Leasehold

Jul 16, 2026

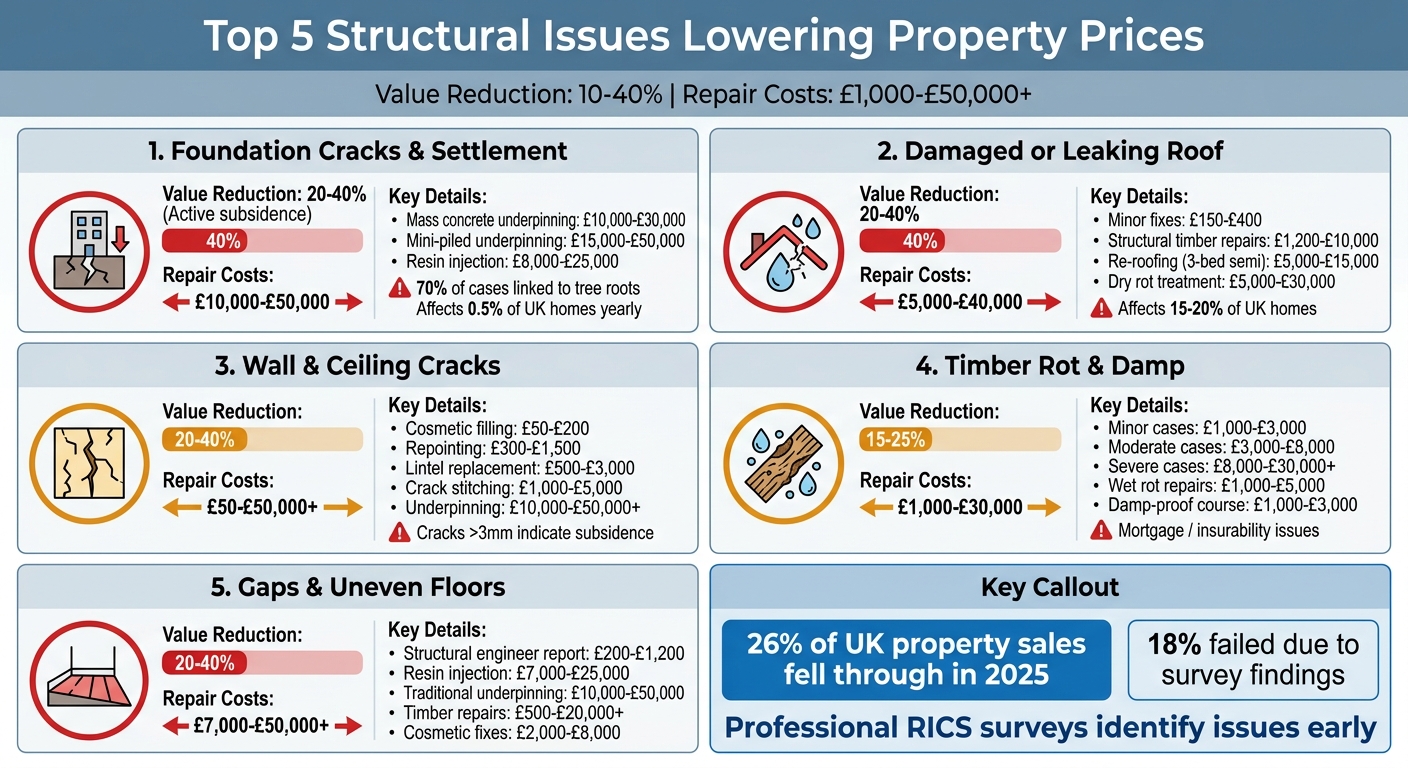

Top 5 Structural Issues Lowering Property Prices

Foundation cracks, roof leaks, wall fractures, timber rot and uneven floors can cut UK property values 10–40% and block mortgages.

Structural issues can drastically reduce property prices and complicate sales. Common problems include foundation cracks, roof damage, wall cracks, timber rot, and uneven floors. These defects can slash market value by 10–40%, make properties unmortgageable, and deter buyers. Repair costs often range from thousands to tens of thousands of pounds.

Key takeaways:

Professional surveys are vital for identifying and addressing these issues before buying or selling. Services like RICS Level 3 Building Surveys provide detailed assessments to help buyers and sellers make informed decisions.

5 Structural Issues That Lower UK Property Prices: Costs and Value Impact

Foundation cracks and settlement can seriously weaken a building's structure. Ground movement may lead to bowed walls, roof spread, and in extreme cases, even total collapse [4][5]. While settlement refers to the natural stabilisation of ground over 2–5 years, subsidence involves ongoing ground movement that demands urgent attention [5].

Common warning signs include diagonal cracks wider than 3mm (about the thickness of a £1 coin) [5]. You might also notice doors sticking, gaps forming between walls and ceilings, or widespread cracking [5][7]. Around 70% of subsidence cases are linked to tree roots, especially in homes built on clay soils that shrink during dry weather [4]. Given the shrink-swell nature of many UK soils, seasonal foundation movement is a widespread issue [8].

Fixing foundation problems can be one of the priciest challenges for homeowners. For semi-detached houses, mass concrete underpinning typically costs £10,000–£30,000, while mini-piled underpinning can range from £15,000 to £50,000 [5]. Resin injection stabilisation, a less invasive option, comes in at £8,000–£25,000 [5]. Before repairs even begin, initial costs like a structural engineer's report (£800–£2,000) and 12–18 months of crack monitoring (£500–£1,500) must be factored in. Tree management or removal can add another £500–£5,000 [5].

The financial hit from foundation issues is significant. Active subsidence can reduce a property's value by 20–40%, while even repaired issues often result in offers 10–25% lower than expected [5][1]. With roughly 0.5% of UK homes affected by subsidence yearly, most mainstream lenders refuse mortgages on properties with unresolved movement [5][8][1]. However, properly repaired subsidence - backed by a Certificate of Structural Adequacy and 10–25 years of insurance guarantees - can help recover 8–15% of the lost property value [6][5].

Foundation problems are a major concern for both buyers and lenders. In England and Wales, sellers are legally required to disclose any history of subsidence, heave, or landslip on the TA6 Property Information Form. Failing to do so could result in misrepresentation claims [8]. High repair costs, insurance complications, and fears of future movement often deter buyers and make achieving full market value difficult. To reassure potential buyers and lenders, sellers should gather all relevant documentation, such as monitoring reports and structural adequacy certificates [1][8]. These challenges highlight how structural issues, particularly in foundations, can ripple through the property market.

A leaking roof can cause serious structural issues, including roof spread, timber decay, and masonry saturation [5]. Roof spread happens when excessive weight or failing tie beams push the external walls outward, potentially leading to wall separation and even collapse [5]. Persistent leaks also lead to timber decay in vital areas like rafters and purlins, creating conditions for dry and wet rot. Additionally, defective flashings allow water to seep into masonry, causing frost damage and weakening load-bearing walls [5].

Surveyors look for early signs of roof neglect, such as daylight visible through tiles, water stains on timbers, and sagging purlins. Other red flags include damp insulation, damaged ceilings, and ponding water on flat roofs. These issues affect about 15–20% of homes in the UK [5]. Damp insulation and damaged ceilings can collapse under the weight of excess moisture, while wet conditions attract wood-boring insects like woodworm. Flat roofs are particularly at risk due to ponding water and deteriorating felt, which can lead to widespread leaks in the rooms below.

Repair costs vary widely depending on the severity of the damage:

"If roof repair costs over a rolling five-year period exceed 30 to 40 per cent of a full roof replacement cost, roof replacement is better value."

– Andrew, Lead Roofer, Bernard Andrews Roofing [9]

These expenses can significantly influence a property's appeal and financing options.

Roof issues have a direct impact on property value. Active structural problems can lower a property's worth by as much as 20–40% [5]. Mortgage lenders often see roof defects as major risks to both habitability and insurability. This can result in retentions, where lenders withhold funds equivalent to repair costs, or even outright refusal to approve loans until repairs are completed. Even something as simple as blocked gutters can reduce a property’s value by £200–£500. To address these concerns, sellers are advised to obtain specialist roof reports and repair estimates. Experts, such as those available through Survey Merchant, can provide impartial and detailed assessments.

Cracks in walls and ceilings are a common concern for homeowners in the UK, often raising red flags about potential structural issues. While some cracks are purely cosmetic, others can signal more serious problems, such as structural movement. Understanding the difference between these two is key for both buyers and sellers. Cosmetic cracks are surface-level flaws, often caused by things like drying plaster or minor settling. On the other hand, structural cracks penetrate through masonry or brickwork and may indicate that the building itself is shifting [10]. This distinction helps guide the necessary repairs and informs long-term decisions about the property.

The Building Research Establishment (BRE) has established a six-category system to classify cracks, ranging from negligible (up to 0.1mm) to very severe (over 25mm). Cracks wider than 3mm often suggest subsidence, which is a major concern for homeowners. In fact, clay shrinkage is responsible for about 75% of domestic subsidence claims in England and Wales [10].

The location and direction of cracks can also point to specific issues. For instance, diagonal cracks are often linked to subsidence, while vertical ones may indicate settlement. Horizontal cracks might suggest problems like heave or lintel failure [10][5]. Cracks around windows, doors, or extension junctions are particularly telling, as they often highlight structural movement. If cracks appear on both the interior and exterior of a wall, it’s a clear sign of through-wall structural movement [5].

| BRE Category | Crack Width | Severity | Action |

|---|---|---|---|

| 0 | Up to 0.1mm | Negligible | No action; normal decoration covers these |

| 1 | Up to 1mm | Very Slight | Easily filled during redecoration |

| 2 | Up to 5mm | Slight | May need professional repair; investigate if recurring |

| 3 | 5mm to 15mm | Moderate | Requires investigation; professional repair/repointing |

| 4 | 15mm to 25mm | Severe | Extensive repair; replacing sections of wall; structural engineer required |

| 5 | Over 25mm | Very Severe | Major repair or partial rebuilding; likely involves underpinning |

Source: BRE Digest 251 [10]

Repairing cracks can range from minor fixes to extensive structural work, depending on their severity. Cosmetic filling and redecoration for hairline cracks can cost between £50 and £200. Repointing mortar for cracked walls typically costs £300–£1,500 [10]. For more serious issues, replacing lintels above windows or doors can cost £500–£3,000 per opening [10][5].

More advanced repairs, such as crack stitching with helical bars, range from £1,000 to £5,000. Resin injection for stabilising foundations can cost between £5,000 and £25,000 [10][5]. Underpinning, which is often required for significant structural movement, can cost anywhere from £10,000 to £50,000 or more, depending on the extent of the work needed [10][5]. For cracks wider than 1mm, a structural engineer’s report is vital and typically costs £400–£800 [10].

Structural cracks can have a major impact on property value, with active issues potentially reducing it by 20–40% [5]. Mortgage lenders often see significant cracks as high-risk. They may hold back part of the loan (known as a retention) until the issues are resolved or even refuse to provide a mortgage for properties with severe structural problems. Sellers in England and Wales are legally required to disclose any known structural damage in Section 7.4 of the TA6 Property Information Form. Failing to do so can lead to claims of misrepresentation later on [10].

"Untrained buyers may not distinguish if a crack is a simple decorating job or whether it's an indication of a major structural issue with the building." – SSJ Surveyors [11]

Cracks in walls and ceilings can create uncertainty for potential buyers, often sparking fears of hidden structural problems. Even if a property has undergone stabilisation for historical movement, the absence of proper documentation can jeopardise a sale. Mortgage lenders typically require Building Control completion certificates and insurance-backed guarantees (usually valid for 10–25 years) for any past foundation or structural repairs [5]. Without these, properties may face significant challenges in securing financing.

For peace of mind and to ensure marketability, professional assessments are essential. Services like Survey Merchant can help identify the root cause of cracks and provide the necessary documentation, helping both buyers and sellers navigate these concerns with confidence.

