeBuyer Report commonly ranges from £400 to £900, while a Level 3 Building Survey for a larger or older property can run from £600 to well over £1,500.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes