You're probably here because you need a number quickly.

Perhaps you're buying a small parade shop, refinancing an office, checking whether an asking price looks sensible, or trying to decide if a vacant unit is worth refurbishing. In that moment, an online commercial property valuation calculator in the UK feels like the obvious first step. Type in a few figures, press a button, and get something usable.

That instinct makes sense. Commercial property decisions are expensive, time-sensitive, and often made before you've assembled every lease, account, and schedule of condition. In a market that's both active and economically significant, speed matters. The UK commercial property industry directly contributed approximately £74 billion to the economy in 2022, and 8,324 commercial properties were available for sale across the UK as of early 2026, according to the Investment Property Forum Property Data Report.

The problem isn't that calculators exist. The problem is that many people mistake a quick estimate for a proper valuation.

A basic online tool can be helpful when you want to sense-check a simple, tenanted asset. If you want to calculate commercial property value at a high level, these tools can support early thinking. But they break down fast when the property is vacant, partly let, in poor condition, subject to odd lease terms, or bought for redevelopment rather than income.

That distinction matters more than most first-time investors realise.

Table of Contents

The Promise of an Instant Commercial Property Valuation

Speed is the attraction.

Most owners and investors don't start with a full valuation instruction. They start with a practical question. Is this guide price in the right area? Does this rent justify the purchase price? If I improve the letting position, could the property be worth more? A commercial property valuation calculator in the UK answers that urge for a quick first pass.

Why calculators feel useful

A simple tool reduces a complex market into a single figure. That's reassuring when you're comparing several opportunities or trying to make sense of a brochure that gives you rent, floor area, and little else.

For straightforward, income-producing assets, that shortcut can be useful. If a property is let on normal terms, with reasonably clear costs and a market-facing yield, the calculator can give you a rough indication of value. That's often enough to decide whether to investigate further.

Practical rule: Use an online calculator for screening, not for commitment.

Why the stakes are high

Commercial property isn't a niche corner of the market. People use valuation numbers to support purchases, disposals, lending discussions, tax planning, probate work, lease events, and internal portfolio reviews. A rough estimate can open the door to useful analysis, but a weak assumption can also send you in the wrong direction very quickly.

That's why experienced investors treat instant tools as the beginning of a process, not the end of one.

A calculator is strongest when the building is ordinary, the lease is understandable, and the income stream is stable. It becomes much less reliable when the asset has a story attached to it. That story might be vacancy, disrepair, redevelopment hope, restrictive planning, short lease expiry, tenant weakness, or unusual repair liabilities. None of those points fit neatly into a one-line form field.

So the promise is real. Instant valuation tools save time, impose discipline, and help you frame questions. But they only work properly when the property fits the model the tool expects.

