You're often closest to a property decision when the risk feels least visible. A buyer is about to exchange and notices hairline cracking that wasn't obvious on the viewing. A landlord renews a lease and realises the repairing obligations are far less clear than expected. A portfolio manager gets an insurance renewal and suspects the declared values no longer reflect rebuild reality.

That's where property risk management stops being an abstract phrase and becomes a practical discipline. It's about finding what can damage value, interrupt occupation, trigger liability, or weaken negotiating position, then dealing with it before the issue becomes expensive. For a house purchase, that may mean identifying hidden defects early enough to renegotiate. For a landlord, it may mean documenting responsibilities properly and keeping inspection records. For a commercial owner, it may mean combining surveys, legal review, maintenance planning, and insurance strategy into one coherent approach.

Multi-disciplinary surveyors sit at the centre of that process because most property risks don't stay neatly in one box. A roof defect becomes a tenant issue. Poor fire compartmentation becomes an insurance issue. An unclear boundary becomes a legal and valuation issue. Good advice joins those dots.

Table of Contents

- What Is Property Risk Management and Why It Matters

- Structural and physical risk

- Environmental risk

- Legal and leasehold risk

- Financial and market risk

- Operational and management risk

What Is Property Risk Management and Why It Matters

Completion day can feel like the finish line until a survey issue, title problem, or uninsured defect surfaces after the keys change hands. At that point, the cost is rarely limited to the repair itself. A single overlooked risk can affect finance terms, insurance cover, tenant occupation, statutory compliance, and the price a future buyer is prepared to pay.

Property risk management is the process of spotting those exposures early, judging their likely effect, and deciding what action makes financial sense. The principle is the same whether you are buying a flat, managing a rental house, or overseeing a mixed-use portfolio. The scale changes. The discipline does not.

In practice, the work usually falls into three broad responses. Remove the risk if the asset or transaction no longer stacks up. Reduce it through repair, maintenance, monitoring, or better management. Transfer part of it through insurance, warranties, lease terms, or specialist appointments. Good decisions often involve a mix of all three, because no single measure deals with every consequence.

For a homebuyer, that may mean withdrawing from a purchase with movement, damp, or legal constraints that exceed the available budget. For a landlord, it may mean accepting a known defect but pricing the repair properly and tightening inspection and maintenance routines. For a commercial owner, it often means coordinating building surveyors, valuers, engineers, and legal advisers so the physical issue, occupational impact, and financial exposure are assessed together.

Practical rule: If a risk cannot be described clearly, it usually cannot be priced, managed, or transferred properly.

That is why surveys should be commissioned early, not treated as a formality once heads of terms are agreed. A sound inspection replaces assumption with evidence. It helps distinguish cosmetic wear from structural concern, deferred maintenance from immediate liability, and acceptable risk from the sort that changes the investment case. For a useful primer on avoiding property risks with surveys, start there.

Multi-disciplinary input earns its keep by connecting these dots. A defect in the roof is not only a building issue. It can become a service charge dispute, an insurance claim, a rent-free negotiation, or a valuation adjustment. That point is important because a risk that appears to be transferred can still return as an uninsured shortfall, a claim dispute, or a gap between the reinstatement cost and the actual cost of putting the building right.

Risk management is not reserved for institutional investors. Anyone responsible for property is making risk decisions, whether deliberately or by default. The advantage of a structured approach is simple. It protects people, supports income and value, and gives owners at every scale a clearer basis for action.

The Five Core Categories of Property Risk

A property rarely fails in just one way. A roof leak can become a health and safety issue, a tenant dispute, an insurance problem, and a budget overrun within the same quarter. That is why risk needs to be split into categories that owners, landlords, and portfolio managers can assess in a consistent way.

The five categories below work across different types of ownership. A first-time buyer, a private landlord, and a commercial asset manager will see different symptoms, but the underlying framework is the same. The value of a multi-disciplinary surveyor is that these risks are not reviewed in isolation. Building defects, compliance duties, lease obligations, and financial exposure often sit in the same problem.

Structural and physical risk

This category covers the condition of the building and the reliability of its components. It is usually the first risk clients recognise because it is the one they can see, although visible defects are often only part of the story.

For a homebuyer, the immediate concerns may be cracking, damp, timber decay, roof defects, or signs of movement. For a landlord, the focus often shifts to common parts, drainage, windows, balconies, and elements close to the end of their service life. In commercial property, physical risk often centres on plant failure, façade condition, water ingress, and maintenance liabilities that can disrupt occupation or trigger claims under a lease.

Typical examples include:

- Building movement: Cracking, racking, sloping floors, and sticking doors or windows need interpretation, not guesswork.

- Moisture-related defects: Damp may arise from a roof leak, failed rainwater goods, plumbing defects, bridging, condensation, or poor ventilation.

- Fabric failure: Roof coverings, flashings, cladding, pointing, sealants, and rainwater disposal all become risk points when inspection and maintenance are weak.

The trade-off is straightforward. Early repair costs money. Delayed repair usually costs more and may bring loss of rent, avoidable damage to finishes, or argument about who should pay.

Environmental risk

Environmental risk sits partly in the site and partly in the building. It includes flood exposure, contaminated land, invasive plants, ground instability, hazardous materials, overheating risk, and the effect of severe weather on continued use.

Older buildings can carry asbestos or concealed contamination from earlier uses. Low-lying sites may face recurring flood exposure even where the building itself appears sound. A commercial estate near water, for example, may remain lettable in normal conditions but still carry insurance, business interruption, and resilience concerns that affect value and tenant demand.

Timing matters here. Environmental issues found before exchange can alter price, contract terms, insurance decisions, or the decision to proceed. The same issue found after completion becomes the owner's problem to fund and manage.

Legal and leasehold risk

A property can be physically sound and still expose the owner to a poor deal. Legal risk often sits in title matters, rights of way, restrictions on use, repairing covenants, service charge provisions, licences for alterations, fire safety responsibilities, and gaps between what the lease says and what the building needs.

This category is particularly important where occupation and ownership are split, which is common across the UK property market. In leasehold flats, the main risks may sit in the management structure, reserve funds, repair obligations, or defects in the lease itself. In commercial property, the pressure points are often reinstatement terms, yield-up obligations, compliance clauses, alienation provisions, and disputes over whether an item is landlord's or tenant's responsibility.

Survey findings and lease review need to be read together. There is little value in identifying a failing roof if no one has checked who must repair it, whether the cost is recoverable, and how the wording interacts with actual condition on site.

Financial and market risk

Some risks sit in the accounts rather than the fabric. Underinsurance, weak capital expenditure planning, rent interruption exposure, void risk, functional obsolescence, and changing occupier demand all affect the performance of a property even where the building is in reasonable condition.

I often see this category underestimated because the building appears to be coping. That can be misleading. An owner may defer £20,000 of planned works only to inherit a £100,000 problem once water damage spreads, access costs rise, or a tenant seeks compensation for disruption.

Market conditions also matter. A tired office building with no obvious structural defect may still carry significant risk if its layout, energy performance, or services no longer meet occupier expectations. In that case, the issue is not repair alone. It is whether the asset remains competitive without further investment.

Operational and management risk

Operational risk is about how the property is run. Weak inspection routines, poor record keeping, unclear responsibilities, inconsistent contractor management, and slow escalation of defects all increase exposure, even where the building itself is not unusually problematic.

The pattern is similar across ownership types:

- For homeowners: missed maintenance allows small defects to become expensive repairs.

- For landlords: incomplete records and irregular inspections make liability and service charge disputes harder to resolve.

- For commercial operators: poor coordination between facilities, asset management, legal advisers, and insurers creates blind spots that delay decisions and increase loss.

This category is often the cheapest one to improve. Better reporting lines, planned inspections, clear ownership of actions, and proper records do not remove every risk, but they do make risks easier to spot early and cheaper to control.

A Practical Framework for Assessing and Prioritising Risk

A long defect list isn't a risk strategy. The job is to decide what matters first, what can wait, and what should change the transaction or management plan immediately.

Start with the right property data

Risk assessment is only as good as the information behind it. In UK practice, thorough assessments require accurate data on property location, construction materials, building age, occupancy type, and historical loss data, with broader approaches increasingly using real-time property condition reports, according to research on the perception and management of risk in UK office property development.

That list is useful because it forces discipline. If you don't know what the building is made of, how it's used, where its vulnerabilities sit, or what has happened before, your conclusions will be shallow. A converted building, for example, often carries different risks from one purpose-built for its current use.

Plot risks by likelihood and impact

Surveyors, managers, and insurers often think in terms of likelihood and impact. The first asks how probable the issue is. The second asks how serious the consequence will be if it happens.

Take a roof leak. If inspection evidence shows failed coverings and blocked outlets, the likelihood may be high. If the affected area sits above critical tenant space or expensive internal finishes, the impact may also be high. That issue moves to the top of the action list.

Compare that with a worn but functioning internal finish in a low-traffic area. The likelihood of further cosmetic deterioration may be high, but the impact is low. That's usually a planned maintenance item, not an urgent intervention.

Don't prioritise by how alarming a defect sounds. Prioritise by what it's likely to do, how quickly, and what it will cost if left alone.

Risk Prioritisation Matrix

| Impact | Low Likelihood | Medium Likelihood | High Likelihood |

|---|---|---|---|

| Low | Monitor during routine inspections | Add to planned maintenance list | Address when cost-effective |

| Medium | Review at next survey cycle | Prepare targeted remedial works | Act soon and assign responsibility |

| High | Put under active review | Escalate for detailed investigation | Immediate action and contingency planning |

A simple matrix like this helps clients stop treating every issue as equally urgent. It also improves budgeting. When the high-impact, high-likelihood items are clear, you can separate essential works from desirable improvements.

Use the matrix consistently. Record the reason for each rating. Update it after repairs, lease events, occupation changes, or new evidence from surveys and inspections. That's how property risk management becomes a live process rather than a report that sits unread in a folder.

Using Surveys and Inspections to Identify Hidden Risks

The most expensive risks are often the ones a casual viewing won't reveal. Surface condition can look acceptable while the actual problem sits behind finishes, above ceilings, beneath coverings, or inside the document trail.

Match the inspection to the risk

Different risks require different tools. A buyer assessing a conventional house may start with a RICS Level 2 Survey where the property appears relatively standard and condition concerns are moderate. Older, altered, larger, or visibly distressed buildings often justify a Level 3 Building Survey because the advice needs to go further on defects, probable causes, repair implications, and future expenditure.

Environmental concerns need their own route. Flood sensitivity, contamination, and historic land use often need environmental search work and specialist interpretation. Suspected hazardous materials require targeted investigation. If asbestos is part of the concern, Survey Merchant asbestos insights give a useful overview of why identification and management matter before refurbishment or occupation decisions.

Legal risk isn't solved by a building survey alone. Title review, lease analysis, licences for alterations, and planning history need input from solicitors and, where relevant, managing agents or landlords. Operational risk may need inspection of plant, maintenance records, fire safety arrangements, and contractor regimes.

A practical mapping looks like this:

- Structural concerns: Building survey, defect report, roof inspection, or drone inspection.

- Moisture and heat loss patterns: Specialist diagnostics, including thermal imaging inspection services, can help reveal concealed moisture paths, insulation gaps, and anomalous temperature patterns that aren't obvious to the naked eye.

- Environmental hazards: Environmental search, asbestos survey, flood review, or specialist testing.

- Legal exposure: Solicitor review of title, lease, covenants, and consents.

- Operational weaknesses: Fire risk assessment, servicing review, maintenance audit, and compliance checks.

