A solicitor has asked for a RICS Red Book valuation. Or your lender, accountant, former spouse's solicitor, or probate adviser has used the term as if it's self-explanatory. For most clients, that's the moment the confusion starts.

What you usually want to know isn't the history of the Red Book. You want to know whether you need one, what it will cover, and why a cheaper estimate or estate agent's figure won't do the job. That's the practical question that matters when a property value has to stand up to scrutiny.

In day-to-day practice, the difference is simple. A Red Book valuation is a formal professional opinion of value prepared to an established standard. It isn't a sales pitch, a rough estimate, or a lender-only check. If the figure may be questioned by HMRC, a court, a lender, or another professional adviser, standards matter. If you only want a broad sense of what your home might sell for, they often don't.

If you're still getting to grips with the wider process, these local property valuation insights in Preston give useful context on how valuers approach property assessment in practice. It also helps to read independent advice on selecting a property valuer before you instruct anyone, because the right brief and the right valuer make a noticeable difference to the quality of the report.

Table of Contents

Your Guide to RICS Red Book Valuations

A rics red book valuation is the form of valuation people turn to when the number must carry weight. That usually means a property decision with legal, tax, lending, or financial consequences. In those cases, nobody wants an off-the-cuff figure. They want a report that is reasoned, documented, and professionally accountable.

The problem is that the term gets used loosely. Clients often hear “you need a Red Book” and assume it's merely a more detailed valuation. It's more than that. A key distinction is that it sits inside a recognised professional framework and is prepared for a defined purpose.

That matters because different valuation products do different jobs. A market appraisal helps someone decide an asking price. A lender's valuation helps a lender judge its security. A Red Book valuation is typically the one used where an independent figure has to be defended.

Practical rule: If someone else may challenge the figure, ask for a formal valuation standard, not an estimate.

In practice, that changes the surveyor's approach. The valuer must identify the purpose of the instruction, the correct basis of value, the relevant assumptions, the extent of inspection, and the evidence supporting the opinion. That discipline is what gives the report credibility.

Clients usually benefit from thinking in terms of risk rather than paperwork. If the valuation may influence tax reporting, borrowing, settlement negotiations, or court proceedings, the cost of getting the wrong type of report is often far higher than the cost of instructing the right one in the first place.