How a Commercial Valuation Calculator Actually Works

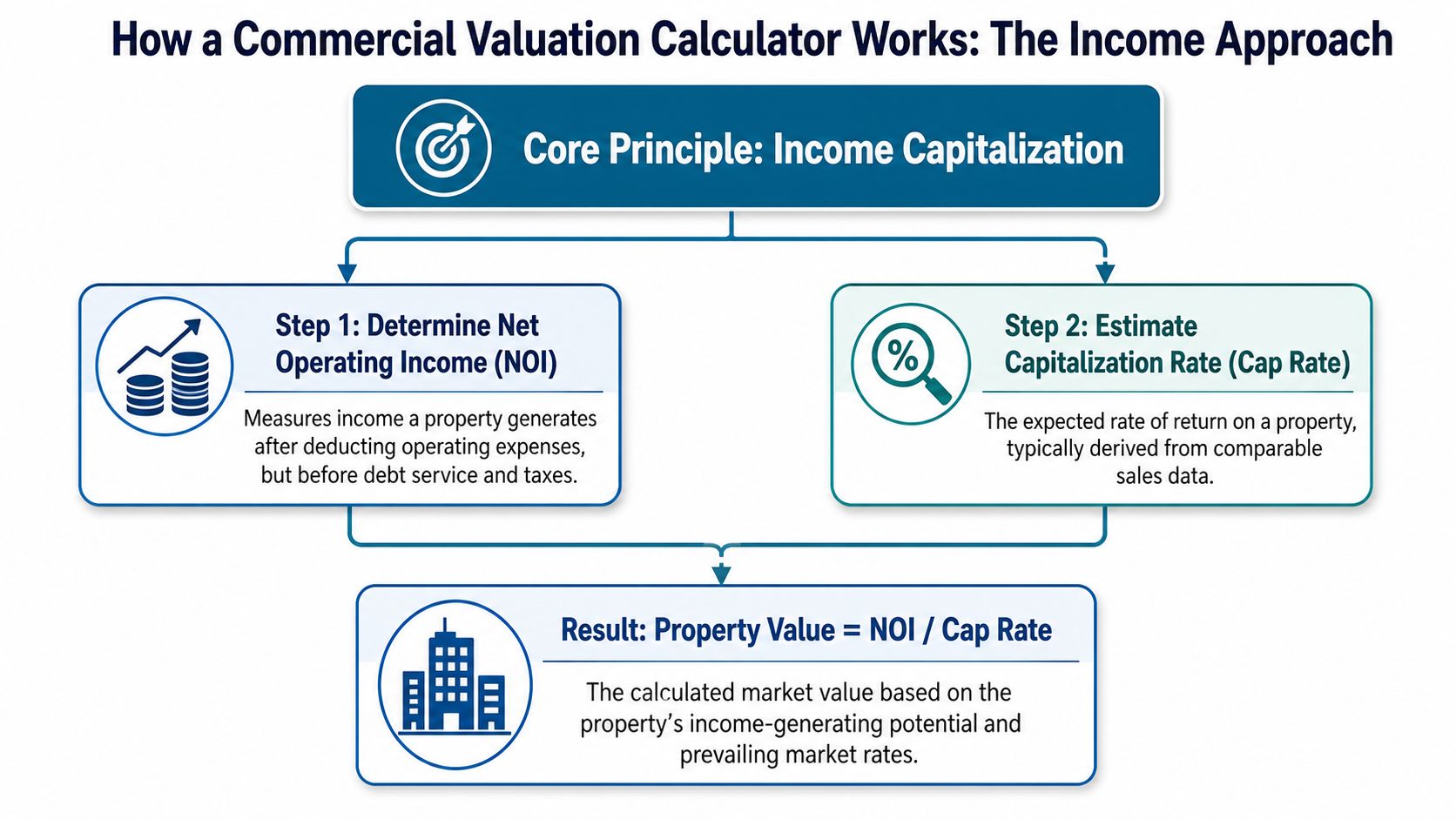

Most online tools are doing one thing. They're applying the income capitalisation method.

That sounds technical, but the logic is simple. A buyer of an income-producing commercial building is often asking, “What income does this asset produce, and what rate of return would the market expect for that type of property?” Put those two pieces together, and you get an indicative capital value.

The core formula behind most tools

The most common quick calculation used by surveyors and lenders is:

Commercial Property Value = Annual Net Rent ÷ Yield

A property producing £60,000 in annual net rent with a 6.5% market yield gives an indicative value of around £923,000, as explained in this guide to the commercial property income capitalisation method.

The easiest way to think about this is to compare it with any investment that produces a return. If the income is stronger, value tends to rise. If the return investors demand is higher, value tends to fall.

Three inputs drive the result:

- Net operating income. This is the income left after deducting operating expenses such as insurance, management fees, repairs, and a void allowance.

- Yield, also called the capitalisation rate. This reflects the return buyers expect for that type of asset in that location and risk profile.

- Market evidence. The yield isn't guessed. In practice it comes from comparable transactions and local judgement.

If you want a plain-English refresher on mastering NOI and cap rates, that resource is useful because it explains the investment logic behind the formula without overcomplicating it.