Why visual checks aren't enough

Owners sometimes assume a competent walk-round is enough. It isn't. Visual checks are useful, but they have limits. They don't measure hidden moisture migration reliably, they don't test legal wording, and they don't model broader vulnerability.

In UK property risk practice, the COPE framework stands for Construction, Occupancy, Protection, and Exposure. It is described as the primary technical specification for quantifying commercial and residential vulnerabilities and supports capex forecasting and insurance premium modelling in Smarty's article on using property data for real estate risk management. The point isn't the acronym itself. The point is that professionals assess risk through several layers at once.

A sound inspection process asks four basic questions. What is the building made of. How is it used. What protection exists. What external exposures could turn a defect into a loss.

Multi-disciplinary input earns its keep: the surveyor identifies building issues, the environmental specialist tests specific hazards, the solicitor clarifies obligations, and the insurance adviser checks whether the declared risk profile still fits the actual asset. Hidden risk usually stays hidden when each adviser works in isolation.

Effective Strategies for Property Risk Mitigation

A mitigation plan is tested when the building is still trading, tenants are in occupation, and the budget is finite. A homebuyer may be deciding whether to proceed at all. A landlord may need to phase works across several properties. A portfolio manager may be balancing premium pressure, compliance exposure, and capex timing across multiple assets. The principles are the same, but the response has to match the scale of ownership and the consequence of getting it wrong.

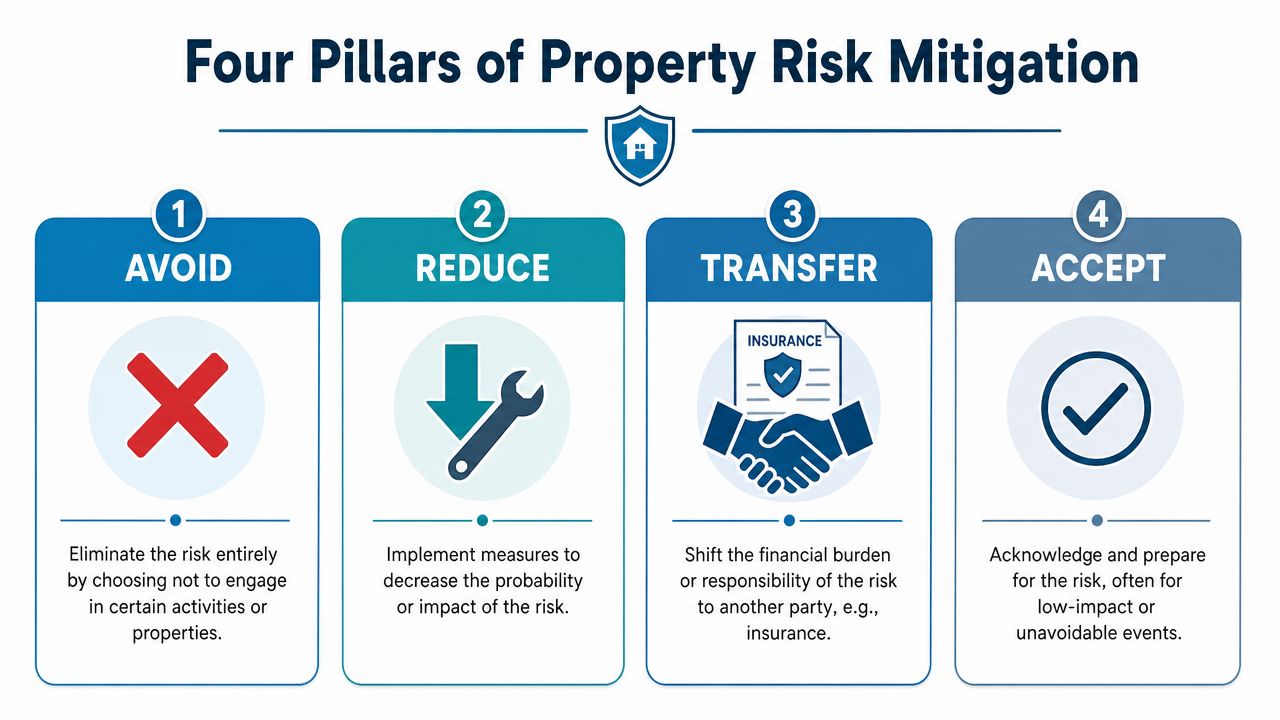

Avoid, reduce, transfer, accept

These four routes give owners a workable structure for decision-making.