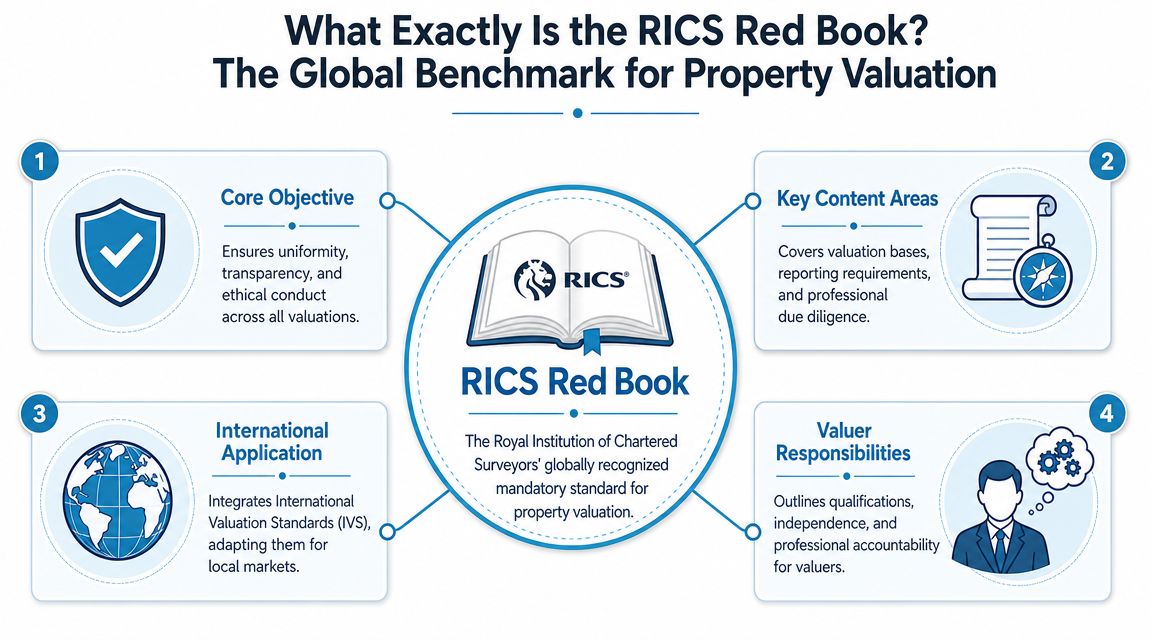

What Exactly Is the RICS Red Book?

The RICS Red Book is the professional standards framework for valuation work by RICS members in the UK and worldwide. RICS states that it contains the mandatory rules, best-practice guidance, and related commentary for members undertaking valuation services, and that it is issued as part of its commitment to high standards in valuation delivery worldwide, as set out in the RICS Red Book standards overview.

Think of it in the same way you'd think about professional rules in accountancy or law. The value in the document isn't the colour of the cover or the label. It's the framework behind the work. That framework tells the valuer how the instruction should be set up, what must be disclosed, and how the final opinion should be reported.

Why that framework matters

A Red Book valuation isn't just “more official”. It is prepared to standards designed to support consistency, transparency, and objectivity. That's why clients, lenders, solicitors, and tax advisers often ask for it by name.

The practical benefit is straightforward:

- Clear purpose. The report is prepared for a defined use, such as probate or matrimonial proceedings.

- Defined basis of value. The valuer doesn't merely state a figure. The report explains what type of value is being assessed.

- Professional accountability. The surveyor is responsible for the quality and defensibility of the opinion.

A strong valuation report doesn't rely on confidence alone. It shows how the valuer reached the conclusion.

What the Red Book is not

It isn't a promise that nobody will ever disagree with the number. Reasonable professionals can differ within a market. What it does provide is a structured method and reporting standard that makes the opinion credible.

It also isn't the same as an estate agent's pricing advice or a quick desktop estimate. Those can be useful in the right setting, but they're different products serving different needs. The mistake clients make is treating all “valuations” as interchangeable. They aren't.

When Do You Need a Red Book Valuation?

The easiest way to answer this is to ask one question. Who will rely on the figure, and what happens if they disagree with it? If the answer includes a lender, HMRC, a court, or another formal decision-maker, a Red Book valuation is often the sensible route because the standards are framed around valuation reports, bases of value, inspections, and reporting requirements, which is why they are important where scrutiny is expected, as outlined in the RICS Red Book Global standards page.

Situations where it is usually non-negotiable

For probate, the figure may need to support inheritance-related reporting and stand up if questioned later. Executors often discover that a casual opinion is of limited use once documentation is requested and the basis of value needs to be clear.

For divorce or matrimonial proceedings, the issue is usually independence. Neither side wants the other relying on an optimistic asking-price estimate. A formal valuation gives both parties and their advisers a more reliable starting point.

For tax matters, the standard matters because the figure may be reviewed in detail. If the valuation has to be explained, challenged, or defended, the report needs reasoning, assumptions, and evidence.

For secured lending or refinance, the exact product required depends on the lender's process, but where a formal valuation is requested for professional or legal use, a Red Book instruction gives a recognised framework.

Some statutory and scheme-based matters also call for a formal valuation. Shared ownership staircasing, leasehold disputes, and similar instructions often require a report that follows a recognised professional standard rather than a marketing estimate.

If the valuation may affect a legal right, a tax position, or a borrowing decision, treat it as evidence, not as guidance.

When a lighter-touch opinion may be enough

Not every situation needs full Red Book formality. If you're only deciding whether to sell, test the market, or budget for future plans, an estate agent's appraisal or informal advice may be perfectly adequate.

The trade-off is reliability versus cost and speed. Informal opinions are quicker and cheaper, but they usually carry less weight. If you are improving a property before sale, practical refurbishment planning can matter more at that stage than formal valuation reporting. In that context, guidance on how to maximize home value with budget-friendly renovations can be more useful than commissioning a formal report too early.

Red Book Valuations vs Other Appraisals

Clients often put three very different things into one bucket: a Red Book valuation, a mortgage valuation, and an estate agent appraisal. They all involve an opinion on value, but they are not interchangeable.

The difference starts with who the report is really for. That point alone clears up most misunderstandings.

Comparison of Property Valuation Types

| Attribute | RICS Red Book Valuation | Mortgage Valuation | Estate Agent Appraisal |

|---|---|---|---|

| Purpose | Independent opinion for legal, tax, financial, or dispute-related use | Security check for a lender | Marketing guidance for a potential sale |

| Main client | The instructing client or professional adviser | The lender | The owner |

| Scope | Formal instruction with defined assumptions, inspection scope, and reporting | Usually narrower and focused on lending risk | Usually brief and sales-focused |

| Legal standing | Stronger, because it is designed as a formal valuation report | Limited to the lender's purpose | Indicative only |

| Detail level | Reasoned and documented | Often concise | Usually informal |

| Best use | Probate, divorce, tax, expert support, formal decision-making | Mortgage lending | Setting an asking price |

If you want more detail on the lender-specific side, these insights into mortgage valuations explain why borrowers are often surprised by how limited that product can be.

The practical mistake clients make

A mortgage valuation can be carried out by a surveyor, but that doesn't make it the same as a Red Book report prepared for your own legal or tax purpose. The intended user and reporting basis matter.

An estate agent's appraisal has value too. Good agents understand buyer behaviour and local pricing strategy. But their task is usually to advise on marketing, not to produce a formal expert report for scrutiny by third parties.

A market appraisal answers, “What might this sell for?” A Red Book valuation answers, “What is the value for this defined purpose, on this basis, supported by this evidence?”

That's why trying to save money by using the wrong product often creates more work later. Clients then need a second report, usually under tighter deadlines.

What to Expect from Your Valuation Report

Most Red Book instructions follow a predictable path. That's helpful, because once you know the sequence, the process stops feeling obscure and starts feeling manageable.

From instruction to inspection

The process starts with the terms of engagement, in which the valuer defines the property, the client, the purpose of the valuation, the basis of value, any assumptions, and the scope of inspection. If those points are vague at the outset, the report can miss the mark even if the valuation work itself is competent.

The inspection itself is not a building survey, but it is still an important part of the evidence-gathering exercise. The valuer will normally inspect the property in a way that is appropriate to the instruction, noting size, layout, condition, location, accommodation, tenure points if relevant, and anything that may influence value.

Off site, the valuer then tests the property against the market. That usually includes comparable evidence, legal and planning context where relevant, and any specific factors tied to the instruction. For probate, for example, the valuation date can be critical. For matrimonial work, neutrality and reasoning are often under close attention.

What the report actually tells you

A proper report should do more than present a headline figure. It should identify the valuation date, because value is always tied to a date, not floating in the abstract. It should also state the basis of value, such as market value where appropriate to the instruction.

You should also expect to see any important assumptions or limitations. If the valuer has made a special assumption, that should be clear. If access was restricted, that should be clear too. The reader shouldn't be left guessing what the opinion relies upon.

A useful way to read the report is to check these points first:

- Purpose. Does the report clearly say what it has been prepared for?

- Property details. Are the address, tenure, and relevant characteristics correct?

- Date. Is the valuation date the one required for your matter?

- Assumptions. Are there any assumptions that could affect how the figure is used?

- Conclusion. Is the final value unambiguous?

Ask questions if the report uses technical wording you don't recognise. A competent valuer should be able to explain the basis of the opinion in plain English.

Turnaround and fees vary by property type, complexity, and urgency, so it's better to ask for these at instruction stage rather than rely on generic expectations. The more unusual the property or the legal context, the more important that early conversation becomes.

Compliance and the Future of Valuations

The value of a Red Book report lies in more than the number on the last page. It lies in whether the report is compliant, properly reasoned, and suitable for the purpose it is meant to serve.

Why compliance matters

A non-compliant or loosely prepared valuation can create practical problems very quickly. It may be challenged for lack of clarity, rejected because the basis of value is not properly identified, or carry less weight because the assumptions and evidence are not transparent.

That risk shows up most often when clients try to retrofit an informal valuation to a formal problem. A sales estimate prepared months earlier rarely converts neatly into evidence for probate, tax, litigation, or negotiated settlement. The report has to be designed for that use from the start.

The wider point is that standards protect everyone involved. They help the client understand what has been done. They help the valuer define the limits of the instruction. They help third parties assess whether the opinion is suitable for reliance.

What the 2025 revisions change

A major recent development is the 2025 revision of the Red Book, which reflects changes in valuation practice around ESG, technology, and data governance. Industry commentary on the revision notes a stronger emphasis on valuation modelling, risk assessment, ESG data integration, and the use of AI and new technology, as discussed in this summary of the 2025 Red Book revisions and valuation practice.

The practical point for clients is that valuations are moving beyond traditional comparables alone. The 2025 revisions mandate consideration of ESG factors. Valuers must record relevant data and assess its impact, including energy efficiency, carbon footprints, and sustainability. Where AI-driven data analysis is used, that use must also be clearly disclosed in the report.

That doesn't mean every report suddenly becomes a sustainability audit. It does mean environmental performance and data handling are no longer side issues. For some properties, those factors may have limited impact. For others, they may become material to value, risk, or marketability.

The future direction is clear. Clients should expect valuation reports to explain not only what a property is worth, but also which documented risks and characteristics materially shape that opinion.

How to Commission a Compliant Red Book Valuation

Instructing a valuation is usually straightforward once you know what information matters upfront. Problems tend to arise when the purpose is unclear, the wrong valuer is appointed, or relevant documents only appear after the inspection.

A straightforward instruction process

Start with the reason for the report. “I need a valuation” is not enough. “I need a probate valuation for a freehold house” or “I need a matrimonial valuation for a leasehold flat” is much more useful because it tells the valuer what standard, basis, and reporting context are likely to apply.

Then gather the obvious paperwork. Depending on the property and purpose, that may include title documents, lease information, plans, tenancy information, planning material, and any previous relevant reports. You don't need to overprepare, but you do need to avoid withholding something material that could affect value.

A sensible appointment process usually looks like this:

- Define the purpose clearly. Probate, tax, divorce, finance, dispute resolution, or scheme requirement.

- Check qualifications. Ask whether the surveyor is a RICS Registered Valuer and whether they handle that type of property and instruction.

- Review terms before instructing. Make sure the report purpose, property, fee basis, and timetable are clear.

- Provide access and documents promptly. Delays often come from practical hold-ups, not valuation analysis.

- Read the final report properly. Check the date, assumptions, and stated purpose before sending it on.

What to ask before you appoint anyone

Don't just ask for a fee. Ask whether the surveyor regularly carries out this exact kind of valuation. A valuer who is strong on residential probate work may not be the right fit for a commercial dispute, and vice versa.

You should also ask who the report is intended to be relied upon by, whether any special assumptions are anticipated, and whether the property has any unusual features that could affect timing or scope.

If you want a route to obtaining quotes for formal UK property valuations, one practical option is Survey Merchant, which connects clients with a nationwide panel of surveyors for valuation instructions. The key point, whichever route you choose, is to match the instruction to a valuer with the right experience, not solely the lowest fee.

A well-commissioned Red Book valuation is rarely complicated from the client side. It just needs a clear purpose, a properly briefed valuer, and enough information to produce a report that can do the job it is meant to do.

If you need a formal valuation for probate, divorce, tax, lending, or another matter where the figure must stand up to scrutiny, Survey Merchant can help you source quotations from appropriately qualified surveyors for the instruction.