What the calculator is really assuming

Readers often encounter a common pitfall. The calculator looks objective, but it's only as reliable as the assumptions behind the figures.

If you enter the passing rent without checking whether that rent is sustainable, you can overstate value. If you choose a yield that's too sharp for the location or tenant quality, you can do the same. If you ignore expenditure that a buyer would price in, the output becomes optimistic.

A calculator doesn't inspect the building, read the lease in detail, or challenge your assumptions.

That's why many investors use a desktop estimate as a first look only. If you'd like to understand UK desktop valuations, it helps to distinguish between a remote, assumption-based exercise and a valuation supported by fuller evidence and inspection.

A decent online tool is therefore not a valuer. It is a formula wrapper. It can be handy, but it can't think.

How to Use a UK Commercial Property Valuation Calculator

If you're using a calculator for a simple tenanted asset, the best approach is to work backwards from realistic net income rather than forwards from the headline rent on the brochure.

That sounds obvious, but many users type in the annual rent and stop there. A surveyor doesn't. The surveyor asks what income a prudent investor would treat as maintainable after normal deductions.

Start with the income, not the headline rent

For a retail property, gather the basic ingredients first:

The rental income

Use the annual rent receivable, then sense-check whether it reflects the market and the lease position.Operating costs

Deduct recurring items that affect net income. Typical examples include insurance, management fees, repairs, and an allowance for voids.Business rates context

For England in the 2026/27 cycle, calculators dealing with affordability and occupational cost may need to reflect business rate multipliers such as 48p for standard non-retail, hospitality and leisure properties with rateable values between £51,000 and £499,999, and 50.8p for properties at £500,000 RV and above, as outlined in this explanation of ITZA and business rates inputs.The yield

This should reflect market evidence for the property type, location, and covenant quality. It's the most judgment-heavy field in the whole process.

A worked retail example

For shops and some office layouts, surveyors may also refer to ITZA, meaning In Terms of Zone A. That method zones floor space by its value relative to the frontage, rather than treating all square footage as equal. Online calculators rarely explain this well, but it matters because front trading space usually commands more value than deeper secondary space.

Here's a simple way to organise your thinking before using a calculator:

| Step | Calculation Component | Example Value | Notes |

|---|---|---|---|

| 1 | Gross annual rent | £60,000 | Starting point only |

| 2 | Less operating expenses | User input required | Include insurance, management, repairs, void allowance |

| 3 | Less rates impact where relevant | User input required | Reflect occupational cost assumptions where appropriate |

| 4 | Net operating income | Derived figure | This is the key valuation input |

| 5 | Yield | User input required | Must reflect local market evidence |

| 6 | Indicative value | NOI ÷ Yield | Ballpark result, not a formal valuation |

A few practical cautions help:

- Don't ignore the lease wording. A rent figure means less if there's a break clause, arrears issue, or unusual repairing obligation.

- Don't flatten retail space into one rate. ITZA exists because frontage and depth don't contribute equally to rental tone.

- Don't treat business rates as background noise. They affect affordability, which in turn affects investor assumptions about net income.

Check the question first: Are you valuing the current income stream, the fully let investment, or the property after works? Each needs different inputs.

If the property is ordinary and occupied, this approach can produce a sensible starting point. If it isn't, the tool begins to strain.

Common Pitfalls and Limitations of Online Calculators

The biggest weakness in the typical commercial property valuation calculator in the UK isn't that it's simplistic. It's that it often assumes every commercial property should be valued as though it already produces stable rent.

That's fine for a standard let investment. It's hopeless for many real assets.

Where the model fails outright

Online calculators almost exclusively use the income capitalisation method, which makes them ineffective for vacant, development, or distressed assets with no rental income, as shown by this review of a typical commercial property valuation calculator format. If there is no income, the formula has nothing useful to capitalise.