Timber rot and damp in subfloors can seriously weaken a building's structural stability. Dry rot (Serpula lacrymans) is particularly damaging because it can spread through masonry and plaster to reach fresh timber [12]. This fungus thrives in damp, poorly ventilated spaces, feeding on the cellulose in wood and causing a distinctive cuboidal cracking that leaves the timber light and brittle [5][12]. Wet rot, on the other hand, remains confined to persistently damp areas and stops spreading once the moisture issue is resolved [5].

The level of timber decay has a direct impact on a building's structural soundness. Dry rot typically develops when timber moisture levels exceed 20%, often due to issues like blocked air bricks, leaking pipes, or failed damp-proof courses [12]. Once it takes hold, it’s crucial to remove the affected timber, including an additional safety margin of 300–600mm into sound wood [5][12]. If left untreated, rot can compromise floor joists, wall plates, and even upper-floor structures. Early detection is key - be on the lookout for signs like musty mushroom-like odours, white cottony fungal growth, brown pancake-shaped fruiting bodies, and springy or uneven floorboards [5].

Repair costs can vary significantly depending on the extent of the damage. For minor cases, which might involve removing small affected areas, applying fungicidal treatments, and addressing the moisture source, costs typically range from £1,000–£3,000 [12]. Moderate cases that require extensive timber removal, wall and floor treatments, and replastering can reach £3,000–£8,000 [12]. Severe cases involving the replacement of floor joists, wall plates, and major damp-proofing can cost anywhere from £8,000 to £30,000 or more [5][12]. Wet rot repairs are usually less expensive, costing around £1,000–£5,000, while woodworm treatment is generally between £500–£2,000 [5]. Installing or repairing a damp-proof course for a typical house adds another £1,000–£3,000 [5].

The high cost of repairs reflects the seriousness of timber rot and its impact on property value. Active dry rot can reduce a property's market value by 15–25%, highlighting the financial consequences of neglect [12]. Mortgage lenders often refuse to approve loans for properties with active dry rot unless a professional management plan and an insurance-backed guarantee are in place [1][12]. In England and Wales, sellers are legally required to disclose timber defects on the TA6 Property Information Form to avoid misrepresentation claims [12]. However, properties with a history of treated rot, supported by a valid Property Care Association (PCA) guarantee, usually experience little to no reduction in offers [12].

Timber rot is often seen as a major red flag for buyers, given its reputation for hidden and extensive damage. Many potential buyers withdraw when they discover it [1][12]. Even when buyers proceed, they may factor in a risk premium that exceeds the actual repair costs, reflecting the inconvenience and uncertainty of structural repairs [12]. Lenders may also impose a retention, holding back part of the mortgage until a specialist confirms that treatment has been completed successfully [12][1]. Professional surveys can confirm the success of treatments, satisfying lender requirements and easing buyer concerns. Services like Survey Merchant can help identify the root cause of damp and timber issues, providing the necessary documentation to reassure both lenders and buyers.

Next, we’ll discuss how gaps and uneven floors can further diminish property value.

Gaps and uneven floors are often red flags for unstable foundations. If you notice sloping floors or gaps between skirting boards and the floor, it could mean structural movement is at play, such as subsidence or heave [3][7]. These problems usually occur when the soil beneath a property shifts - shrinking, expanding, or failing to drain properly - leading to the building's frame warping [7]. In some cases, sloping floors on upper levels might indicate that a load-bearing wall has been removed without proper steel reinforcement [3].

Like foundation or roof defects, gaps and uneven floors can weaken a property's overall structure [5][1]. The seriousness of the damage depends on whether the movement is ongoing or has stabilised. Active movement is especially concerning, as it poses a direct threat to both safety and the property's financial viability [5][1]. Signs like sticking doors or windows often point to warped frames caused by shifting foundations [7]. In older homes, uneven floors may also stem from timber issues, such as joist rot or woodworm, which compromise the floor's support [14][1]. Structural problems are not uncommon in the UK, affecting 15–20% of residential properties, with subsidence alone impacting about 0.5% annually [5].

