Valuation

Jul 16, 2026

RICS Survey Help to Buy: Your 2026 Valuation Guide

Get your rics survey help to buy valuation right in 2026. Our guide covers rules, costs, and the step-by-step process for loan repayment.

If you’re looking up rics survey help to buy, you’re probably at the point where the scheme stops feeling simple. You may be selling, remortgaging, or repaying part or all of the equity loan, and suddenly everyone wants a valuation, a deadline, a named administrator, and the right paperwork in the right format.

That catches many owners out. They assume any valuation will do, or that the figure is a rough formality before the solicitor takes over. It isn’t. The valuation is the figure used to calculate what you owe on the equity loan, so the report has a direct financial effect on you.

I’ve seen the same pattern repeatedly. The stress rarely comes from the inspection itself. It comes from uncertainty. People don’t know which surveyor is acceptable, what must appear in the report, how long it stays valid, or what to do if the figure feels out of line with nearby sales.

A proper Help to Buy valuation should remove that uncertainty, not add to it. Done correctly, it gives you an evidence-based market value, a compliant report, and a clear basis for the next legal and financial steps.

The Help to Buy valuation exists for one reason. It establishes the current market value of your home so the scheme administrator can work out what percentage-based repayment is due when you sell, remortgage, or staircase.

That sounds straightforward until real money is attached to the figure. If your home has risen in value since purchase, the repayment rises with it because the loan is a share of the property’s value, not a fixed sum. If the valuation comes in lower than you expected, that can help on the repayment side, but it may complicate a sale or remortgage if the number doesn’t sit comfortably with the rest of the transaction.

Most of the friction comes from mixing up three different things:

They are not interchangeable.

Practical rule: For Help to Buy, the report isn’t just about opinion. It must also be acceptable in format, authorship, and evidence.

There’s another point many owners don’t realise early enough. The report is part legal compliance, part valuation evidence, and part timing exercise. If one part goes wrong, the transaction can stall even if the value itself is reasonable.

A correct valuation saves avoidable delay. A rejected one means rebooking, resubmitting, and often paying again. That’s especially frustrating when your solicitor, lender, buyer, or onward purchase is already waiting.

The aim is simple. You need an independent RICS valuation that stands up on evidence, meets the Help to Buy rules, and gives you a figure you can understand and challenge sensibly if necessary.

A Help to Buy RICS valuation is an independent assessment of your property’s current market value by a qualified surveyor working to recognised professional standards. It is used for equity loan redemption, sale, or staircasing under the Help to Buy process.

The easiest way to understand it is to think of the government equity loan as a shareholding. If someone owns a share of an asset, they don’t get repaid based on what that asset was worth years ago. They get repaid based on what it is worth now. That’s why the valuation matters so much.

According to RICS market surveys guidance, the Help to Buy scheme launched in 2013 and enabled over 400,000 UK households to buy homes with minimal deposits, while Help to Buy transactions requiring redemption or staircasing rely on RICS valuations built on independence and comparable evidence.

This isn’t a box-ticking exercise. The valuation sits at the centre of the repayment calculation.

If you’re reviewing multiple documents, it can help to analyze real estate inspection reports so you can compare valuation wording, property details, and supporting comments before you send anything on to your solicitor or administrator.

The valuation also needs to be prepared to the right standard. In practice, clients will often hear the term Red Book valuation. That refers to the professional framework surveyors use for formal valuation work. If you want a plain-English explanation of that standard, this guide to a Red Book valuation is a useful reference.

A lot of owners order the wrong thing because the names sound similar. Here’s the simplest distinction:

| Report type | Main purpose | Who it is for | Acceptable for Help to Buy redemption |

|---|---|---|---|

| Mortgage valuation | Supports lending decision | Lender | No |

| Building survey | Reviews condition and defects | Buyer or owner | No, on its own |

| Help to Buy RICS valuation | Establishes current market value for equity repayment | Help to Buy administrator and homeowner | Yes, if compliant |

A building survey can still be helpful in the wider decision-making, especially if defects affect marketability or sale strategy. But it doesn’t replace the formal Help to Buy valuation report.

The common mistake is assuming a lender’s figure and a Help to Buy figure should be identical. They often aren’t because the instruction, audience, and reporting requirements are different.

The compliance side is where many perfectly sensible transactions start to wobble. A valuation can be professionally prepared and still be rejected if it doesn’t meet the administrator’s checklist.

The mandatory items are specific. According to guidance on how RICS home surveys support Help to Buy valuations, the valuation report must be addressed to Homes England (or Target HCA), be on headed paper, be signed by the RICS surveyor, include at least 3 comparable properties within 2 miles, and remains valid for 3 months from the inspection date.

That same guidance also notes practical administration points that regularly matter in real cases. The report should be supplied as an uneditable PDF, and submission is required within 5 working days. It also states that the valuation typically costs around £250 inc VAT.

If you’re dealing with other equity or lease-related property matters alongside the valuation, the wider context in this article on Help to Buy, shared ownership schemes and staircasing can help separate one process from another.

This catches people out more often than it should. A valuation for Help to Buy isn’t supposed to come from anyone with a conflicting interest in the transaction. That means a bank or mortgage valuation won’t do, and using someone tied too closely to the sale can create avoidable problems.

In practical terms, independence protects you as much as it protects the administrator. If the figure is challenged later, a properly instructed independent valuer is in a far stronger position than someone whose role was never suitable for Help to Buy in the first place.

The validity period is short. Three months passes quickly when you’re also dealing with lenders, solicitors, title documents, redemption statements, and buyer negotiations.

A lot of owners assume that once the report is done, the hard part is over. It isn’t. The moment the report lands, the clock is already running. If the case drifts, the valuation can expire before repayment completes.

To help with the timing side, it’s worth watching this practical overview:

If your valuation date is getting close to expiry, don’t wait for someone else in the chain to notice. Ask the question early and in writing.

This is one of the least clearly explained parts of the process. Official guidance says that if repayment isn’t completed within the initial validity window, you’ll need to provide and pay for a new valuation report. But in practice, some owners hear about “desktop extensions” and assume that’s an automatic cheaper alternative.

It isn’t that simple.

The grey area is eligibility. Government guidance confirms the need for a new valuation if the original expires, but it doesn’t set out a clear public framework for when a desktop update might be acceptable instead of a fresh inspection. That leaves owners unsure about cost, timing, and risk.

A sensible approach is to treat any extension as uncertain unless your surveyor and the administrator confirm otherwise. Budget and plan on the basis that a new compliant report may be needed.

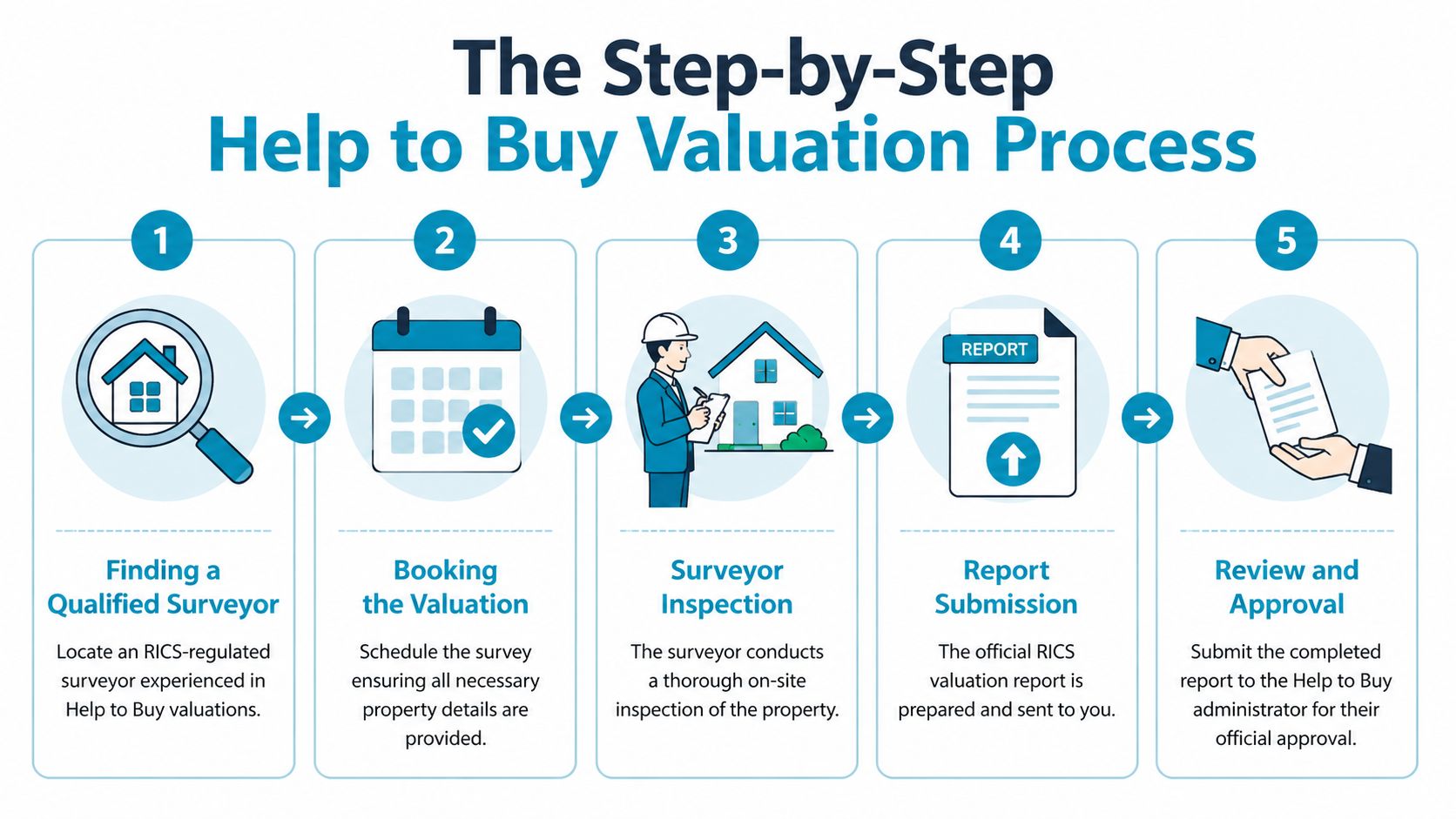

Once you know the rules, the process becomes manageable. Most problems come from doing the right things in the wrong order, or leaving too little time between each stage.

Start with the instruction, not the fee. You need a surveyor who understands that this is a Help to Buy valuation, not a standard estate agency appraisal and not a lender’s mortgage valuation.

In practice, many owners use a broker platform or direct local firm. Survey Merchant is one option that matches instructions to qualified surveyors from a nationwide panel, including work such as RICS valuations and related property reports.

Before booking, ask three practical questions:

Owners often overthink this part. You don’t need to stage the house like a glossy brochure, but you do need to make inspection straightforward.

Useful preparation includes:

If the property has unresolved snagging or visible issues, tell the surveyor. Concealing defects doesn’t help you. A proper market valuation has to reflect condition.

The valuer isn’t just walking around deciding whether they “like” the property. They are comparing it to evidence from the local market and reconciling your home against that evidence.

The report should reflect location, accommodation, condition, tenure, and comparable sales. The administrator’s format requirements also mean the surveyor needs appropriate supporting comparables, not just a headline figure.

Modern inspection tools can support this process in some cases. According to scan-to-BIM guidance for surveyors, technologies such as Matterport scanning, validated by RICS with ±1% accuracy, can support snagging and valuation-related inspection work and generate defect schedules that may cut buyer holding costs by 15% through faster developer rectifications.

That doesn’t mean every Help to Buy valuation needs advanced scanning. It does show that careful evidence gathering and defect recording can influence how quickly related issues are resolved.

When the report arrives, don’t just read the final figure and forward it on. Review the basics first.

Check for:

A surprising number of delays happen because nobody checks the obvious administrative points until after rejection.

A compliant report is both a valuation document and an application document. Treat it as both.

This is the stage where people relax too soon. The valuation itself may only take a short time to arrange, but the wider transaction can stretch.

As soon as the report is issued:

If your sale or remortgage timetable starts slipping, deal with that early. A valid report today doesn’t help if it expires before the legal steps catch up.

The first figure everyone looks at is the market value. That matters, but it shouldn’t be the only thing you read. The essential substance of the report is often in the comparable evidence and the surveyor’s reasoning.

Start with the comparables. Are they similar in type, size, age, setting, and tenure? A flat should usually be supported by other flats, not nearby houses. A modern new-build style property should be compared with similar stock where possible, not very different older homes because they are close by.

Then read the commentary. Even where the final figure is disappointing, the explanation may be perfectly coherent. Condition, outlook, floor level, parking, lease terms, incentives on competing stock, and saleability all affect value.

If you’re still unclear about how formal valuations differ from lending assessments, this guide on what a mortgage valuation is helps explain why two figures in the same transaction may serve different purposes.

Because the equity loan is repaid as a percentage of the current market value, changes in value directly affect what you owe. Guidance on getting an RICS-compliant Help to Buy valuation notes that a 5-10% variance in valuation can represent thousands of pounds in additional liability for the homeowner because the repayment is percentage-based and not tied to the original purchase price, as explained in this Help to Buy valuation guide.

Here is the basic calculation for a 20% loan:

| Original Purchase Price | Current Market Value | Repayment Amount (20% of Current Value) |

|---|---|---|

| £250,000 | £250,000 | £50,000 |

| £250,000 | £275,000 | £55,000 |

| £250,000 | £300,000 | £60,000 |

The original purchase price in the table is there for context. The repayment figure is driven by the current value, not by what you paid at the start.

There is recourse, but it needs to be sensible and evidence-led. Don’t begin with “my neighbour says it’s worth more”. Begin with the comparables and the facts.

A practical approach is:

Not every disagreement justifies a revised valuation. But if the evidence base appears inconsistent with the local market, a calm, documented query is the right response.

The strongest challenge is not emotional. It is comparative. Show why one piece of market evidence is more relevant than another.

Most Help to Buy valuation problems are avoidable. They happen because someone assumes the process is informal when it’s tightly administered.

Here are the mistakes that cause the most grief.

Using a lender’s valuation instead: A bank or mortgage valuation is not the same thing as a Help to Buy valuation. If you submit the wrong report, the case can be rejected and you lose time.

Letting the report expire: Official government guidance states that if repayment isn’t completed within the 3-month validity period, you must provide and pay for a new valuation report, as set out in the government’s Help to Buy valuation guidance. This is one of the most expensive avoidable mistakes because it often lands when the legal work is nearly complete.

Choosing a surveyor without the right instruction: Even a competent surveyor needs the correct brief. If you book a standard market valuation without making clear it is for Help to Buy redemption, the report may not be produced in the right format.

Ignoring the supporting evidence: Homeowners sometimes fixate on the final number and fail to review the comparables. That matters because any challenge needs to be based on evidence, not frustration.

Assuming everyone else is tracking the deadline: Solicitors, lenders, buyers, and administrators are all watching their own part of the file. You need to watch the valuation date yourself.

The simple discipline is to treat the report like a time-sensitive legal document, not just a property opinion.

Possibly, but only if the surveyor is independent and the report is prepared as a Help to Buy compliant RICS valuation. Independence matters more than who introduced them.

No. A home survey looks at condition and defects. A Help to Buy valuation provides a formal market value for the equity loan process. They serve different purposes.

That can happen. The administrator is concerned with the compliant valuation figure for the equity loan process. Your buyer and lender may be working from different information and objectives. If the gap is significant, your solicitor may need to help align the transaction.

Sometimes people refer to desktop extensions, but the public guidance isn’t clear on when that route is available instead of a new inspection. Treat it as uncertain until confirmed. If there is any doubt, assume a new valuation may be required.

Raise it promptly with the surveyor and provide better evidence if you have it. Good challenges are specific. Point to more relevant sold comparables, not broad online estimates or asking prices.

Ask directly whether they carry out Help to Buy valuations, whether they are RICS qualified for the work, and whether the report will be prepared in the required format for submission to the administrator.

If you need a compliant Help to Buy valuation and want the instruction matched to an appropriate professional, Survey Merchant connects property owners with qualified surveyors for RICS valuations and related property reports across the UK.

Survey Merchant provides vetted RICS surveyors across 100+ UK locations at fixed fees:

→ Level 2 Home Survey (HomeBuyer Report)

→ Level 3 Building Survey (full structural survey)

→ RICS Red Book property valuations

→ Party wall surveyors — notices, awards & schedules of condition

→ Expert witness surveyors — CPR Part 35 reports for property disputes