That creates a real valuation gap for:

- Vacant offices that need incentives, reconfiguration, or major repair before they can be let

- Empty retail units in secondary pitches where the challenge is reletting, not capitalising existing income

- Development sites where value depends on land, planning, build costs, and exit assumptions

- Distressed buildings where a buyer is pricing risk, remedial works, and downtime

In those situations, professionals may use the cost approach or sales comparison approach instead. A simple web calculator rarely lets you switch method.

If you're trying to stress-test the income side of a let building, a basic guide to calculating rental income can still be useful as a rough screening companion. But it doesn't solve the empty-property problem.

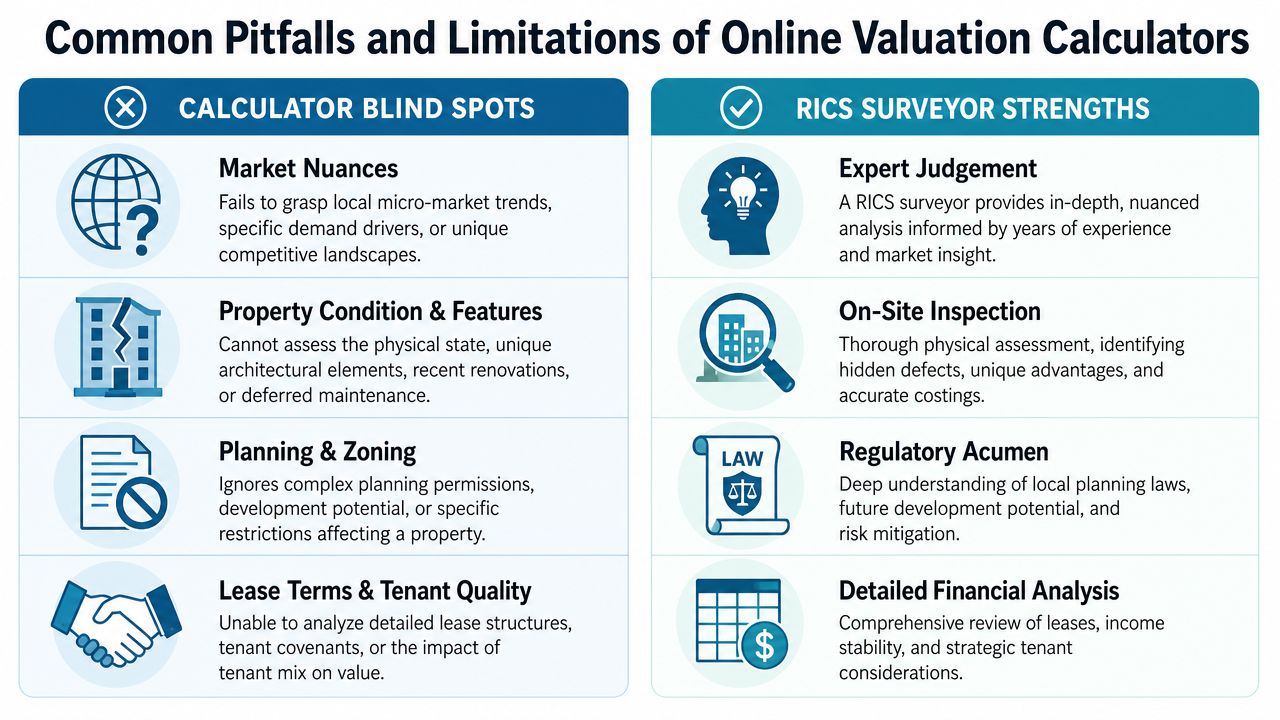

What the calculator cannot inspect or judge

Even when the building is producing income, the tool still can't assess matters that directly influence value.

Consider what it misses:

Physical condition

It can't see roof failure, damp ingress, outdated services, poor loading arrangements, or non-compliant alterations.Lease complexity

It won't read rent review clauses, tenant breaks, service charge caps, repairing liabilities, or unusual incentives.Tenant quality

It doesn't judge whether the covenant is strong, weakening, or already under pressure.Planning and use constraints

It won't analyse whether the current use is vulnerable, restricted, or ripe for change.

A vacant secondary office and a fully let office can sit on the same road and need completely different valuation methods.

That's the heart of the limitation. Calculators are narrow tools. Property is not a narrow subject.

When to Instruct a RICS Chartered Surveyor

There comes a point where using a calculator stops being efficient and starts being risky.

A proper valuation is not just a more polished version of an online estimate. It is a professional opinion prepared under recognised standards, supported by evidence, and accountable to the client who relies on it.

Situations where a calculator is not enough

You should stop relying on an instant tool and instruct a qualified surveyor when the valuation is being used for a real decision with legal, lending, or tax consequences.

That usually includes:

Securing finance or refinancing

Lenders need defensible evidence, not a self-generated estimate.Probate or matrimonial matters

The valuation may be scrutinised by other parties, advisers, or the court.Tax work

If the figure supports a tax position, it needs a proper rationale and file.Purchase or sale negotiations

A professional valuation helps you challenge price with evidence rather than intuition.Lease events and disputes

Rent reviews, lease renewals, dilapidations context, and strategic negotiations often turn on careful interpretation of facts.Vacant, unusual, or development property

As covered earlier, these need methods that most calculators can't apply.

Why formal valuation standards matter

In the UK, valuation standards are governed by RICS through the Red Book. That matters because the valuer is not merely producing a number. The valuer is giving an impartial opinion for a stated purpose under a recognised framework.

If you need a closer look at the standard itself, this explanation of RICS Red Book valuations is a helpful starting point.

A formal valuation carries things an online tool can't offer:

- a defined basis of value

- a stated purpose and assumptions

- inspection and evidence

- professional accountability

- indemnity-backed advice

That's what turns a rough estimate into something fit for decision-making.

The Difference Between a Number and a Valuation

A calculator gives you a number. A valuer gives you an opinion.

Those may sound similar, but they're not the same thing at all.

What an automated number can do

An online estimate is useful for quick screening. It helps you test scenarios, compare opportunities, and ask better questions. For a standard, income-producing property, that can be enough to decide whether a deal deserves more time.

Used properly, it's a thinking tool.

It's particularly good for early conversations. You can model what happens if the rent changes, if costs rise, or if the yield moves. That's useful investment discipline.

What a professional valuation adds

A valuation is more than arithmetic. The surveyor considers the building, location, evidence, lease structure, condition, legal context, and the purpose of the instruction. Then the surveyor reconciles those factors into a reasoned conclusion.

The most dangerous mistake is treating a neat answer as a reliable one.

That's why experienced owners separate exploration from commitment. They use calculators to shape their view, then use professional advice when the number will influence money, liability, negotiation, or legal position.

If the asset is vacant, unusual, or capable of redevelopment, that distinction becomes sharper still. In those cases, the wrong method doesn't just produce an imprecise figure. It can produce the wrong answer entirely.

From Estimate to Certainty with Expert Valuation

A commercial property valuation calculator in the UK has a place. It can help you sense-check a simple let investment, run a quick scenario, and avoid starting from a blank page.

But that's all it is. A starting point.

The moment the property becomes more complex, or the decision becomes more important, you need more than a formula. You need method selection, evidence, inspection, and professional judgement. That's especially true for vacant buildings, refurbishment opportunities, and development assets, where the usual rent-and-yield shortcut often doesn't apply.

If you're weighing a transaction, planning a refinance, dealing with probate, or trying to pin down the value of a non-standard commercial asset, the sensible next step is to move from estimate to advice. A good place to begin is to understand how independent valuations for UK properties differ from informal pricing tools and why independence matters when the number has consequences.

If you need a dependable commercial valuation rather than a rough online estimate, Survey Merchant can connect you with a suitably qualified surveyor from its UK-wide panel. It's a practical way to obtain impartial, competitively priced advice for commercial property, whether you need a formal valuation for lending, tax, probate, dispute resolution, or a purchase decision.