Repair costs can vary widely, depending on the root cause and the extent of the damage. A structural engineer’s report, which is often the first step, typically costs between £200 and £1,200 [7]. If subsidence is confirmed, resin injection - a less intrusive soil stabilisation technique - can cost anywhere from £7,000 to £25,000. Traditional underpinning, a more involved method, may range from £10,000 to £50,000 or more, often priced at £1,000–£1,750 per metre [5][7]. For timber-related issues, repairs can start at £500 but may exceed £20,000 in severe cases [1]. Once the structural issues are resolved, cosmetic fixes like replastering or redecorating can add another £2,000–£8,000 to the bill [5].

"Subsidence is one of the most feared survey findings, and for good reason. Active structural movement can make a property unmortgageable and reduce its value significantly." – Pine [1]

Active structural issues can slash property values by 20–40% [5]. Mortgage lenders typically refuse to approve loans for properties with unresolved movement unless a professional plan and guarantees are in place [1][7]. Cash buyers, on the other hand, often demand discounts of 10–25% or more for properties with active subsidence. Even properties with historical but treated movement require a Certificate of Structural Adequacy and ongoing monitoring reports to reassure lenders [1][7].

Buyers are quick to spot uneven floors and gaps during a simple 'walk test', as these defects can hint at serious structural problems [5][1][3][7]. Properties with these issues often struggle to attract mortgage-backed buyers, narrowing the pool of potential purchasers. A Level 3 Building Survey can provide a thorough structural assessment to determine whether movement is still active or has stabilised [7][13]. Services like Survey Merchant help property owners connect with certified surveyors who can produce detailed reports, offering clarity to both buyers and lenders. This level of transparency can be crucial in salvaging deals that might otherwise fall through due to structural concerns.

Structural defects can have a dramatic impact on property prices in the UK. Issues such as foundation cracks, uneven floors, or more severe problems like active subsidence, dry rot, and roof damage don’t just lower property values - they can also make securing a mortgage much harder [1][5]. In fact, in 2025, 26% of residential property sales fell through before completion, with 18% failing because survey findings revealed serious issues that buyers couldn’t overlook or renegotiate [15]. These figures show how structural problems don’t just affect the price tag - they can bring transactions to a standstill. This highlights the importance of professional property surveys.

Spotting these issues early can save you from skyrocketing repair costs and protect your investment. If left unchecked, small problems like cracks or damp patches can quickly spiral into significant structural failures [5]. As Andy Smith, Property Expert at Homemove, explains:

Ignored problems compound, transforming modest defects into major failures [5].

Professional surveys, such as RICS Level 2 HomeBuyer Reports or Level 3 Building Surveys, are crucial for uncovering hidden risks, including wall tie failure, timber decay, or non-compliant renovations, before committing to a purchase [2].

Survey Merchant connects buyers and property owners with RICS-qualified surveyors across the UK. These experts provide detailed Level 2 and Level 3 surveys to identify structural risks before they escalate into costly repairs. Whether you’re buying an older property, negotiating after a survey, or safeguarding your investment, a thorough inspection ensures you have all the facts to make informed decisions. Angela Kerr, Director at HomeOwners Alliance, emphasises:

Red flags on a house survey can make or break a property deal. Buyers often get cold feet if problems arise... and it can lead to sales falling through [15].

Cracks in walls can be cosmetic or structural, and understanding the difference is key. Pay attention to the width, pattern, and surrounding signs.

If you notice a crack getting wider over time or spot signs of structural strain, it’s wise to consult a professional for further evaluation.

Subsidence can complicate the process of getting a mortgage, especially if the problem is serious or unresolved. For minor cases, however, financing is often still possible, and it might even open the door to negotiating a lower property price. Mortgage lenders usually evaluate the severity of the issue along with any necessary repairs before deciding whether to approve the loan.

If you’re worried about structural problems, a full structural survey is your go-to choice. This detailed inspection looks at issues such as subsidence, problems with the foundations, and any structural movement. It’s ideal for older homes, listed buildings, renovated properties, or if you’ve noticed visible damage, as it provides an in-depth evaluation of the main structural components.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes