If your lease has 80 years or fewer left, leasehold marriage value can apply and the freeholder is entitled to 50% of that calculated uplift in value. The complication is that although the Leasehold and Freehold Reform Act 2024 abolishes marriage value in law, that change is currently suspended, so many homeowners still need to make decisions as if the old rules remain in force.

That's the position many leaseholders find themselves in right now. You've checked your lease term, realised it's getting uncomfortable, and then found conflicting advice online. One article says marriage value has gone. Another says it still matters. A third talks about reform as if it's already on the ground.

From a valuation point of view, the issue is simple. From a practical point of view, it isn't. The number of years left on your lease affects what your extension is likely to cost, how buyers and lenders view the flat, and whether waiting is a sensible strategy or an expensive mistake.

A homeowner with a healthy lease can plan calmly. A homeowner hovering around the threshold often can't. Once the term is short enough for marriage value to bite, delay can become costly very quickly. That's why this topic matters so much to your wallet, not just to lawyers and surveyors.

Table of Contents

- Option one, wait for full implementation

- Option two, proceed under the current statutory route

- Option three, negotiate an informal extension

What Is Leasehold Marriage Value

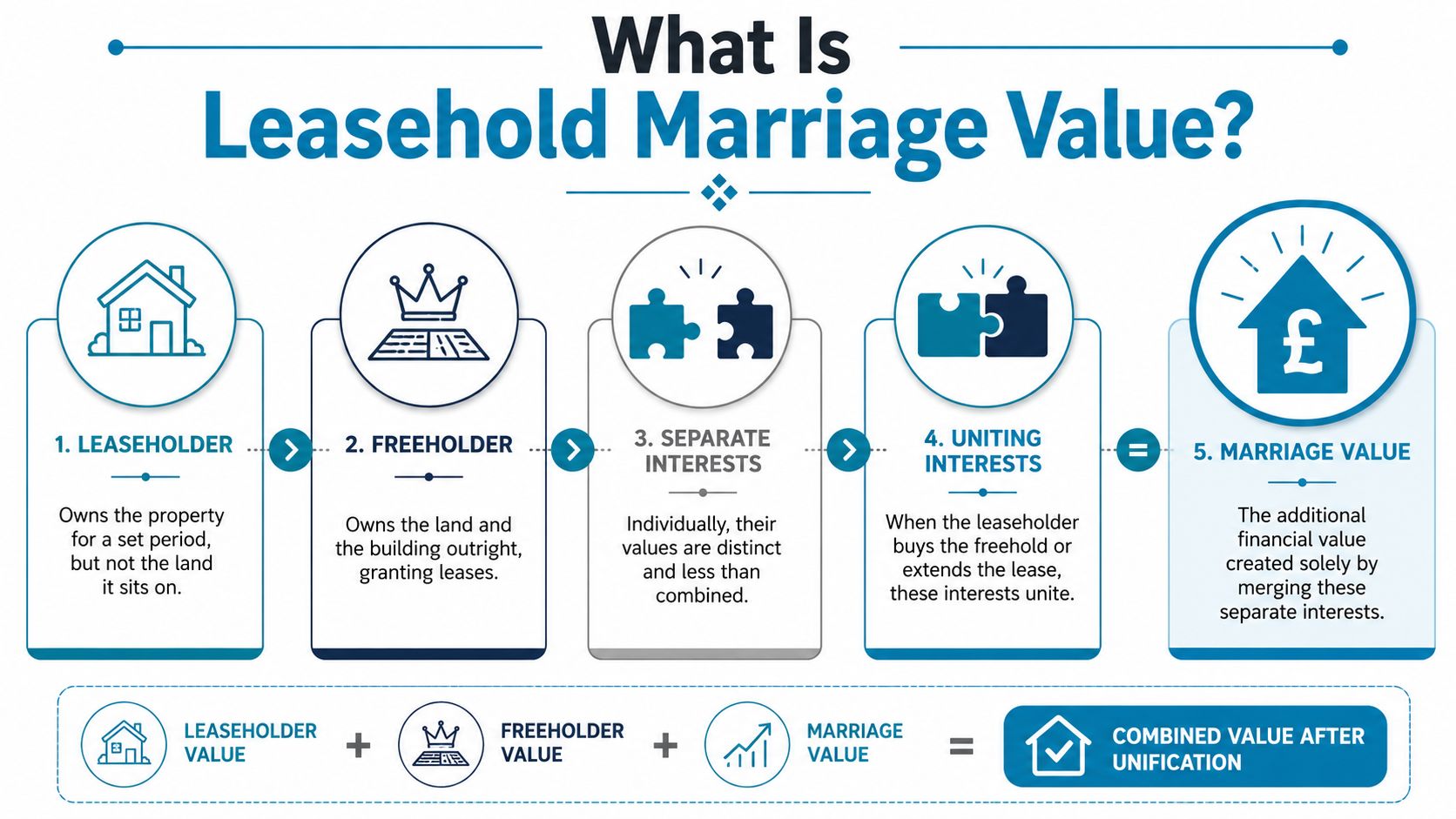

Leasehold marriage value is the extra value created when the leaseholder's interest and the freeholder's interest are brought together. The easiest way to think about it is as two puzzle pieces. Separately, each has value. When they interlock, the combined result is worth more than the two pieces looked to be worth on their own.

That extra uplift is what valuers call marriage value. In the leasehold system, it has historically formed part of the premium payable on certain statutory lease extensions and freehold acquisitions.

Why the 80-year mark matters

This isn't a charge that applies all the time. Under the law derived from the Leasehold Reform Act 1993, marriage value applies only when a residential lease has 80 years or fewer remaining, and the freeholder is entitled to 50% of that calculated uplift, as explained in Starck Uberoi's summary of leasehold marriage value.

That threshold matters because the cost profile changes once the lease passes it. Above that point, the extension premium is assessed without this extra element. At or below it, the calculation can become much more expensive.

Practical rule: If your lease is approaching the threshold, treat timing as a valuation issue, not just an admin task.

Why homeowners find it confusing

Most leaseholders understand ground rent and service charge because they see them on statements. Marriage value is different. It isn't a routine bill. It appears when you take action to extend the lease or buy the freehold through the statutory route.

That makes it feel abstract until it suddenly isn't. By the time many owners look into it, the lease has already shortened enough for the issue to matter.

A simple example shows the principle. If a flat with a short lease and the freeholder's separate interest together are worth less than the flat becomes worth after the lease is extended, the gap is the marriage value. The law historically split that uplift, with half going to the freeholder.

- Leaseholder's interest: You own the right to occupy the property for the term left on the lease.

- Freeholder's interest: The landlord owns the underlying reversion and any relevant ground rent stream.

- Combined interest: Once the lease is extended or the freehold is acquired, the market often treats the asset as more valuable.

- Marriage value: The added value created by that union.

- Who receives it: Under the old framework, the freeholder's statutory share is half.

In practice, that's why surveyors focus so closely on lease length. The shorter the lease becomes, the more careful you need to be about the timing and route you choose.

How Marriage Value Is Calculated

The old calculation often sounds more mysterious than it is. At heart, a valuer compares the separate interests with the combined position after the lease is improved. The difference is the marriage value.

For homeowners, the important point isn't to reproduce a tribunal spreadsheet. It's to understand where the extra premium comes from and why small shifts in lease term can affect negotiations.

A worked example in plain English

Take the example commonly used to explain the concept. A flat with a short lease is worth £200,000. The freeholder's separate interest is worth £5,000. After the lease is extended, the combined value becomes £250,000.

The uplift is £45,000. That is the marriage value. Under the old statutory framework, the landlord's share would be £22,500.

That example shows why homeowners feel the sting so sharply. The premium doesn't just reflect ground rent and reversion. Once marriage value applies, it captures part of the increase created by curing the short lease problem.

A real valuation reference point

In a cited valuation case, the difference between separate and common ownership was £8,250, derived from £330,250 minus £322,000, according to Peter Barry's explanation of how marriage value works.

That doesn't mean every leaseholder will face the same figure. They won't. The premium depends on the property, the term remaining, the lease terms and the valuation assumptions. But it does show the structure of the calculation clearly enough for a non-specialist to grasp what's happening.

If you want a broader sense of the wider premium, not just the marriage value element, this guide on how to value a lease extension is a helpful starting point.

What works and what doesn't

Here's where I see owners go wrong.

| Approach | What happens in practice |

|---|---|

| Relying on online chatter | You get broad opinions, not a defensible valuation. |

| Using the estate agent's sale figure as your premium guide | Sale value and enfranchisement value are related, but they aren't the same exercise. |

| Getting a specialist valuation early | You gain a realistic negotiating range and a clearer budget. |

A lease extension premium is a valuation problem first and a legal process second. If the valuation is weak, the rest of the case usually follows it downhill.

The exact mathematics can get technical quickly. The practical lesson is much simpler. If your lease is near the line, don't guess. Get the number modelled properly.

The 2024 Leasehold Reform and Its Current Status

The headline reform is genuine. The legal position on the statute book changed. The practical position for homeowners has not yet changed in the same clean way.

The Leasehold and Freehold Reform Act 2024 removes marriage value for statutory lease extensions and freehold acquisitions, and it also introduces other reforms intended to reduce enfranchisement costs. That is why many people have read that marriage value has been abolished.

Why the change still feels stuck

The difficulty is implementation. Current guidance in the market continues to flag that the relevant abolition provisions are suspended while legal challenges work through the courts. Leaseholders therefore face a limbo period where the law points one way, but transactions on the ground may still need to proceed under the old assumptions.

That uncertainty has been one of the most frustrating parts of advising owners near the threshold. People don't just want legal theory. They want to know whether to serve a notice now or wait.

As noted in Lease Extension UK's discussion of the current suspension, the abolition is legally in place but currently suspended due to judicial review challenges, with no firm implementation timetable and predictions of no practical change until 2026.

What this means for decisions now

That creates a very specific problem. If your lease is comfortably long, waiting may be tolerable. If you are already close to the threshold, waiting may expose you to the very cost you were hoping reform would remove.

For a broader policy context, Survey Merchant's leasehold update is useful background reading. It helps frame why owners are hearing mixed messages.

A sensible way to look at the current position is this:

- Law in principle: Marriage value is set to go.

- Law in operation: Homeowners may still face the old cost structure until the suspended provisions are brought fully into effect.

- Decision point: The shorter your lease, the less room you have to sit tight and hope.

Waiting can be rational. Waiting without a valuation, a timetable and a fallback plan usually isn't.

If you're making a 2026 decision, don't rely on headlines alone. Ask what rules are being applied in live transactions at the point you're ready to act.

The 80-Year Cliff Edge and Your Mortgage

The phrase I use with clients is “cliff edge” because that's how it behaves in real life. One side feels manageable. The other side can alter cost, saleability and mortgage conversations all at once.

A lease at 81 years and a lease at 79 years may sound almost identical to a homeowner. In practice, they can produce very different outcomes once a statutory claim is in view.

Why timing matters more than many owners realise

The key point is the timing of the statutory claim. Marriage value is payable when serving a Section 42 notice with 80 years or fewer remaining, which is why missing the threshold can become an irreversible financial problem, as discussed in this HousingUK thread on the 80-year cliffhanger.

That issue often collides with mortgage reality. A homeowner may be in a fixed-rate deal, may not have planned for a larger premium, and may discover too late that the lease term has become part of the refinancing conversation.

The practical trap is obvious. You delay because reform might help. The lease shortens in the meantime. Then your lender, buyer or broker starts asking harder questions.

A short explainer is worth watching here if you want the issue set out visually.

The financing pressure point

Owners often focus on premium only. Lenders focus on security as well. A lease with a shrinking term can affect how straightforward the property looks as collateral, which can narrow your room for manoeuvre just when you need flexibility.

That's one reason the wider conversation around leasehold and land tenure matters. If you want a broader perspective on long lease structures and how they shape ownership models, Unitism on land-use models gives useful context.

Consider the actual pattern:

- You remortgage late: The lender may scrutinise the lease term more closely than when you first bought.

- You try to sell with a shorter lease: Buyers ask for a discount or want the extension started before exchange.

- You budget only for legal fees: The valuation side turns out to be the bigger shock.

- You assume reform will arrive in time: The market doesn't pause while legislation catches up.

If your lease is close to the trigger point, the cheapest year to act is often the year before you feel any urgency.

That isn't alarmism. It's basic risk management.

Strategic Options For Homeowners in 2026

By the time homeowners ask about leasehold marriage value, they usually want one answer. Should I wait, proceed, or try a deal directly with the freeholder?

There isn't one universal answer. The right route depends on lease length, budget, how soon you may need to remortgage or sell, and how much uncertainty you can tolerate.

Option one, wait for full implementation

Waiting appeals for an obvious reason. Once the reform is fully in force, marriage value is expected to fall away from statutory calculations, and the new regime includes a ground rent cap of 0.1% of freehold value for premium calculations while also limiting recovery of certain non-litigation costs, with Peter Barry describing this as promising substantial premium savings.

The upside is potential cost reduction. The downside is that your lease keeps shortening while you wait. If you are near the threshold, that can be a poor trade.

This route tends to suit owners with enough lease length left to absorb delay and enough financial flexibility to pivot if implementation takes longer than hoped.

Option two, proceed under the current statutory route

This is the lower-uncertainty route. You instruct a specialist valuer, budget on the basis of the current position, and move forward using the rights available now.

The benefit is certainty of process. You stop gambling on timing. If the lease is already short or you need to refinance, that certainty often matters more than chasing a future saving that may not arrive when you need it.

The drawback is obvious as well. If marriage value still applies in practice when you proceed, you may pay more than you would under a fully implemented reformed system.

Option three, negotiate an informal extension

Some owners explore an informal deal with the freeholder instead of serving a statutory notice. That can sometimes be useful where speed matters or where both sides are commercially realistic.

But informal deals need careful scrutiny. The headline premium may look attractive while other terms worsen unobserved. I've seen cases where the owner focused on the upfront number and missed less favourable lease wording, continuing ground rent liability, or other terms that reduced the long-term benefit.

A simple comparison helps.

| Option | Main advantage | Main risk |

|---|---|---|

| Wait | Possible savings if reform becomes fully operational | Delay may shorten the lease and weaken your position |

| Statutory route now | Clear legal framework and firmer control of timing | You may still face current valuation rules |

| Informal deal | Can be quicker and more flexible | Terms may be less favourable than they first appear |

My view: if you are close to the danger zone, the decision should be driven by risk exposure, not by hope.

For homeowners who need a specialist valuer to model those scenarios, Survey Merchant is one route to finding a surveyor experienced in lease extensions and enfranchisement work. The value in any platform or referral source is simple. It should connect you with someone who can quantify the options before you commit to one.

Assembling Your Professional Team Surveyor and Solicitor

A lease extension is one of those jobs where homeowners get the best results when each professional stays in their lane and does that part properly. The surveyor handles value and negotiation on price. The solicitor handles the legal machinery.

When either side is weak, the owner usually feels it in cost, delay or poor terms.

What the surveyor actually does

A chartered surveyor doesn't just “give you a number”. The job is to inspect the facts of the lease, assess the property, apply the relevant valuation approach, and advise on what constitutes a realistic premium and negotiation range.

That matters because the first figure a homeowner hears is not always the right one. A specialist valuer should be able to explain not only the likely premium, but also where the pressure points are and what assumptions are driving it.

If you need a starting point on selecting the right professional, this surveyor for lease extension guide covers the basics clearly.

What the solicitor does differently

The solicitor's role is procedural and protective. They serve notices, review the lease terms, deal with the legal drafting, and make sure the final document reflects what was agreed.

That legal review matters particularly with informal deals. The premium may look acceptable, but the lease wording may still leave the homeowner worse off than expected.

A useful wider read, especially if a sale may follow the extension, is this guide to UK property sales. It gives practical context on how buyers assess saleability and transaction readiness.

How the team works best

The smoothest cases usually share three features:

- The surveyor is instructed early: That gives the owner a realistic budget before legal steps begin.

- The solicitor reviews the route before documents are issued: This avoids procedural mistakes and helps align strategy.

- The homeowner provides paperwork promptly: Missing leases, title documents and correspondence slow everything down.

Here's the split in simple terms:

| Professional | Primary focus |

|---|---|

| Surveyor | Premium, valuation evidence, negotiation strategy |

| Solicitor | Notice, drafting, compliance, registration |

| Homeowner | Decision-making, documents, budget, instructions |

Good outcomes usually come from coordinated advice, not from one professional trying to do two jobs badly.

If you're extending because you may refinance or sell later, that joined-up approach matters even more. The valuation, the lease wording and the transaction timing all need to line up.

Your Next Steps on Leasehold Marriage Value

If you take one point away, let it be this. Leasehold marriage value is not just a technical formula. It is a timing issue with financial consequences.

The old rule remains the practical benchmark many owners still have to work with while the 2024 reforms sit in limbo. That's why homeowners with shorter leases need advice grounded in current transaction reality, not just legislative headlines.

A practical checklist

Start with the basics and be exact.

- Check the unexpired term: Don't estimate it from memory or an old sales brochure.

- Find out whether a sale or remortgage is likely soon: That affects how much delay you can tolerate.

- Get a specialist valuation: You need a proper view of the likely premium, not just a rough guess.

- Ask about both statutory and informal routes: One may suit your circumstances better than the other.

- Speak to a solicitor before committing to terms: Especially if a freeholder offers an informal deal that sounds quick and cheap.

The decision most people regret

In practice, the mistake that causes the most frustration is delay without a plan. Waiting can be sensible. Waiting because internet articles made the position sound settled is where owners get caught.

If your lease is already close to the point where marriage value may affect cost, your next move should be to replace uncertainty with numbers. Once you know the likely premium and the legal options available today, the decision becomes far clearer.

Professional advice won't remove every trade-off. It will stop you making the decision blind.

If you need help finding a specialist to assess your lease extension position, Survey Merchant can connect you with a suitable UK surveyor for leasehold valuation and enfranchisement advice, so you can understand the likely premium, the timing risks and the options open to you before you commit.