Avoid means declining the exposure altogether. For a buyer, that may mean withdrawing where flood history, structural movement, title complications, and repair cost combine into a poor investment case. For a landlord or asset manager, it may mean refusing a proposed use that would increase fire load, servicing demand, or wear beyond what the building can safely support.

Reduce means lowering either the likelihood of a problem or the cost if it occurs. Most property risk work falls into this category. Typical measures include repairing roof coverings before moisture reaches finishes and structure, improving drainage to limit repeat water ingress, upgrading fire compartmentation, replacing life-expired elements on a planned basis, and tightening inspection intervals where defects are known to progress quickly.

Fire safety is a good example because effective control rarely depends on one product or one inspection. It depends on the building fabric, the alarm strategy, records, maintenance, management arrangements, and how the premises are used. Owners and managers looking for a practical reference point may find Wisenet's fire safety guide useful.

Transfer usually means insurance, though lease terms, warranties, indemnities, and service contracts can transfer part of the financial exposure as well. This has limits. Insurance does not repair a neglected roof before tenants complain, and it does not remove the business interruption, excesses, exclusions, or time spent evidencing a claim.

Accept is appropriate for minor issues with low consequence that are understood and costed. A small defect with no immediate safety implication may be monitored until planned works are due. The key is to record the decision, set a review date, and make sure accepted risk does not become unmanaged deterioration.

Where mitigation plans fail

The weak point is often not identification. It is follow-through.

Owners regularly commission reports, agree that defects matter, then delay action because the building is still operational and no one issue looks urgent in isolation. Over time, small defects become linked losses. A slipped tile becomes water ingress. Water ingress damages insulation, ceilings, and electrics. The claim then raises questions about maintenance history, reinstatement cost, and whether the policy schedule still reflects the asset as it stands today.

Underinsurance is part of that problem, but a hard percentage is less useful than the practical point. A significant share of UK property is insured on figures that do not match current rebuild cost, site conditions, professional fees, demolition, or inflation in specialist materials. When that happens, risk transfer is only partial. The owner still carries a funding gap.

The stronger approach is to treat mitigation as a package rather than a single fix. Survey findings should feed into maintenance planning. Maintenance planning should inform insurance reviews. Insurance reviews should be checked against lease responsibilities, occupancy, and any material changes to the building.

A workable response plan usually includes:

- Immediate actions: life safety defects, active leaks, serious structural concerns, security failures, or compliance gaps that expose the owner to immediate loss.

- Short-term works: repairs or upgrades that prevent repeat damage, tenant disruption, or avoidable claims within the next maintenance cycle.

- Insurance and contract review: declared values, excesses, exclusions, reinstatement assumptions, lease liabilities, and contractor responsibilities.

- Planned investment: phased capital works for elements nearing the end of service life, especially where failure would affect safety, income, or insurability.

- Monitoring: inspection dates, condition triggers, photographic records, and a clear point at which a monitored issue becomes a repair instruction.

For smaller owners, that may be a disciplined annual review with a surveyor and broker. For larger portfolios, it usually means a live risk register tied to inspections, capex forecasting, and occupancy data. Multi-disciplinary input matters in both cases because the building problem, the legal obligation, and the financial consequence are rarely identical.

Case Studies and Checklists for Every Property Owner

General advice becomes useful when you can see how it works in real decisions. The examples below are illustrative practice scenarios, not claimed client results.

Three practical examples

A first-time homebuyer agreed terms on a period house that looked well presented. The survey identified roof defects, damp-related deterioration at lower walls, and evidence that earlier alterations needed closer legal checking. The key value of the report wasn't drama. It was clarity. The buyer could separate urgent items from routine upgrading, ask targeted questions through the solicitor, and renegotiate from an informed position rather than vague suspicion.

A landlord with several mixed-age residential units had no single view of condition across the portfolio. Some properties had ad hoc repairs, some had incomplete compliance records, and inspection notes were inconsistent. Once the risks were grouped by building condition, fire precautions, and tenancy obligations, the landlord could phase works properly, improve documentation, and stop treating every issue as a last-minute emergency.

A commercial property manager inherited a multi-let building with recurring water ingress complaints. Initial assumptions blamed tenant alterations. A more structured review pointed to roof drainage, detailing defects, and weak inspection follow-up. The result wasn't merely a repair order. It was a capex and maintenance plan tied to actual risk areas, with clearer communication to occupiers about timing, access, and responsibilities.

Good property risk management often changes the question from “What's wrong with this building?” to “What do we need to do first, and who is responsible for it?”

Checklists you can use

Homebuyer checklist

- Commission the right survey: Match the survey type to the age, condition, and complexity of the property.

- Review legal documents with the findings in mind: Ask whether defects, alterations, boundaries, or rights affect the deal.

- Distinguish urgent from non-urgent items: Not every defect justifies renegotiation, but some certainly do.

- Budget for ownership, not just purchase: Include repairs, maintenance, and investigation costs in your decision.

Landlord checklist

- Keep inspection records organised: Dates, findings, actions, and follow-up should be easy to retrieve.

- Clarify repairing responsibilities: Make sure lease wording and practical management line up.

- Prioritise life safety and water ingress: These issues escalate quickly in occupied buildings.

- Review insurance against actual condition: Don't assume the policy still matches the asset.

Commercial owner or manager checklist

- Create an asset risk register: Track issues by likelihood, impact, responsible party, and target date.

- Integrate advisors: Survey, legal, compliance, and insurance work should inform each other.

- Plan capex before failure: Life-expired elements rarely fail at convenient moments.

- Communicate with occupiers: Poor communication turns manageable works into operational disputes.

One final point matters across all three groups. A checklist is not a substitute for judgement. It's a way to make sure obvious gaps don't get missed while professional advice deals with the more technical points.

How to Instruct a Surveyor and Get the Advice You Need

The quality of the instruction shapes the quality of the advice. If the brief is vague, the report may answer the wrong question.

Start with the basics. Tell the surveyor the property type, age, size, location, tenure, and current use. State the transaction context as well. Purchase, lease renewal, planned refurbishment, portfolio review, insurance concern, or dispute support all require different emphasis. If you already know about cracking, leaks, asbestos concerns, tenant complaints, or missing documents, say so at the outset.

It also helps to be clear about the outcome you need. Some clients want a broad condition picture. Others need a focused defect diagnosis, a valuation, a reinstatement assessment, or advice that supports negotiation. Surveyors can do much more useful work when they know whether the priority is acquisition, compliance, budgeting, or liability management.

Professional accreditation matters, but so does relevance. A chartered surveyor with experience in older residential buildings may not be the right fit for a commercial dilapidations instruction, and vice versa. You should ask who will inspect, what the scope includes, what it excludes, and whether specialist follow-on investigations may be needed. If you're comparing providers, this guide on how to find a UK property surveyor is a helpful benchmark for what to ask.

The best instructions are specific without trying to diagnose the building yourself. Describe the symptoms, provide the paperwork you hold, and let the surveyor shape the scope around the actual risk.

If you need impartial help finding the right surveyor for a purchase, a landlord issue, or a commercial instruction, Survey Merchant connects clients with a nationwide panel of multi-disciplinary professionals suited to the property type and risk involved. That makes it easier to get focused advice, competitive quotes, and reporting that helps you act with confidence.